What We're Watching for on Four Holdings as Single-Family Housing Starts Climb

We’ll acknowledge potential near-term noise, but focus on the longer view for these holdings.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The September Housing Starts and Building Permits report is out and, while it showed overall housing starts were slower compared to August, single-family housing starts in September climbed month over month.

Not only were single-family housing starts up compared to September 2023, but the September 2024 increase continues the sequential improvement of the last few months. The timing on this can be traced back to falling mortgage rates as the market prepared for and then eventually received the Fed’s first rate cut.

The September single-family housing data, both for the fresh starts and ones under construction, support forecasts by Lennar LEN, KBHome KBH and other homebuilders for stronger 2H deliveries compared to 1H 2024. We could see some disruption in the October housing data due to recent hurricanes, but our focus will remain on the Fed getting monetary policy back to more neutral footing over the coming quarters. Those moves should drive mortgage rates lower, stimulating further housing activity and demand for Builders FirstSource BLDR and the residential construction sides of United Rentals URI, Vulcan Materials VMC and Waste Management WM.

That’s the medium- to longer-term view.

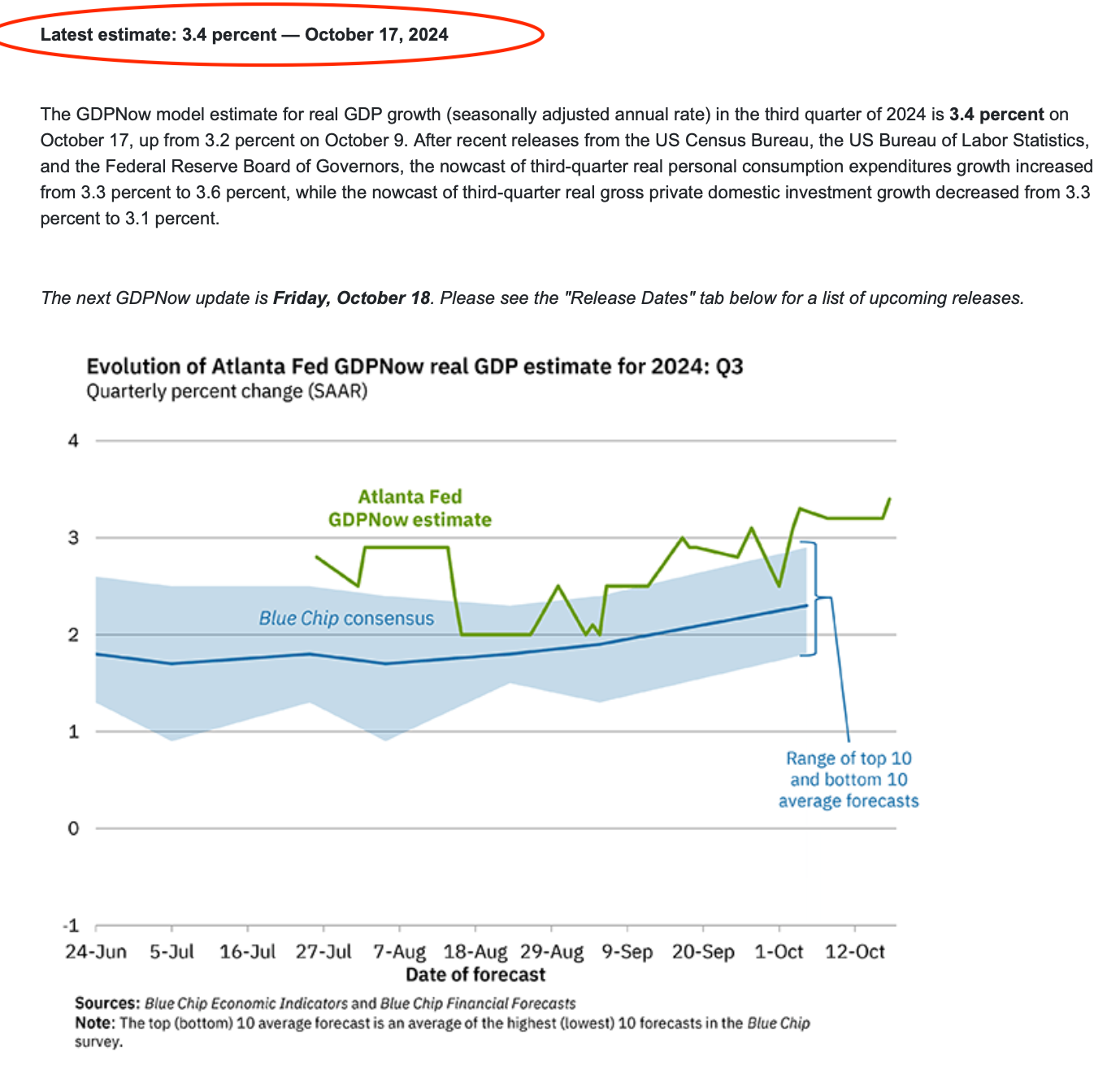

In the short term, we could see those holdings swing back and forth, should the market question the pace of expected rate cuts. Thursday's update for the Atlanta Fed GDPNow model pegged 3Q 2024 GDP at 3.4%, up from its prior forecast of 3.2%. That fresh print speaks more to a no-landing scenario for the economy. More folks working and making more money as mortgage rates improve is a pretty good recipe for the housing market.

However, mixing that updated rolling GDP forecast with some September inflation data that was not moving in the right direction is raising renewed questions about the cadence of Fed rate cuts. This explains why our shares of BLDR and URI traded off on Thursday.

While our thinking is that the Fed’s preference is to loosen monetary policy over the coming quarters, we also think the pace could be somewhat slower than the market expects. Even so, the focus for us remains the direction of Fed policy and the corresponding impact on mortgage rates and housing activity over the next several quarters.

Complicating the near-term view will be October data that will be disrupted by Hurricanes Helene and Milton. Much like we will, the Fed is likely to account for that in its policy deliberations. We expect to hear that message from Fed speakers on Friday and next week, but we also suspect their overall tone will be more dovish than it has been compared to earlier this year.

As we listen to their comments next week also brings the September PCE Price Index data and the Flash October PMI data from S&P Global. Barring a head-turning PCE print should we see a larger-than-expected decline in the Flash October data, we could see the market’s enthusiasm for rate cuts return. We’ll continue to stick to the medium- to longer-term outlook for interest rates and what that means for our four holdings.

More Pro Portfolio

- Why We Opened a Position in a $8.4 Billion AI Name

- Weekly Roundup: Portfolio Begins October With Big Gains and Big Moves

- We Did the Homework for You: Here're the Top Stories on Our Investing Themes

At the time of publication, TheStreet Pro Portfolio was long BLDR, URI, VMC and WM.