We Are Only in the Early Innings of Palantir's AI-Fueled Run

You will search for a long time before you find another balance sheet as clean and strong as this one. Here's my latest view, game plan, and price target on this long-time holding.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

On Monday evening, former Stocks Under $10 portfolio core holding and long-time Sarge favorite Palantir Technologies PLTR released its first-quarter financial results. For the period ended March 31, Palantir posted adjusted earnings per share of $0.08 (GAAP EPS: $0.04) on revenue of $634.338M.

The adjusted earnings print met Wall Street expectations, the GAAP print beat by a penny, and the revenue numbers exceeded Street projections by a smidge. Revenue generation was good enough for year-over-year growth of 20.8%, which reflected a third consecutive quarter of accelerating sales.

This was Palantir's sixth consecutive quarter of GAAP profitability. U.S commercial customer count grew an astounding 69% to 262, while U.S. commercial remaining deal value increased 74%.

Commercially driven revenue growth came to 27% over the same quarter a year ago. Total customer count grew by 42%. All government-driven revenue advanced 16% versus the year-ago comp to $335M, while U.S. government-driven revenue increased 12% to $257M.

Operations

As revenue was growing 20.8%, the cost of revenue increased 8% to $116.256M. This left a gross profit of $518.082M (+24.1%), as gross margin widened to 81.7% from 79.5%. Total operating expenses grew 5.8% to $437.201M, leaving GAAP operating income of $80.881B (up from $4.115M).

After accounting for interest taxes, and other income/losses, Palantir was left with net income attributable to shareholders of $105.53M (+528%, not a misprint). That works out to GAAP EPS of $0.04, up from $0.01 for the year-ago comp.

Once stock-based compensation expense of $125.651M and payroll taxes related to this compensation of $19.926M are added back in, adjusted operating income becomes $226.458M (+81%) and adjusted EPS becomes $0.08, up from $0.05.

Key Quotes

Honestly, I think those considering an investment in Palantir need to read and understand the following quotes taken from Monday night's releases.

From the Shareholder Letter

CEO Alex Karp:

"Other companies engage in intricate and elaborate efforts to sell and market their offerings. Their resources are focused on marketing at the expense of actually constructing the software and building the systems that they hope to sell. We have taken a different approach and are now investing even more heavily in simply letting potential partners use our software in order to decide what works and what does not for themselves."

From the Earnings Call

When I was seventeen years old, I shipped off to Parris Island and took my place upon the hallowed yellow footprints where the greatest warriors in the history of the planet have stood. Yeah... Palantir is using a different kind of "boot camp" involved in the development of a different kind of warrior to sell its AI-infused platforms.

CTO Shyam Sankar:

"Now there's this thing that some companies have started saying where only 10% of my customers have data that's even AI-ready to begin with. I think that's completely wrong. Maybe they don't have something to sell in the present moments where they're trying to sell the past. But if that was right, how is it that in a single-day boot camp, we're able to add value on-top of our customers' messy extant data. Ultimately, software that works, works. And to the present moment, I'm focused on helping enable builders in the context of the enterprise."

CEO Alex Karp:

"The bootcamps also have, quite frankly, another massive advantage because de facto it sets a standard that will be very hard for any other company to meet. So, even if you don't buy our product, you de facto have locked in an idea of what's possible. And that means that at some point when you go try your own thing and it fails, you've seen, okay, well, I've seen the art of the possible, and therefore I'm going to go buy it from Palantir at some point in the future."

CEO Alex Karp:

"I don't believe we have competitors. So, I don't believe in the U.S. commercial market we have competition. I don't believe in the U.S. government market we have competition. I don't -- I think that's the reason Ukraine and Israel bought our product. We are differentiated because in order to actually make AI work, you need an ontology. No one has an ontology."

Guidance

For the current quarter, Palantir sees revenue of $649M to $653M with Wall Street looking for $653M. This was seen as somewhat disappointing overnight. Adjusted operating income is seen at $209M to $213M.

For the full year, the company is projecting revenue of $2.677B to $2.689B. This is an increase, but again, the Street was looking for something around $2.69B.

Palantir now expects U.S. commercial clients to drive revenue of $661M, which would be growth of at least 45%. Full year adjusted operating income is seen at $868M to $880M. Free cash flow is seen for the full year at $800M to $1B as well.

After all of that, Palantir still expects to remain profitable on both a GAAP operating and GAAP net income basis for each quarter of the year.

Fundamentals

For the quarter reported, Palantir generated operating cash flow of $129.579M. Add to that number $21.719M in employer payroll taxes related to its stock-based compensation expense, and then subtract capex spending of just $2.664M. That leaves free cash flow of $148.634M. Palantir does not return capital to shareholders.

Moving on to the balance sheet, Palantir ended the period with a cash position of $3.868B and current assets of $4.436B. Current liabilities add up to just $750.553M, including $237.634M in deferred revenue, which is not truly a financial obligation. There is no short-term debt on the books. This puts its current ratio at an almost absurdly robust 5.91. Once adjusting for deferred revenues, the current ratio rises to a jaw-dropping 8.65.

Total assets amount to $4.807B. Palantir claims no value for intangible assets. We appreciate that, but with a balance sheet like this, there is no need to try to puff up the assets side of the balance sheet. Total liabilities less equity comes to $945.907M. There are some more deferred revenues in there, but no long-term debt. No debt of any kind.

You may search high. You may search far. You may search all day or all week. You will search for a long time before you find another balance sheet as clean and strong as this one. This balance sheet is a reason, in my opinion, to invest in this name, on its own merits.

Wall Street

There is some difference of opinion on Palantir. Remember, I exclude sell-side analysts ranked at below 4 stars (out of 5) by TipRanks. Readers really should pay attention to ratings of sell-side analysts as many of those often favored by CNBC and other outlets are ranked at very few, and in some cases, zero stars.

Since Palantir's earnings were released Monday night, I have come across just eight highly rated sell-side analysts that have opined on the stock. Among the eight, there is one "buy" rating, five "hold" or hold-equivalent ratings and two "sell" ot sell-equivalent ratings. Two of our "holds" did not bother to set price targets, so we are working with just six of those.

After allowing for changes, the average price target across those six is an even $21 with a high of $35 (Dan Ives of Wedbush) and a low of $9 (Rishi Jaluria of RBC Capital). After omitting these two as potential outliers, and in this case, they both really do appear to be, the average target across the other four stands at $20.50.

My Thoughts

It's no secret, I am a fan of Palantir. I have been with PLTR through the Stocks Under $10 portfolio and through my own account after that, since the stock was trading in the mid-single digits.

I really do not think that we are in the seventh, eighth or ninth innings of Palantir's run. I honestly believe we are in the second or third inning and that Palantir eventually becomes a, if not the dominant player in big data analytics, in data-supported security and surveillance and in all that protecting nations and businesses requires.

Oh, did I mention the cash flows, or the balance sheet? Talk about a fortress.

The fundamentals, outside of valuation, which at 70 times forward-looking earnings, 26 times sales, and 16 times book, are tricky. Do those valuations not tell us something though? Do they not tell us that these guys are so far ahead on AI-supported data-driven software that Karp is right... There really is no competition.

Sell this name because that's what the algos are doing right now? Do I look like I was born yesterday?

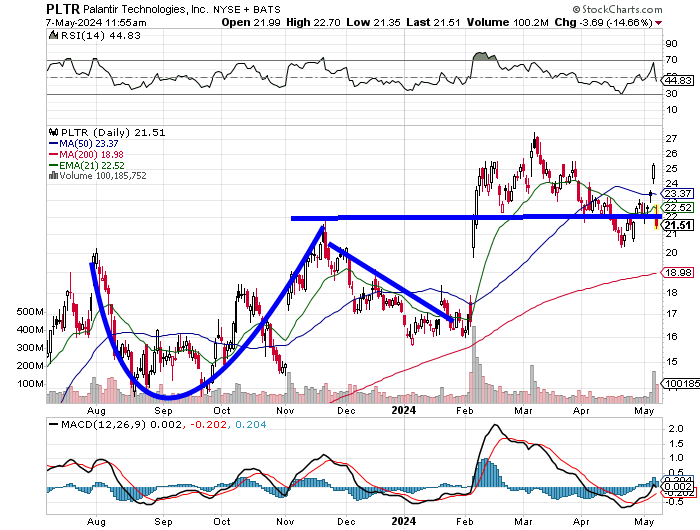

Okay, with Tuesday's almost 15% beat-down, the stock has given up both its 50-day simple moving average (SMA) (that forced some risk managers to pressure some portfolio managers to reduce exposure) and 21-day exponential moving average (EMA) (wringing out some swing traders). Understandable. The stock had broken out in early February from a cup-with-handle pattern bearing a $22 pivot. We had a $27 target at that time. The stock apexed at $27.50 in March.

That old pivot line has become something of a battleground, since cracking in mid-April. Even with Tuesday's pounding, RSI (Relative Strength Index) is neutral and the daily MACD (Moving Average Convergence Diveregence) is still bullish in posture.

I would expect that I will add to my long position at some point Tuesday afternoon and add more if the stock weakens from there. Only a break of that 200-day line could get me to sell anything and that's only because I know that "old Wall Street" would sell it down a few bucks from there.

It pays to know these guys inside and out. I will be setting a new (higher) price target at this time.

Palantir Technologies (PLTR)

Price Target: $29

Pivot: 50-day SMA (currently $23).

Add: Down to 200-day SMA (currently $19).

Panic: On a break of the 200-day SMA.

At the time of publication, Guilfoyle was long PLTR equity.