Weekly Roundup: After a November to Remember, What's in Store for December?

Historically December is a strong month for the stock market. Here's our we're prepping the portfolio for year-end and 2025.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The stock market powered ahead during this shortened, holiday and shopping-filled week, adding to the gains posted by broader market averages earlier this month. That combination more than offset the October decline seen for all four major market averages, leaving them up mid-single digits with one month to go in the current quarter.

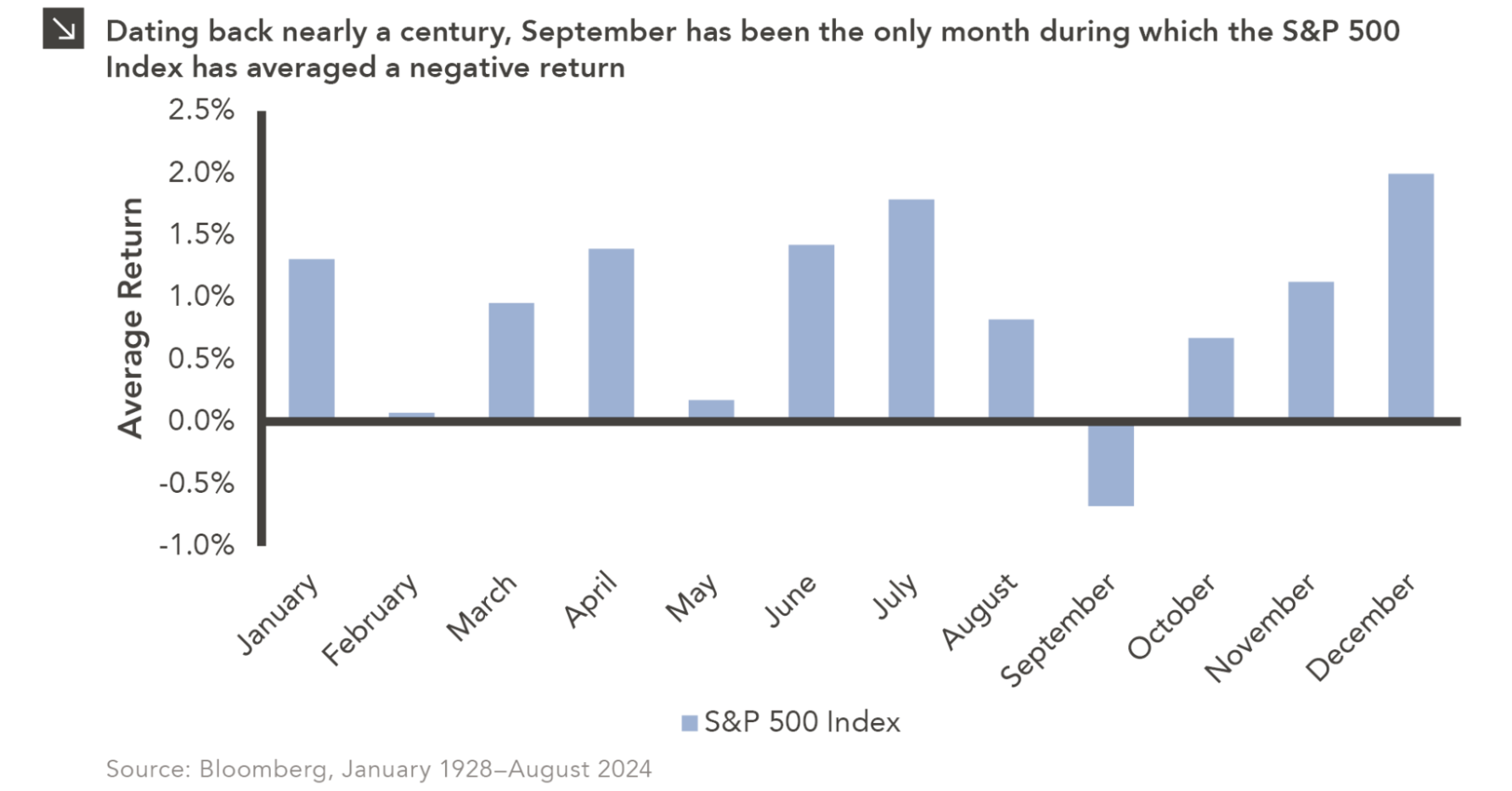

The predisposition of the market is for December to be one of the strongest months of the year. As we look at the chart below, however, we recognize the S&P 500’s move in November 2024 was far greater than the average. At the same time, the Fear and Greed Index’s "Greed" reading moved up over the last week and Citibank’s Panic Euphoria model is flashing "Euphoria."

While neither the S&P 500 nor the Nasdaq Composite are flashing overbought status with their latest relative strength levels, it’s fair to say expectations are running high. Adding to that is the recent decline in the dollar, which has been on a tear over the last several weeks. The move this week in the dollar is helpful, but so far still not enough to quash currency headwinds. We’ll want to follow this and the 10-year Treasury yield as we digest next week’s November economic data and the implications for a Fed rate cut on December 18.

Setting us up for that data, the Fed’s November policy meeting minutes showed the central bank thinking the path to its 2% inflation target may take longer than expected. The minutes revealed conversations about a more gradual approach to recalibrating monetary policy may be called for. In reviewing those minutes with you and breaking down the October PCE price index data that showed little question about inflation being sticky, we also explained why next week’s data has the potential to make or break the likelihood of a December rate cut.

With expectations running high, if next week’s data increases the likelihood the Fed delivers a pause on December 18, it could foster a market pullback following the strong November move. Other developments that could influence the market as we begin December include policy-related announcements from President-elect Trump, geopolitical tensions, and whether Black Friday-Cyber Monday spending forecasts are met.

Our plan is to return from the shopping weekend reinvigorated for the final 21 trading days of 2024, finish the year strong, and position the portfolio for what’s to come in 2025.

Have a wonderful weekend, and we’ll see you back here on Monday.

Catching Up on the Portfolio This Week

While the market rose over the last few days, gains in Amazon AMZN, Builders FirstSource BLDR, Dutch Bros BROS, Alphabet GOOGL, Mastercard MA, and other portfolio holdings were offset by declines in Nvidia NVDA and Lockheed Martin LMT. On Monday, we took advantage of the sharp selloff in Lockheed Martin shares following a tweet by Elon Musk. We didn’t quite bottom tick that purchase, but we did score a nice pick-up at $518.53 before LMT shares rebounded. Just ahead of the Thanksgiving holiday, Lockheed was awarded a $579 million contract modification with the Japan Ministry of Defense that runs through August 2026.

During November, the portfolio benefited from some pronounced moves in its holdings with notable standouts being Dutch Bros and Elastic N.V. ESTC followed by double-digit moves in Bank of America BAC, Eaton ETN, Marvell MRVL, Morgan Stanley MS, and ServiceNow NOW. Those gains as well as those in other holdings that bested the S&P 500 in November allowed the portfolio to widen its lead over the S&P 500. As we shared in last week’s Monthly Roundup, while we’re pleased with that, we recognize the road ahead is a long one and we will remain vigilant.

Meanwhile, we have our eyes on a few other positions, including Meta META and Microsoft MSFT, that remain on our shopping list, but should the year-end market strength play out as expected, we’ll remain disciplined buyers as we approach the start of 2025. Over the next few weeks we’ll be refreshing our thoughts on the portfolio’s holdings as they relate to the coming year and most likely revisiting the Bullpen’s current list of potential portfolio candidates. Our goal remains to position the portfolio for what’s ahead, focusing on companies poised to benefit from multi-year tailwinds and deliver superior earnings growth.

During the week, Wall Street made some noise regarding some of our holdings:

Redburn Atlantic boosted its Amazon AMZN price target to $235 from $225 and reiterated its Buy rating.

Bernstein trimmed its price target for Applied Materials AMAT to $210 from $200. We made the same move in mid-November following Applied’s quarterly results and used some of the post-earnings selloff to pick up more shares for the portfolio near current price levels.

Last week we boosted our price target on Elastic ESTC to $135 and this week Citi upped its to $150 from $136, Barclays reset its at $138 from $105, and Wedbush upgraded ESTC shares to Outperform from Neutral as software “gets in on the AI party.”

Susquehanna lifted its Marvell MRVL price target to $110 from $95, noting upside demand for custom AI chips driven by robust demand. Ahead of that move both Wells Fargo and Oppenheimer upped their MRVL target to $110 from $90 as it sees tailwinds accelerating into 2025. Our MRVL price sits at $105, but we’ll be revisiting that after the company reports next week.

Raymond James added Meta META to its Analyst Current Favorites List, reiterating its Strong Buy and $675 target as it did so.

Citi boosted its price target on Morgan Stanley MS shares to $135 from $105 amid an improving capital markets outlook. During the week, we shared what we’re watching when it comes to MS and BAC shares and IPO activity.

JPMorgan raised its target on Vulcan Materials VMC to $290 from $245.

This Week's Portfolio Videos

We cover a lot of ground during the week in our Daily Rundowns. If you happened to miss one or more of them, here are some helpful links:

Monday, November 25: Here's Our Plan in Case This Holding Becomes Oversold

Tuesday, November 26: Our Take on the Fed Minutes, New Homes Sales and Consumer Confidence

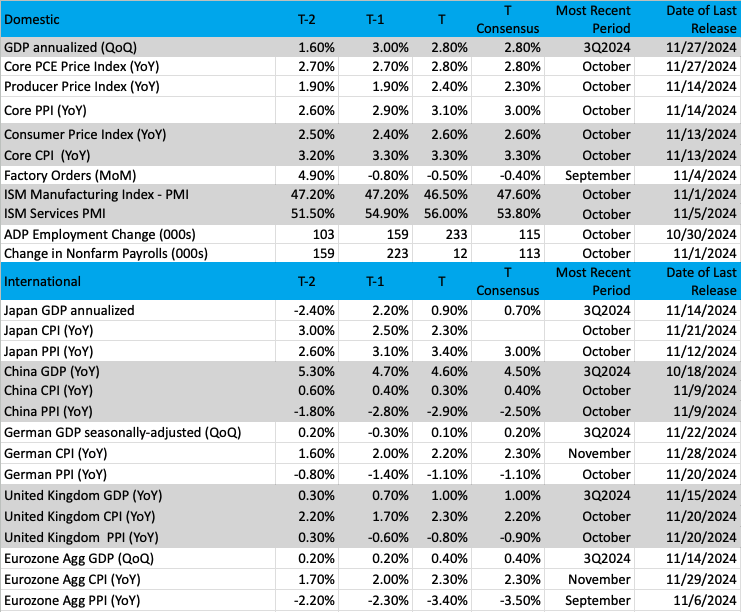

Key Global Economic Readings

(Note: T is the most recent period, T-1 is the prior period's reading and T-2 is two periods back, the intent being to illustrate any trends)

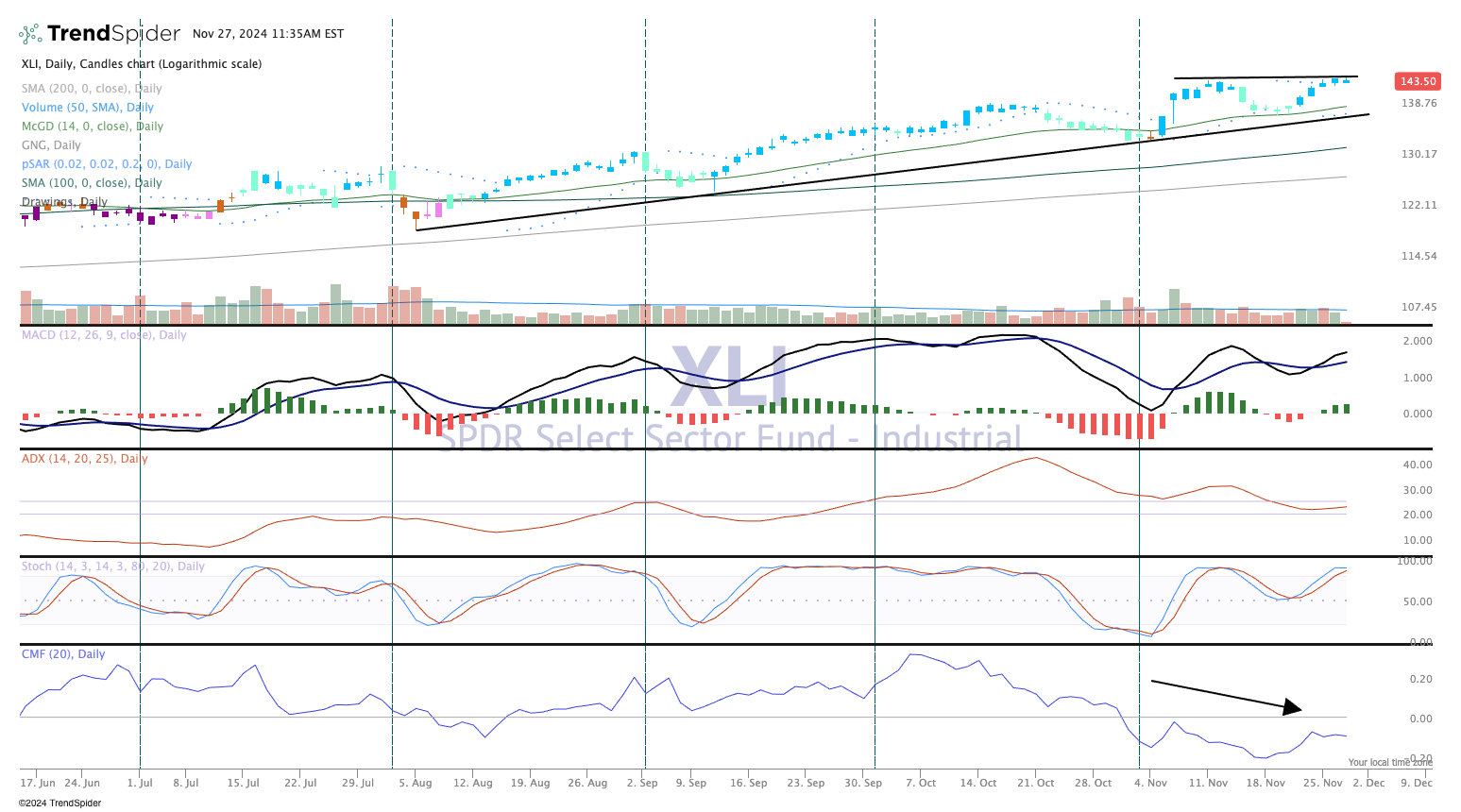

Chart of the Week: Industrial Select Sector SPDR Fund (XLI)

It's simply been a spectacular year for the industrial — not just the Dow 30 but also the Industrial Select Sector SPDR Fund XLI. This ETF really burst onto the scene back in early August following that scary drop of nearly 5% in the broader market indexes. That move down was the bottom for the XLI, and since then the ETF has been roaring higher.

We have several industrial-related names in the portfolio, so it is important to always track this ETF. A series of higher highs, and higher lows in this chart is a textbook uptrend, and even the pullbacks over the last five months were excellent buying chances on the XLI.

Some caution, though is warranted. Currently the Chaikin money flow (CMF), seen at the bottom of the chart, reflects bearish flows. That simply means more outflows in the ETF, which creates a divergent condition. This is not a signal but rather a recognition that price action diverts from the indicators.

Does it matter, or should it matter? Yes, it does and should in the context of trying to determine if an uptrend has stretched too long or moved too far. In this case that might be true. We do have the MACD (moving average convergence/divergence) still on a buy signal crossover, and the stochastics are overbought but may be rolling over (pane 4).

Lastly, the top pane shows a sufficient ceiling around the $144 area. Perhaps a double top (bearish) is being created here. If the trendline drawn in from August fails to hold, there clould be a much more significant down move to come.

Other charts we shared with you this week were:

Monday, November 25: Russell 2000 - The Russell Is on a Run

Monday, November 25: Meta Platforms (META) - Is This Yet Another Opportunity to Buy This Holding?

Tuesday, November 26: Amazon (AMZN) - It's the Most Amazon Time of the Year

Wednesday, December 27: First Trust Nasdaq Cybersecurity ETF (CIBR) - Cybersecurity Remains Top of Mind for Most Companies

The Week Ahead

When we return from the holiday shopping weekend, there will be just 21 trading days left until we shut the book on 2024. In last week’s Roundup, we discussed that while some will be in coast mode as we approach year-end, we will remain focused on positioning the portfolio for the months and quarters ahead.

Part of that means dissecting the wave of November economic data coming at us next week. What we find in the various PMI, employment, and other data will tell us much about the health of the underlying economy and give us a better sense of timing for the next Fed rate cut. Complementing those figures will be the latest iteration of the Fed’s anecdotal collection of economic conditions, better known as its Beige Book. Ahead of that data, the CME FedWatch Tool shows a better than 60% chance the Fed will deliver another 25-basis point rate cut on December 18 with the next one not likely until its May policy meeting.

As we’ve seen before, though, as fresh employment and inflation data becomes available, we could see those market expectations shift. This means we’ll keep a close on the numbers and what it means for rate cuts, the economy and the portfolio.

We’ll also be looking forward to the final consumer spending tally from the Black Friday-Cyber Monday shopping event. The figures should confirm our view that consumers are leaning into digital shopping, a positive for our shares of Amazon AMZN and Costco COST. To the extent the overall shopping weekend disappoints, it would confirm our concern about retailer margin pressure as they ramp sales and other promotional activities between now and Christmas.

Here's a closer look at the economic data coming at us next week:

U.S.

Monday, December 2

· Cyber Monday

· S&P Global Final Manufacturing PMI – November (9:45 AM ET)

· ISM Manufacturing Index – November (10:00 AM ET)

· Construction Spending – October (10:00 AM ET)

Tuesday, December 3

· JOLTS Job Openings & Quits – October (10:00 AM ET)

Wednesday, December 4

· MBA Mortgage Applications Index – Weekly (7:00 AM ET)

· ADP Employment Change Report – November (8:15 AM ET)

· S&P Global Final Service PMI – November (9:45 AM ET)

· ISM Non-Manufacturing PMI – November (10:00 AM ET)

· EIA Crude Oil Inventories – Weekly (10:30 AM ET)· Fed Beige Book (2 PM ET)

Thursday, December 5

· Initial & Continuing Jobless Claims – Weekly (8:30 AM ET)

· Factory Orders – October (10:00 AM ET)

· EIA Natural Gas Inventories – Weekly (10:30 AM ET)

Friday, December 6

· Employment Report – November (8:30 AM ET)

· University of Michigan Consumer Sentiment Index (Preliminary) – December (10:00 AM ET)

· Consumer Credit – October (3 PM ET)

International

Monday, December 2

· China: NBS Manufacturing & Non-Manufacturing PMI – November

· China: Caixin Manufacturing PMI - November

· Japan: Jibun Bank Manufacturing PMI – November

· Eurozone: HBOB Manufacturing PMI – November

· UK: S&P Global Manufacturing PMI - November

Wednesday, December 4

· Japan: Jibun Bank Services PMI – November

· China: Caixin Services PMI – November

· Eurozone: HCOB Services PMI – November

· Eurozone: Producer Price Index - October· UK: S&P Global Services PMI - November

Thursday, December 5

· Eurozone: Retail Sales - October

Friday, December 6

· Germany: Industrial Production – October

· Eurozone: GDP (3rd estimate) – 3Q 2024

As strange as it may seem as we enter the final weeks of the year, companies are still reporting their quarterly results. Among those reporting next week will be portfolio holding Marvell Technology MRVL as well as another slew of retailers. We’ll continue to parse their guidance, but our suspicion is it will confirm our thinking the holiday season will have its share of retail winners and losers.

We’ll also be eyeing reports from Zscaler (ZS), and Okta (OKTA) given our position in the First Trust Nasdaq Cybersecurity ETF CIBR. In addtion, we'll be interested in what Salesforce (CRM) has to say about AI adoption in the enterprise and what that could mean for several holdings in the portfolio.

Here's a closer look at the earnings reports coming at us next week:

Monday, December 2

· Close: Zscaler (ZS)

Tuesday, December 3

· Close: Box (BOX), Marvell Technology (MRVL), Okta (OKTA), Salesforce (CRM)

Wednesday, December 4

· Open: Campbell Soup (CPB), Dollar Tree (DLTR), Foot Locker (FL), Hormel Foods (HRL)

· Close: American Eagle (AEO), Five Below (FIVE), PVH (PVH), SentinelOne (S)

Thursday, December 5

· Open: Brown-Forman (BF.B), Kroger (KR)

· Close: Cooper (COO), Hewlett Packard Enterprise (HPE), lululemon (LULU), Petco Health & Wellness (WOOF), Ulta Beauty (ULTA), Victoria’s Secret (VSCO)

Portfolio Investor Resource Guide

· Economic Data: Here's a List of Links to the Key Economic Data We Closely Watch

· Investing Terminology: 16 Key Terms Club Members Should Know

· 10-Ks: Want to Know About a Stock? Read the Company's Reports

· 10-Qs: Unlock the Numbers and Key Information Behind Your Stock With the 10-Q

· Income Statement: Our Cheat Sheet to Understanding This Financial Document

· Balance Sheet, Cash Flow Statements, and Dividends: How to Know If a Company Is Off-Kilter? Read Its Balance Sheet

· Valuation Metrics: Everyone Wants a Value. Here's How Investors Can Find

· Thematic Investing 101 Webinar

The Portfolio Ratings System

1 - Buy Now (BN): Stocks that look compelling to buy right now.

2 - Stockpile (SP): Positions we would add to on pullbacks or a successful test of technical support levels.

3 - Holding Pattern (HP): Stocks we are holding as we wait for a fresh catalyst to make our next move.

4 - Sell (S): Positions we intend to exit.