What We're Focused on as Headline September PPI Falls

The September Core PPI is another reason why the Fed could deliver a slower pace of rate cuts

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The market is moving higher this morning as are the majority of our holdings following nice quarterly results out of a few of the big banks and a favorable headline September print for the Producer Price Index (PPI).

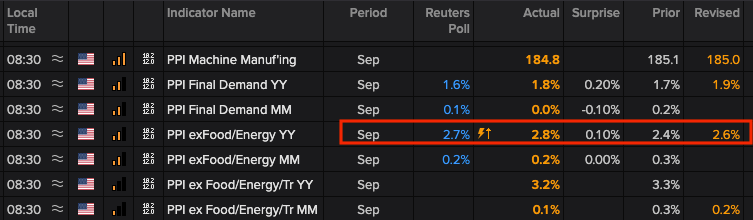

While many are focused on that latest move down for headline PPI, what we saw with the core PPI figure in September has us less enthusiastic.

As you can see in the table above, not only was the August core PPI figure revised higher to 2.6% from 2.4%, but the September reading also jumped up even further to 2.8%, hotter than the 2.7% market consensus. Ahead of this report, we explained why the September ISM Service PMI price subcomponent led us to suspect we could see a higher-than-expected print.

Context, as we like to say, is key and that has us looking back at prior core PPI data. In doing so, we see the data trend has been volatile this year, but we haven’t seen the sustained moves lower like we did in 2023. We acknowledge that the closer we get to the Fed’s 2% target, the more difficult incremental progress can be. But as we can see in the chart above the trend, much like we saw with Thursday's CPI data, doesn’t scream that the Fed must cut rates.

Taking in the data published over the last two weeks, we’d say the Fed does not need to rush further rate cuts. Based on what is seen in the data ahead the Fed can be flexible. Between now and the Fed’s next policy decision on November 7, we’ll get the September PCE Price Index data, ISM’s October PMI figures, and several looks at jobs as well as wages in October. What we won’t get before the meeting is the October CPI and PPI reports, which could be influenced by the rebound in oil prices that has unfolded amid renewed Middle East tensions.

As we think about the potential pace of rate cuts to come, should the Fed opt to lean more dovish and loosen monetary policy further, our interest rate-sensitive positions will benefit. If, however, the Fed opts to take a more measured approach than the market expects, we have our shopping list of stocks and a plan to follow.