We Are Trimming and Downgrading Our McDonald's Position

There are a host of reasons why we are making these moves.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

* We are trimming our McDonald’s position, which has been a drag on the portfolio.

* We will also downgrade MCD to a Three rating from Two on concerns about March-quarter results and guidance headwinds.

* We will look to opportunistically reduce exposure to MCD in the near term.

| Symbol | Transaction Type | #Shares Traded | Recent Price ($) | Shares Owned After Trade | % Portfolio |

|---|---|---|---|---|---|

MCD | Sell | 230 | 267.20 | 225 | 1.50 |

After you receive this Alert, we will sell 230 shares of McDonald’s MCD at or near $267.20. Following the trade, MCD shares will account for about 1.5% of the portfolio.

An easy mistake for an investor to make is falling in love with their holdings, which can blind them to changes in the data that warrant a re-think for owning the shares of a company. We aim to avoid that mistake by parsing and revisiting the data as they are updated, letting it talk to us rather than looking for what we want to see. It’s that critical eye that helps us side-step potentially crushing problems.

One of those data points we track as it relates to the portfolio’s position in McDonald’s is restaurant spending. MCD shares are down nearly 10% year to date, lagging the market, and that is weighing on the portfolio given the 6% decline for our position. That is leading us to dig a bit deeper beyond the favorable findings for restaurant spending in the March Retail Sales report, which showed those sales climbed 6.5% for the month, matching February’s gain, and compared to 5.4% for the March quarter. As we lamented at the time, that line item doesn’t give much insight into the spending between fine dining, casual dining, and fast food.

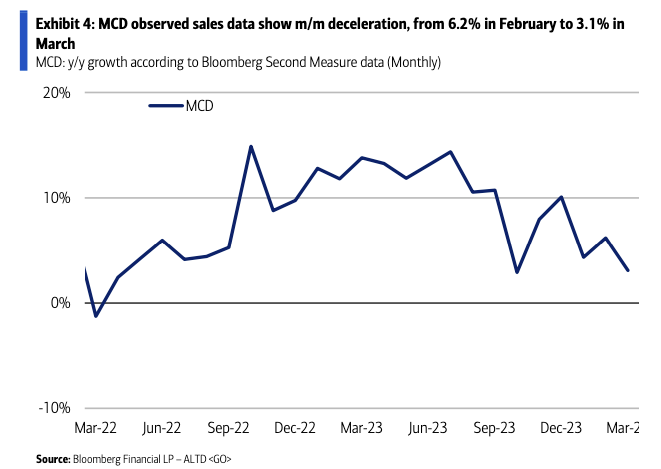

Other restaurant-facing data from Bloomberg gives us a second look at credit-card and debit-card spending. Those figures showed restaurant sales growth decelerated to 3.8% in March from 4.2% in February. While that isn’t a deal breaker per se, what the data showed for McDonald’s compared to other restaurant companies is more concerning. McDonald’s sales growth decelerated in March while sales growth at Domino’s DPZ, Papa John’s PZZA, Wingstop WING, Jack in the Box JACK, and Yum! Brands YUM accelerated. Wendy’s WEN was unchanged month over month.

Tracking that data suggests McDonald’s U.S. sales were in line with Wall Street total revenue expectations for the March quarter, up 4.5% year over year. The key here is that the U.S. business accounts for about 40% of overall revenue. However, in mid-March the company said its international sales will fall sequentially in the current quarter, pressured by the conflict in the Middle East and demand weakness in China. With the Middle East and other geopolitical tension increasing this month, it stands to reason those factors could be a headwind in the current quarter as well.

McDonald’s French fry supplier Lamb Weston LW has dialed back its fiscal 2024 revenue guidance to $6.54 billion-$6.60 billion from $6.8 billion-$7.0 billion, which implies modest top-line improvement in the current quarter. It’s not lost on us that Lamb’s largest customer is McDonald’s, which accounted for 10%-13% of Lamb’s revenue over the last few years.

We are also reading about the prospects of record beef prices this year because of the lowest cattle inventory since 1951, according to the American Farm Bureau Federation. The last time beef prices spiked in 2014, McDonald’s operating margin hit the lowest level since the start of the Great Recession. And that time around, we didn’t have the impact of California’s $20 minimum hourly wage to contend with, an issue the fast-food industry will have to contend with starting this quarter.

Putting these pieces together suggests we could see McDonald’s come up short either with its March-quarter results or it guidance. MCD is flirting with becoming oversold, but to us, there is the risk of the shares moving lower or best case becoming dead money in the near to medium term.

There is also the issue of modest EPS growth expectations for 2024 and 2025, up 4.0% and 1.0%, respectively. That pales in comparison to the double-digit growth expected for the market. Should McDonald's expectations soften, it would be another reason why P/E multiple expansion isn’t likely to emerge and if it does, probably won’t be robust.

We are likely to see we see far better growth prospects for companies currently in the Bullpen such as The Trade Desk TTD and Welltower WELL, which are on our shopping list should they hit the right price level.

Based on all of the above, taking some of our McDonald's chips off the table and downgrading it to a Three rating from Two. We will look to opportunistically work the portfolio out of MCD in the near term.

(Please note that we are looking to execute these trades at or near the share price mentioned above. Once the trade is completed, subscribers can see the trade's executed price here. Be sure to toggle the chart to sort by Purchase Date.)

At the time of publication, TheStreet Pro Portfolio was long MCD.