Why We Opened a Position in a $8.4 Billion AI Name

Accelerating AI adoption in the enterprise space mixes well with this subscription business.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Earlier today, we started a new position in the shares of Elastic ESTC with a One rating and a $105 price target. Let’s dig into our reasons for making that decision and why we see the shares moving higher in the coming quarters.

The 411 on Elastic

While it refers to itself as the “search AI company,” Elastic is best known as a leading enterprise search engine that offers three search-powered solutions:

- Enterprise search provides a search platform for building search AI applications. Use cases include generative AI and retrieval-augmented generation, search applications and foundational capabilities for building search experiences to support websites and portals, e-commerce, mobile app search, customer support and workplace search.

- Observability enables unified analysis across the IT ecosystem of applications, networks and infrastructure.

- Security provides unified protection to prevent, detect and respond to threats. Its AI-driven security analytics solution includes integrations to network, host, user and cloud data sources, as well as workflow and operations, shareable analytics, incident management and investigations as well as endpoint security and cloud security.

One thing we do not like is that, despite those solutions, at least for now, Elastic reports its SEC documents in one reporting segment. It does share, however, that the U.S. is about 60% of its revenue.

Getting back to the company’s solutions, they are available as a hosted, managed service across major cloud providers, including Amazon Web Services (AWS), Google Cloud and Microsoft’s Azure in more than 55 public cloud regions globally. Customers can also deploy Elastic’s platform across hybrid clouds, public or private clouds, and multi-cloud environments.

Leveraging these platforms, Elastic’s customer count has mushroomed to more than 21,200 exiting its July quarter, but even more impressive is its growth in customers with over $100,000 in annual contract value (ACV). The number of those customers reached 1,370 at the end of July, continuing a steady growth rate over the last few years. Paired with similar gains in customers with ACV over $10,000 has led the average subscription revenue per customer to climb to about $16,368 compared to $12,868 exiting its fiscal 2022. Customers include Comcast CMCSA, Booking.com BKNG, BMW, Orange and a variety of others across as many sectors.

Parsing those figures, we find Elastic has been growing its revenue per customer faster than its overall customer base, which has grown consistently. This tells us that customers have been adopting more of Elastic’s products across its Elastic Cloud, Elastic Stack and Elasticsearch Relevance Engine & Gen AI applications. Exiting the July quarter, Elastic had over 1,300 customers using Elastic Cloud for GenAI use cases, with about 200 falling with ACVs of more than $100,000. That has helped make Elastic Cloud the fastest-growing business at the company over the last eight quarters.

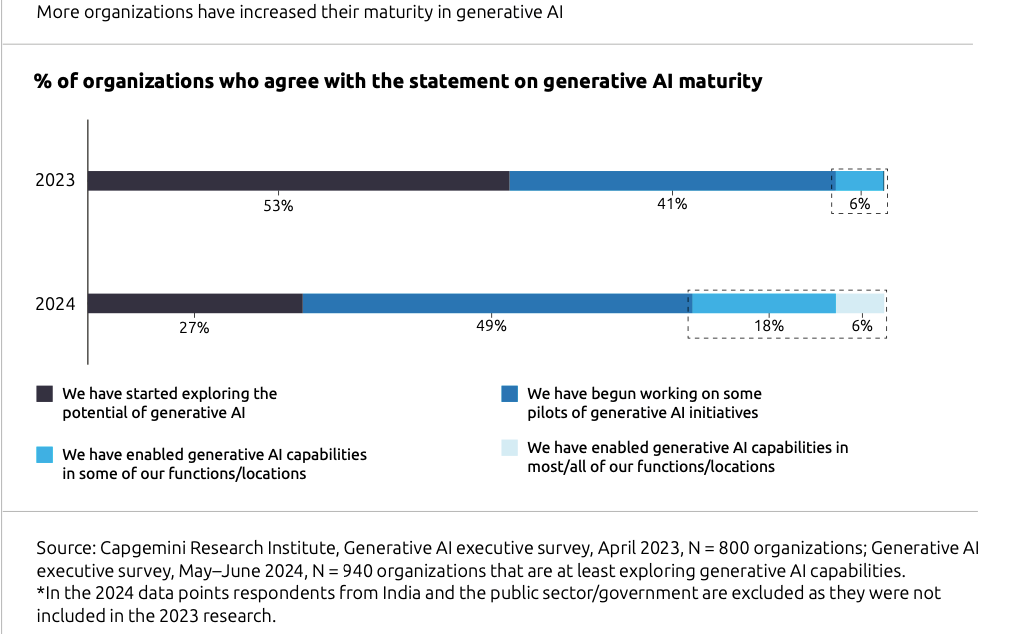

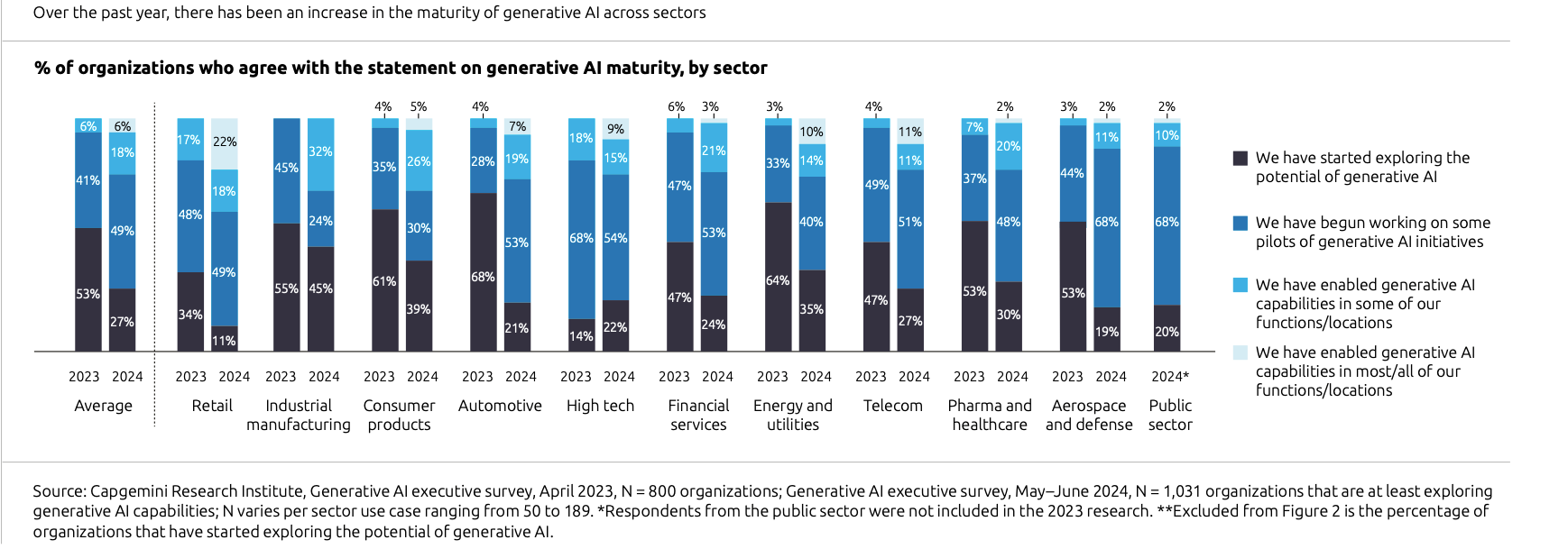

We should not be surprised by that given the data compiled by CapGemini that showed the rising adoption of AI in the enterprise and across a wider array of sectors. It was this data, and the price lift associated with generative AI applications reported by ServiceNow NOW that led us to lift our price target for NOW shares. We suspect the same impact is being had with Elastic’s business and the addition of the shares bolsters our exposure to the enterprise software market.

Other findings from a recent EY executive survey pointed to a nearly twofold increase in AI investments in the next year. The survey also revealed that half of survey respondents expect to spend more of their budget on AI in the coming year. We see this signaling that, despite all of the AI headlines and hype, we are still in the relatively early innings of AI adoption.

What we like even more about this is Elastic’s subscription-based business model, which accounts for just over 93% of its total revenue stream. As we’ve discussed before with other companies, this affords not only good visibility but predictable cash flow and earnings. Moreover, the gross margins associated with the subscription business are above 80%, which helps explain the rising margin profile and EPS as that business has come to account for a greater percentage of overall revenue.

Why Now With Elastic shares?

When we look at the chart of ESTC shares, we see they were trading between $95 and $125 over the last several months, until the company revised its fiscal 2025 revenue to $1.436 billion to $1.444 billion, compared to its previous guidance of $1.468 billion to $1.48 billion. In response to that 2% to 2.5% downward revenue revision, ESTC shares plummeted just below $70 and have since started to make their way back.

In response, we saw some tinkering with calendar EPS expectations but not enough to warrant such a drop in the shares, given Elastic is expected to grow its bottom line by more than 60% this year and by nearly 25% next year. That puts 2025 consensus EPS at $1.76, up from $1.43 this year and on a path for $2.09 in 2026. Over the 2023 to 2026 time frame, the thinking is that Elastic will grow its EPS by a compound annual growth rate of 33%. As Elastic scales its business further, we should start to see more operating leverage across its sales and marketing and R&D spending, which combined account for about 60% of its revenue.

With that in mind, we’re establishing an initial price target of $105 for ESTC, which equates to a PEG ratio of 1.5x expected calendar 2026 EPS near $2.10.

Some on Wall Street have more aggressive price targets, with some between $120 to $130. Those equate to higher PEG ratio multiples between 1.7x to 1.9x. We’d rather take a more conservative approach and revise our price target should Elastic deliver faster customer and ACV growth, driving stronger EPS generation in the process. In terms of potential downside, the shares bottomed out near $70 in November 2023 and early September, offering indications of support.

With those figures, we see a net upside of just under 20%, which is enough to warrant a One rating, especially as enterprise customers look to accelerate their AI adoption in the coming quarters. We’ll set an initial panic point at $65 and look to move it higher as the shares move closer to our target price. As we add ESTC shares, we would note their beta is 1.3, which means they are more volatile than the market, which explains the wider-than-usual range for our initial panic point.

Given the potential market pullback that led us to add shares of the ProShares Short S&P 500 ETF SH on Thursday, we’d be inclined to more aggressively add additional ESTC shares closer to $75.

When it comes to potential risks, one sign that would lead us to reconsider owning the shares would be if either Elastic’s customer count or its subscription revenue per customer stalled. Another item we’ll be watching because of Elastic’s geographic mix, with 40% of its revenue outside of the U.S., is the dollar and corresponding foreign exchange impact.

The Likely Question

When we look at Elastic’s business, you’re likely to have the same question we thought about while doing our ESTC homework: Could the company be a takeout candidate?

The company’s $8.4 billion market cap and its $1.15 billion in cash and marketable securities could be easily swallowed by the likes of Alphabet GOOGL, Microsoft MSFT and potentially Salesforce CRM or Oracle ORCL. However, Google’s global search market share of more than 90% could keep it out of the running and a pick-up of Elastic by Microsoft would not only augment its far distant position in search with roughly 4% of the market, Elastic could also be integrated into its Azure and security offerings.

To be clear, while Elastic might land on some M&A radar screens, that is not a reason behind our adding ESTC shares to the Portfolio. But if the company were to be acquired, the odds of that transaction delivering a nice return for the Portfolio are pretty good.

More Pro Portfolio

- We're Locking in Big Gains on These Two Holdings

- Monthly Roundup: After a Great September, We Await Opportunities in October

- Market’s P/E Is Stretched — And So Is Its Dividend Yield

At the time of publication, TheStreet Pro Portfolio was long ESTC, AMZN, GOOGL, MSFT and NOW.