Weekly Roundup: Portfolio Begins October With Big Gains and Big Moves

Two new positions, large gains locked in, several price target increases, and meaningful outperformance from several names highlighted the start of the month.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

While it looked a little wobbly at one point, the stock market had a positive start to the final quarter of the year this week with all four major market indexes moving higher. Below we’ll discuss how this led the portfolio to notch further gains this week, but the continued rise in the market has brought relative strength index (RSI) levels for the S&P 500 and Nasdaq Composite that much closer to being overbought. The S&P 500’s continued climb has also pushed its already stretched valuation even higher, raising the stakes for corporate earnings and guidance over the coming weeks.

These and other factors led us on Thursday to begin a new tactical position in the ProShares Short S&P500 ETF SH to hedge the portfolio against a potential pullback in the market in the coming weeks. To those market dynamics, we can add what we saw in the September CPI and PPI data that showed core inflation not moving in the right direction for a second consecutive month.

Those data points build on the argument stemming from the September Employment Report and the 3.2% figure published this week by the Atlanta Fed’s GDNow model that the Fed may not deliver as many rate cuts as the market expects this year. On Thursday, Atlanta Fed President Raphael Bostic shared that he is "… totally comfortable with skipping a meeting if the data suggests that’s appropriate…”

When we discussed the September PPI data on Friday, we also said that between now and the Fed’s next policy announcement we will have several more pieces of September data and a few for October in hand. We suspect some of the pricing data in that October data could be influenced by the rebound in oil prices that has unfolded amid renewed Middle East tensions. Over the weekend, we’ll be monitoring Israel’s expected response to Iran’s missile attack earlier this month and whether it raises the stakes for that conflict even further. If it does and oil prices move up further, it would be another reason to suspect October inflation data may move higher as well.

As we think about that upcoming data and the potential pace of rate cuts to come, should the Fed opt to lean more dovish and loosen monetary policy further, our interest rate-sensitive positions will benefit. If, however, the Fed opts to take a more measured approach than the market expects, we have our shopping list of stocks and a plan to follow. We will continue to focus on companies with strong tailwinds and superior earnings prospects as well as favorable risk to reward entry points in their shares.

We saw that in Elastic N.V. ESTC and that led us to start a new position in the shares on Friday. The addition of ESTC and SH this week brings the number of holdings in the portfolio back to 29, a tad higher than we’d prefer. We will remain disciplined investors and if that means having to make some tough choices to ensure we have sufficient room to make the right moves for the portfolio that’s what we’ll do.

Catching Up on the Portfolio This Week

The market put in another winning weak, starting the last quarter of the year in the green. However, the portfolio started with a bang following meaningful outperformance from half a dozen names. In the pole position this week was Nvidia NVDA, followed by another robust week for Axon AXON, Trade Desk TTD, and United Rentals URI. Late-in-the week surges in Bank of America BAC and Morgan Stanley MS made them outperformers as well.

Laggards for the week included Alphabet GOOGL, likely due to breakup headlines, but we shared our view on that with you here. We don’t see any near- or medium-term operational issues and we’re inclined to pick up shares at the right price. Lockheed Martin LMT shares closed lower, but candidly given the strong run they've had since late July, they were due for a breather.

We sold some LMT shares early in the week, locking in a nice gain of more than 30% for the portfolio. The next catalyst we’re watching is the company’s updated multiyear delivery schedule, which may lead us to revisit our recently increased price target of $625. Alongside that Lockheed trim, we rang the register on another profitable slice of Axon shares. We discussed why prudent portfolio management led us to make that move in the trade Alert and also during Wednesday’s Quarterly Members-Only call.

Tuesday, we discussed why we are sticking with PepsiCo PEP as we move deeper into its seasonally strongest quarter. Wednesday was when we tackled the headline risk with Alphabet shares, explaining why any impact won’t be felt for some time. We also reviewed the September revenue report from Taiwan Semiconductor TSM discussing how it supports several of our holdings, but especially Nvidia and Marvell MRVL.

Thursday was a busy day for us. We not only started a new position in the ProShares Short S&P500 ETF SH to help hedge our returns against a growing risk of a market pullback. Later that day we boosted our price targets for ServiceNow NOW, Mastercard MA, and the First Trust Nasdaq Cybersecurity ETF CIBR.

On Friday, in addition to explaining how quarterly results from JPMorgan Chase JPM and Wells Fargo WFC support our stance on Bank of America BAC and Morgan Stanley MS, we also started a new position in Elastic N.V. ESTC. Our initial rating for ESTC is One and our price target is $105. Be sure to read our deep dive into the company and our rationale for starting the position.

Now let’s take a quick look at what Wall Street had to say about our holdings this week:

JPMorgan cut its PEP target price to $183 from $185, while we kept our target at $185.

RBC raised its price target for LMT shares to $675 from $600, believing that the monetary easing cycle will support the company's stock. We’re more focused on the upcoming multi-year delivery schedule update, but a lower-rate environment would be an incremental positive.

Goldman Sachs upped its price target on Nvidia to $150 from $135 and kept its Buy rating on the stock. On Thursday, Morgan Stanley reiterated Nvidia as a top pick. Several weeks back we increased our NVDA target to $155, and September-quarter revenue this week from TSM discussed plus September data from Hon Hai supported that decision.

Meta received several price target increases this week, which follows our recent boost to $630 from $575. Cantor Fitzgerald lifted its META target to $670 from $660 while KeyBanc raised its to $655 from $560 and maintained its Overweight rating.

Truist raised the firm's price target on United Rentals to $954 from $873 and reiterated its Buy rating on the shares. Citi raised its price target on United Rentals to $930 from $860 and keeps a Buy rating on the stock.

Trade Desk got some love from Macquarie and KeyBanc as they both lifted their price targets to $130 from $115. Earnings from Netflix NFLX are a potential catalyst for us to revisit our $120 target.

Scotiabank started coverage on Amazon and Google with Outperform ratings.

Pivotal Research started AMZN at a Buy with a $260 target.

This Week's Portfolio Videos

We cover a lot of ground during the week in our Daily Rundowns. If you happened to miss one or more of them, here are some helpful links:

Monday, October 7: Today's Profitable Trades and Our Plan for This Week

Tuesday, October 8: Why We’re Waiting on This Holding's Earnings Call

Wednesday, October 9: Reviewing a Stellar Q3 and Looking Ahead on Our Members-Only Call

Thursday, October 10: Why We Added More Protection With a Market Hedge

Friday, October 11: More Thoughts on the Newest Name to the Portfolio

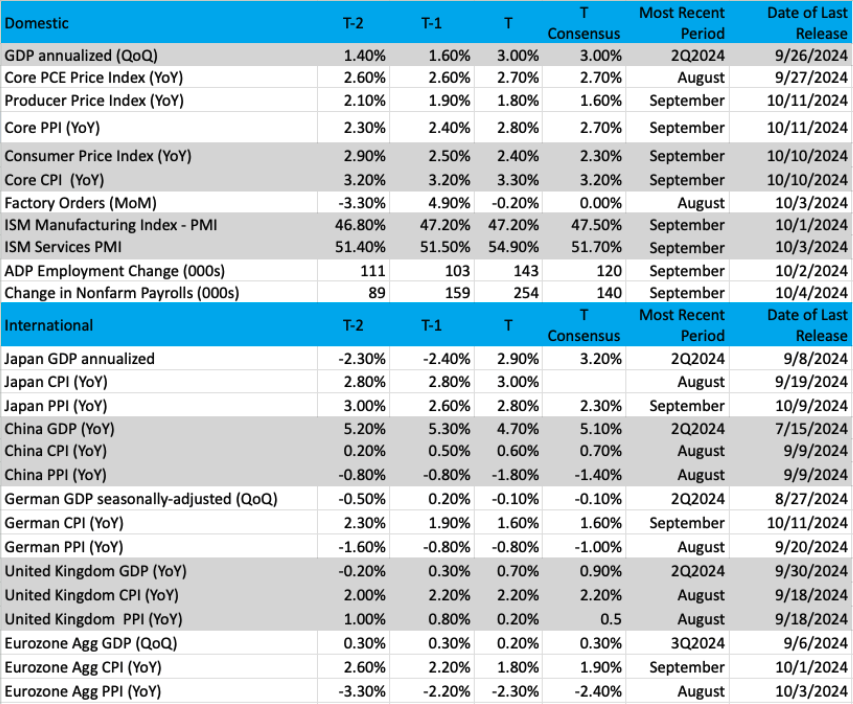

Key Global Economic Readings

(Note: T is the most recent period, T-1 is the prior period's reading and T-2 is two periods back, the intent being to illustrate any trends)

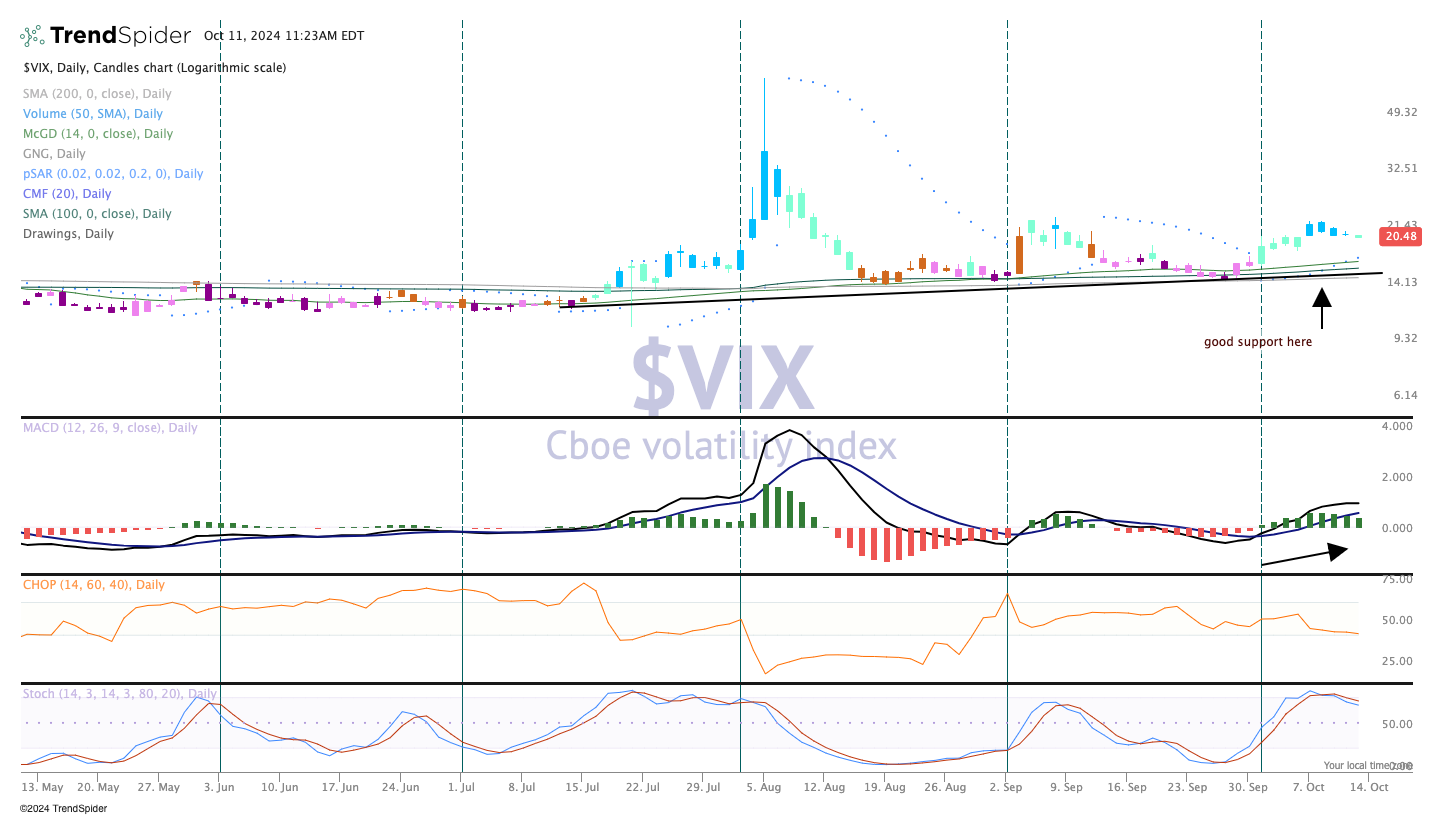

Chart of the Week: The Volatility Index (VIX)

Market volatility is certainly on center stage until the end of this year. With a crucial election coming up in just under a month and no real favorite in sight, the VIX is showing the uncertainty that is often the guise of real sentiment.

What does that mean?

Fear is present when unknowns and uncertainties are out there, and that includes now. Who will win the election? What policies will come forth to help/hurt the economy? Is the national debt ever going to be addressed? How about inflation, growth, and jobs?

These questions seem to be asked repeatedly with the same answer: Who knows? Market volatility tends to deflate when the uncertainties disappear, but stays elevated as it is now until that time arrives. The VIX, which is the market volatility index, currently portrays some angst. With a reading of 20%, the market is pricing in a great deal of movement in the markets, both up and down.

Now, with the VIX being higher it simply means the range in the market is expanding. In other words, larger price moves up and down. Is that something to worry about? Well, for some traders/investors large moves down cause a great deal of worry that could lead to large losses and despair, and this despite the fact higher volatility means the markets can also rise sharply.

The current volatility situation with the elevated VIX remains a caution flag for the markets, despite a couple of the indexes recently hitting new all-time highs. Could that caution disappear? Absolutely yes, but we would like to see fewer intense news events (Middle East drama, etc.), which can sound the alarm bells to start selling stocks.

The VIX shows an uptrend, but unless it moves significantly past the 24 area, we do not expect to see much damage to the markets. In general, the VIX trends down over a longer period, and short-term spikes up become a great opportunity to add to your holdings. We can expect that situation to happen again over the next few weeks but buckle up for a bumpy ride to the end of the year.

Other charts we shared with you this week were:

Monday, October 7: S&P 500 - S&P 500 Muscles Its Way Higher

Monday, October 7: Applied Materials (AMAT) - This Tech Position Is Waiting for Momentum to Arrive

Tuesday, October 8: First Trust Nasdaq Cybersecurity Fund (CIBR) - It Would Be a Crime to Ignore This Position

Wednesday, October 9: AMD (AMD) – AMD Remains in Our Sights

Thursday, October 10: Morgan Stanley (MS) - This Portfolio Holding Sits on Top of All the Bank

The Week Ahead

Coming off a big week of September inflation data, we’ll be waiting for the next update to the Atlanta Fed GDPNow model, which stood at 3.2% as we closed out the week. The three September economic reports we’ll be focusing on next week are Retail Sales, Industrial Production, and Housing Starts.

The Retail Sales report will not only bring insight into Costco’s (COST) blowout September revenue report, it will bring the final piece of the quarter as well. With that in hand, we’ll have yardsticks by which to measure upcoming earnings reports from Amazon (AMZN) and others tied to consumer spending.

When we review the September Industrial Production report, we’ll continue to focus on what it says about the manufacturing economy. Our intention is to compare that to September Manufacturing PMI findings from ISM and S&P Global. The last few months of the manufacturing production data have offered a slightly more positive view of that part of the economy

In mid-September, we learned August New Home Purchase Mortgages rose 4.4% compared to July, and both Lennar (LEN) and KB Home (KBH) guided their H2 2024 deliveries up double-digits compared to H1 2024. That sets the stage for what could be a positive single-family housing starts print in the September Housing Starts report. If that is what we see, it would be a positive catalyst for shares of Builders FirstSource (BLDR), United Rentals (URI), Vulcan Materials (VMC), and Waste Management (WM).

We also have several Fed speakers making the rounds, spread out throughout the week. We’ll be listening for their post-September inflation report comments to determine if their thinking lines up with ours after those reports.

Here's a closer look at the economic data coming at us next week:

U.S.

Wednesday, October 16

· MBA Mortgage Applications Index – Weekly (7:00 AM ET)

· Import/Export Prices – September (8:30 AM ET)

· EIA Crude Oil Inventories – Weekly (10:30 AM ET)

Thursday, October 17

· Initial & Continuing Jobless Claims – Weekly (8:30 AM ET)

· Retail Sales – September (8:30 AM ET)

· Industrial Production & Capacity Utilization – September (8:30 AM ET)

· Business Inventories – August (10:00 AM ET)

· NAHB Housing Market Index – October (10:00 AM ET)

· EIA Natural Gas Inventories – Weekly (10:30 AM ET)

Friday, October 18

· Housing Starts & Building Permits – September (8:30 AM ET)

International

Monday, October 14

· China: Inflation Rate, Producer Price Index – September

· China: GDP Growth Rate (Advanced) – 3Q 2024

Tuesday, October 15

· Japan: Industrial Production & Capacity Utilization – August

· Germany: Wholesale Prices – September

· Eurozone: ECB Bank Lending Survey

· Eurozone: Industrial Production – August

· Eurozone: ZEW Economic Sentiment Index - October

Wednesday, October 16

· UK: Inflation Rate - September

Thursday, October 17

· Eurozone: Inflation Rate – September

· Eurozone: European Central Bank Interest Rate Decision

Friday, October 18

· China: 3Q 2024 GDP

· China: Industrial Production, Retail Sales – September

· UK: Retail Sales - September

While we have a bit of a breather on Monday due in part to Indigenous Peoples’ Day, equity market will be open but no market-moving companies are expected to report. We will remain on watch, however, for any companies that seek to use the day to slip by any earnings pre-announcements.

Over the ensuing days, we have three more portfolio companies reporting – Bank of America (BAC), Morgan Stanley, and Elevance Health (ELV) – spread across Tuesday, Wednesday, and Thursday. Quarterly results this week from JPMorgan Chase (JPM) and Wells Fargo (WFC) drove some good performance for BAC and MS shares late this week, setting up their reports next week rather nicely. With Elevance, the focus will be on cost containment and footprint expansion as we rip through its results, but we also recognize the overhang that is the 2024 presidential election.

We also have earnings from Bullpen resident Netflix (NFLX), which we’ll use to update our view on those shares, but we’ll also be interested in what the company says about its advertising-supported offerings. With Trade Desk (TTD) shares moving closer to our $120 price target, Netflix’s comments could give us a reason to revisit that target.

Because it touches on several of our holdings, we’ll be spending ample time parsing results and guidance from Taiwan Semiconductor (TSM). With TSM’s September revenue in hand, we’ll be focusing on its end market mix and comments not only about the current quarter but also its capacity utilization levels. Our expectation is that tightened further during the quarter, and that means we will be listening closely for any comments about capital spending plans in the coming quarters.

Outside of the portfolio and those particular stocks, we’ll be monitoring results from Goldman Sachs (GS), Ericsson (ERIC), United Health (UNH), ASML (ASML), Discover (DFS), and American Express (AXP).

Here's a closer look at the earnings reports coming at us next week:

Tuesday, October 15

· Open: Albertsons (ACI), Bank of America (BAC), Charles Schwab (SCHW), Citigroup (C), Ericsson (ERIC), Goldman Sachs (GS), Johnson & Johnson (JNJ), United Health (UNH).

· Close: Interactive Brokers (IBKR), JB Hunt (JBHT), United Airlines (UAL)

Wednesday, October 16

· Open: ASML (ASML), Morgan Stanley (MS), Synchrony Financial (SYF)

· Close: Alcoa (AA), CSX (CSX), Discover Financial Services (DFS), PPG Industries (PPG), Steel Dynamics (STLD)

Thursday, October 17

· Open: Elevance Health (ELV), Nokia (NOK), Taiwan Semiconductor (TSM)

· Close: Netflix (NFLX)

Friday, October 18

· Open: Ally Financial (ALLY), American Express (AXP), Procter & Gamble (PG).

Portfolio September Quarter Earnings Schedule:

Below is a mixture of announced and tentative reporting dates for the portfolio’s holdings. As we move deeper into the September-quarter earnings season, we’ll be updating this list as needed:

October 15 – Bank of America BAC

October 16 – Elevance Health ELV, Morgan Stanley MS

October 22 – Alphabet GOOGL, Lockheed Martin LMT, Microsoft MSFT

October 23 – Meta Platforms META, United Rentals URI

October 24 – Apple AAPL, Amazon AMZN, Labcorp LH, Mastercard MA

October 28 – Waste Management WM

October 31 – Builders FirstSource BLDR, Universal Display OLED

November 6 – Dutch Bros BROS, Qualcomm QCOM

November 7 – Axon AXON, Trade Desk TTD, Vulcan Materials VMC

Portfolio Investor Resource Guide

· Economic Data: Here's a List of Links to the Key Economic Data We Closely Watch

· Investing Terminology: 16 Key Terms Club Members Should Know

· 10-Ks: Want to Know About a Stock? Read the Company's Reports

· 10-Qs: Unlock the Numbers and Key Information Behind Your Stock With the 10-Q

· Income Statement: Our Cheat Sheet to Understanding This Financial Document

· Balance Sheet, Cash Flow Statements, and Dividends: How to Know If a Company Is Off-Kilter? Read Its Balance Sheet

· Valuation Metrics: Everyone Wants a Value. Here's How Investors Can Find

The Portfolio Ratings System

1 - Buy Now (BN): Stocks that look compelling to buy right now.

2 - Stockpile (SP): Positions we would add to on pullbacks or a successful test of technical support levels.

3 - Holding Pattern (HP): Stocks we are holding as we wait for a fresh catalyst to make our next move.

4 - Sell (S): Positions we intend to exit.