If the Once-Mighty Intel Is Going to Reverse Course, It Will Have to Show Me

Intel gave an update on its foundry segment. The results are ugly. Still, there's a way to trade this name.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Intel INTC was once the mighty of the mighty when it came to all things semiconductors. Though Intel remains one of the 30 stocks included in the Dow Jones Industrial Average, like that average itself, Intel has gone quietly off into the mist to fight simply for renewed relevance.

Year after year, Intel watched helplessly as Advanced Micro Devices AMD stole its lunch, taking a seemingly ever-growing share of the PC processor business. Then there was the high-end market for the data-center and then generative AI. It felt like Nvidia NVDA dominated that market before Intel even knew there was a market to dominate. AMD and Marvell Technology MRVL have at least made some noise in those markets.

Intel? The firm thought that they could go back to an earlier time and serve as a semiconductor foundry as so many competitors design their own chips but then rely upon Taiwan Semiconductor TSM and the smaller GlobalFoundries GFS to then manufacture their products. There were naysayers. Many folks doubted that Intel could attract much business beyond their own.

Last night, Intel updated its foundry segment. The results are ugly, but the company points toward future success. What to think?

Yikes

Intel held a brand-new segment reporting webinar late Tuesday and made an announcement. There was some good news. This was that Intel's Foundry business currently has an "expected lifetime deal value with external customers of more than $15B." There was some less than good news. The foundry business had suffered an operating loss of $7B in 2023 on sales of $18.9B. That's incredibly a deeper operating loss than 2022 on reduced revenue. The firm posted an operating loss of $5.2B for 2022, on sales of $27.5B.

It's okay, despite the fact that most of Intel's foundry revenue comes from its own operations, the firm expects to ascend to taking its place as the second-largest semiconductor foundry in the world by the year 2030. That would put them behind Taiwan Semiconductor and ahead of GlobalFoundries? Actually, Intel claims that there are five companies committed to using the latest techniques in semiconductor fabrication, known as 18A. This technique will become widely used by next year, supposedly, and then accelerate across the industry.

What's even better? Intel tells us that the foundry's operating losses are peaking this year (2024) and the firm will target 40% adjusted gross margins and 30% adjusted operating margins, again, by the year 2030 with an eye toward breaking even by 2027. Do I trust Intel to actually take share in the space with sales going backwards already? Let's pretend I'm from Missouri. They'll have to show me.

Three Weeks Out

Intel is expected to report first quarter financial results on or about April 26th. Consensus view is for an adjusted EPS of $0.14 (or GAAP EPS of $-0.11) on revenue of about $12B. This would compare to an adjusted EPS of $-0.4 for the year ago comp, while reflecting overall revenue growth of close to 8%. What Intel adds along the lines of firm-wide guidance in sight of what was mentioned above may matter as much as anything else.

The stock currently trades at roughly 33 times forward looking earnings. Nvidia trades at 37 times forward looking earnings and Nvidia is expected to post sales growth of almost 250%. Does that make INTC expensive? Well, it certainly does not make INTC inexpensive.

For the past twelve months, Intel posted firm-wide operating cash flow of $11.471B but spent $25.75B on capital expenditures. That put free cash flow at a rather grotesque $-14.279B. The balance sheet is okay, but not spectacular. Current and Quick ratios stand well above the 1.0 level, but the debt-load is on the large side. I see nothing here that I am overly impressed with. At least the firm stopped repurchasing common stock for its corporate treasury.

Wall Street

Since last night when Intel updated us all on its foundry business, I have come across 13 highly rated (4+ stars at TipRanks) sell-side analysts who have opined on INTC. The lack of positive ratings is startling. Among the 13, there is one "buy" rating, nine "hold" or hold-equivalent ratings and three outright "sell" or sell-equivalent ratings. One of the holds did not set a target price, so we are working with 12 of those.

After allowing for changes, the average target price across the remaining 12 works out to $44.54 with a high of $62 (Cody Acree of Benchmark) and a low of $31 (Chris Caso of Wolfe Research). Once omitting those two as potential outliers, the average target drops slightly to $44.15. The average "hold" target came to $45.69, while the average "sell' target came to $35.67.

My Thoughts

Well, to say the least, I am not impressed.

Do I care in 2024 that the firm thinks this is as bad as it gets, but by 2030 things will go just swimmingly? No. Of course not. I may get hit by a bus later today (I hope not).

What I am trying to say is that if you need multiple years to unscrew yourself, then I'll find something else to do with my capital and come back and have another look after you think you're all gussied up.

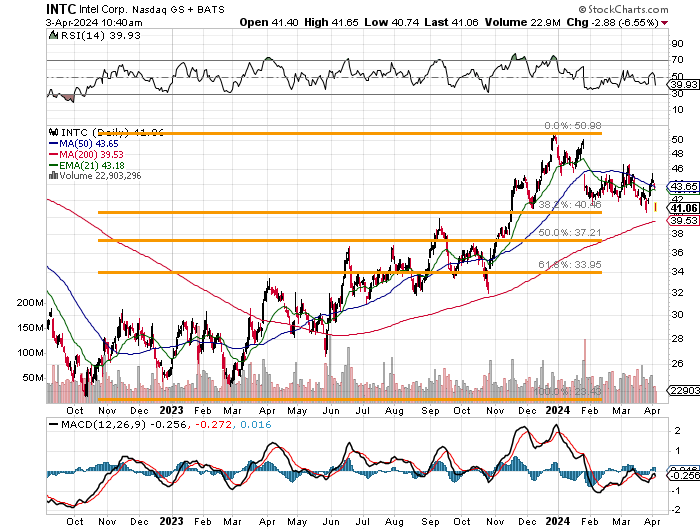

Readers will note that for the second time in less than a month, INTC is testing the 38.2% Fibonacci retracement level of the stock's October 2022 into December 2023 rally. Should that line crack, it's another $2 down to the stock's 200-day SMA (simple moving average). That's where the professional money also known as the "long and wrong" crowd will have to make a decision. Lose that line... Well, we'll think about that when it happens.

What I am trying to say is that if I were thinking about investing in Intel, it would have to be at a discount and it would not come above that 200-day line which currently stands at $39.53. A sale of the June 21st $39 puts for a rough $1.90 looks more attractive to me than an outright purchase of the equity.

The stock never goes that low? That's not a bad premium to take in. The stock does go there? Then the trader would be long the equity at a net basis of $37.10 in two and a half months.

At the time of publication, Stephen Guilfoyle was long AMD, NVDA equity.