Lam Research Plans a Buyback and Stock Split: Here's When to Trade It

This firm is well run. The business is efficient. On these matters, I have no doubt.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Lam a Damma Ding Dong!

Whoa doggie. Now that's news. The news on Tuesday morning was almost shocking. Lam Research LRCX, a former Sarge favorite - that handed me one heck of a year several years back - announced a new $10B share repurchase authorization, in line with the firm's plan to return 75% to 100% of free cash flow to shareholders through cash dividends and buybacks.

Currently Lam Research pays shareholders $8 per year per share, which sounds like a lot, but given the roughly $950 last sale, yields just 0.84%. That brings us to our next item.

Not only did Lam authorize a huge buyback, but the firm also announced a 10 to 1 stock split expected to be affected after the close of business on Wednesday, October 2nd. Sashes will open on Thursday, the 3rd at the post-split price.

The firm released information that stated, "As a result of the stock split, proportionate adjustments will be made to the number of shares of Lam Research's common stock underlying the company's outstanding equity awards, equity incentive plans, and other existing agreements, as well as exercise or conversion prices, as applicable."

Interestingly...

The shares have not moved much this morning and are down from a surge on the open in New York. Then again, the firm's competitors, KLA Corp KLAC, Applied Materials AMAT, and ASML Holding ASML are all trading 1% to 2% lower relative to Monday afternoon's closing prices. Lam currently trades at 26 times forward looking earnings, which is not terribly expensive.

ASML trades at 41 times, while KLAC trades at 28 times and AMAT also trades at 26 times. Lam trades 8 times sales, 15 times book and runs at a very healthy PEG ratio of 2.54. There is no significant short interest to speak of (1.9% of the float).

The Nuts & Bolts

About a month ago, Lam reported its fiscal third quarter numbers. The firm posted an adjusted EPS of $7.70 on revenue of $3.79B, beating expectations for both top and bottom-line performance. It should be noted that the sales print reflected a year over year contraction of 2.1%. This was the fifth consecutive quarter of year over year sales contraction, though the slowdown has been slowing down itself.

Over the past twelve months (as of the last earnings report), Lam had generated operating cash flow of $4.913B, including $1.385B for that most recent quarter. This is impressive. After accounting for capital expenditures, FQ3 free cash flow printed at $1.281B, while twelve-month FCF printed at $4.528B, so at least readers know that the firm is a cash flow beast and intends to return that cash flow to shareholders.

As of the end of the March quarter, Lam had a cash position of $5.672B and inventories of $4.323B, leaving current assets at $12.488B. Current liabilities printed at $4.43B, including just $505M in short term debt, but $1.602B in unearned revenue, which is not a true financial liability. This puts the firm's headline current and core ratios at a very healthy looking 2.82 and 1.84, respectively. After adjusting for unearned revenues, these ratios rise to a quite robust 4.42 and 2.89.

Total assets amounted to $18.28B including $1.77B in goodwill and other intangibles. At less than 10% of total assets, this is not a worry. Total liabilities ex-equity comes to $10.258B. This does include $4.478B in long-term debt, which is something the firm could pay off out of cash if it had to. This is one fine balance sheet.

My Thoughts

This firm is well run. The business is efficient. On these matters, I have no doubt. Initiating a large buyback makes sense as the firm transitions from a "growth" type stock to more of a "value" name focusing more on profitability, free cash flow, and returning cash to shareholders than in driving sales.

I don't see gains in market share unless there is to be a bout of M&A across the industry... that said, they're all large. Very large. KLA Corp is the smallest among the four with a market cap of close to $105B.

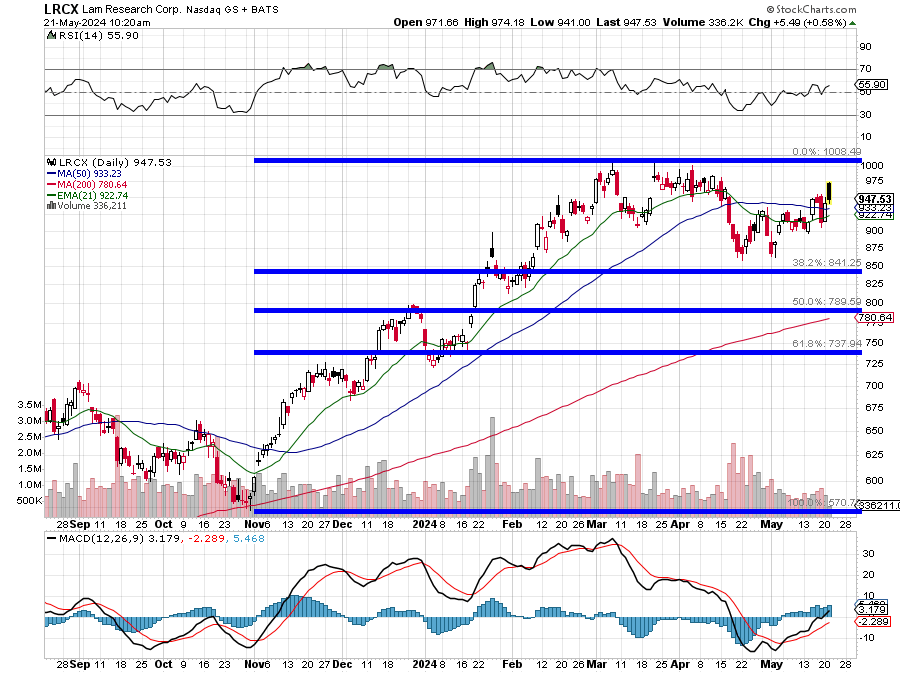

Readers will see that LRCX rallied from late October into early March and then went into a basing period of consolidation. The $1,008 level of resistance has been tested four times and held. Support at $858, just above a 38.2% Fibonacci retracement level of the entire rally, has also held on several attempts to crack to the downside.

The shares have recently retaken their 21-day EMA (exponential moving average) and more importantly, their 50-day SMA (simple moving average), while relative strength has poked its head up and the daily MACD (moving average convergence divergence) has started to look a lot better.

I would be lying if I said I was not intrigued by the 10 for 1 stock split. I know, stock splits don't do anything for market cap in terms of the math involved, but they do invite a wider swath of investors to participate.

I probably will think about entry at the 50-day line, with an intention to add at established support and then at the Fib level if the stock goes that way. If it does not, I would think to get involved on momentum above established resistance on a take and hold move, but not before.

At the time of publication, Stephen Guilfoyle had no position in the securities mentioned.