Great Expectations: What to Look for From Nvidia and How the Stock May React

Nothing else matters Wednesday as the market waits to hear from the AI King and Jensen Huang. Here's everything you need to know, including how I'm trading it.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The day has arrived.

There are several other public corporations set to report quarterly earnings on Wednesday. There has been a plethora of Fed speakers out and about this week. There will be some fairly important macro out late this week. Right now, though, none of that matters. Right now, or later this afternoon, it will be all about Nvidia NVDA, the AI King and that firm's leader... CEO Jensen "The Fonz" Huang. Rock on.

It was just about a year ago that Nvidia released its fiscal first-quarter (April 2023, fiscal 2024) results that would blow the doors off of not just the company's share price but change the way financial markets behaved — and in some respects the way the economy works and will work. That day, Nvidia did more than beat top and bottom-line expectations, they provided guidance that simply crushed Wall Street estimates. They haven't stopped since.

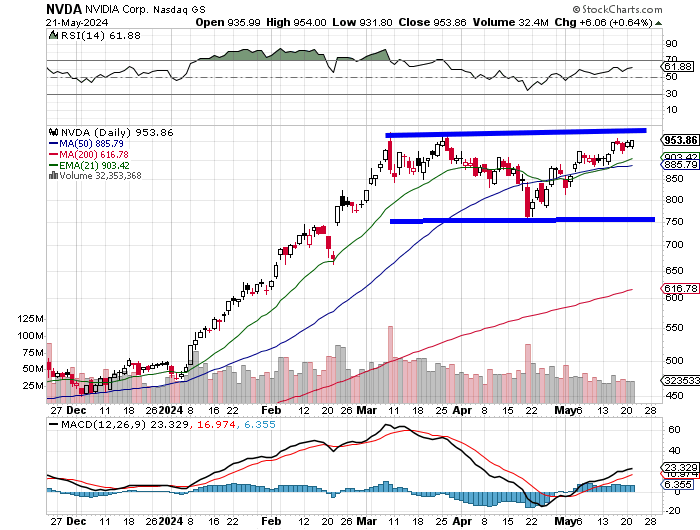

Over the past year, Nvidia has tacked on roughly $1.5T in market cap and now ranks as one of the most valued companies in the world at a market cap of $2.33T. Nvidia's trailing 12 months earnings per share is up some 617%, according to Bank of America, and the stock price surged 219% from $305.38 as of the close on May 24, 2023 to a high of $974 this past March 8. Since that high, the stock sold off 22.4% and then rallied 26.2% to Tuesday evening's closing price of $953.86.

Tuesday's News Flow

First, Micron Technology MU increased its capital spending forecast for this year to around $8B from $7.5B thanks to the need for high-bandwidth memory used in AI accelerators such as those designed by Nvidia. This bodes well for Nvidia earnings. One might think.

Then we were told by the Financial Times that Amazon's AMZN AWS had changed plans to use Nvidia's most advanced AI-capable chip, the Grace Hopper, and wait for the next great AI-capable chip from Nvidia, the Grace Blackwell. Nvidia, we were told, declined to comment. Hmm, that might not be so good.

Finally, after the bell, we were told by Reuters that Amazon had indeed not halted any existing orders for Hopper and the Blackwell order was in addition to existing orders and for a different project. Well, that's a horse of an entirely different color.

Great Expectations

"Moths, and all sorts of ugly creatures, hover about a lighted candle. Can the candle help it?"

- Charles Dickens, 1861

"For Nvidia is the flame, for we, the many of us, are but moths and all sorts of ugly creatures."

- Sarge, 2024

For the first quarter of fiscal 2025, consensus for Nvidia's financial results are for adjusted EPS of $5.58, and GAAP EPS of $5.21 on revenue of $24.65B. Should the sales number end up being accurate, it would reflect year-over-year growth of 278%. Not a misprint. This would be a deceleration (yes, a deceleration) from the 265% growth for Q4 fiscal 2024. Of the 38 sell-side analysts that I am aware of that follow Nvidia, 36 have revised their estimates higher since the quarter started.

Investors will be watching for margin and guidance. Gross margin printed at 76% this past quarter and 63.3% for the year-ago comparison. As for guidance, Nvidia has already guided towards a full-year GAAP gross margin of 76.3% and 77% adjusted. Operating expenses were seen at $3.5B (GAAP) and $2.5B (adjusted) for the full year.

Investors will look for affirmations of these numbers and perhaps some guidance on revenue or free cash flow generation.

Remember

For fiscal 2024...

Data Center drove revenue growth of 217% to $47.5B.

Gaming generated revenue of $10.4B, up 15%.

Professional Visualization produced revenue of $1.6B, up 1%.

Automotive "drove" sales of $1.1B, up 21%.

The trick will be maintaining Data Center growth while Gaming tries to catch up. Gaming did see 56% year-over-year growth for Q4 over the year-ago comp. Professional Visualization and Automotive are mere contributors at this point.

My Thoughts

Needless to say, I'm coming in long. I did take some profits a couple of months ago. That looked smart for a little while. Maybe not so much now. So, yes...I am coming in long, but I'm not coming in heavy.

The stock now trades at 38 times forward-looking earnings, 38 times sales and 54 times book, but runs with a five-year expected PEG ratio of "just" 1.25. Undervalued? Seems crazy with numbers like that, but we shall see very shortly.

Just 1.1% of the entire float is held in short positions. Wow. That takes some guts.

The stock enters into this release rather close to the resistance provided by the top end of this basing period of consolidation that NVDA has been "mired" in since early March. Relative strength is slightly stronger than neutral.

The daily Moving Average Convergence Divergence (MACD) turned for the better in late April and really looks very bullish right now with the 12-day exponential moving average (EMA) above the 26-day EMA and the histogram of the 9-day EMA well entrenched in positive territory.

What I think is this. Should the stock take and hold the $974 high, which is now the pivot, that not only unlocks prices above $1K, but price targets up around $1,120, in my opinion. Should this afternoon go poorly... well, you don't need to be told, you can see the 200-day simple moving average (SMA) for yourselves.

Hopefully we're not all playing Chutes and Ladders later. Well, maybe Ladders.

More Sarge:

- Nvidia Earnings, FOMC, Unpleasant Breadth, Shrinking Disney, Investing in SoFi, Palantir

- Lam Research Plans a Buyback and Stock Split: Here's When to Trade It

- We Are Only in the Early Innings of Palantir's AI-Fueled Run

At the time of publication, Guilfoyle was long NVDA and AMZN equity.