Here's the Big Picture on Gold, Silver, Oil and Meats

Let's recap what's going in the commodities world and where we may be headed.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

In a news-driven world, blocking out the noise and focusing on the big picture can be challenging. We will attempt to do that in a few commodity markets garnering a lot of attention as global politics heat up.

Gold

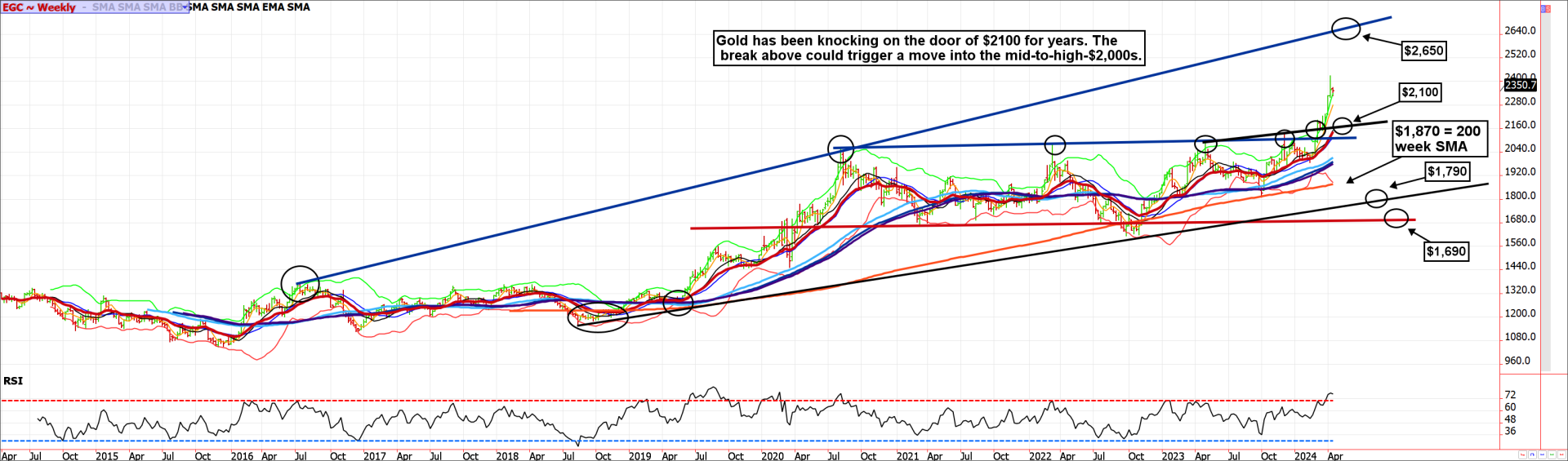

A mostly forgotten commodity headed into 2024 has made one of the most considerable splashes. Gold is playing catch-up after years of stagnant pricing.

Previously, higher interest rates and a higher dollar have been headwinds preventing the yellow metal from pricing inflation and geopolitical risk into valuation, but investors have finally looked past those hurdles. In fact, neither of those factors has resolved themselves, but the precious metal has rallied wildly in spite.

Gold started its move in mid-February; we suspect investors with cash to allocate likely looked at gold and silver as being attractively priced in a world of overvalued assets (stocks, crypto, real estate).

For the first time in a long time, flight-to-quality assets are beginning to behave as such. What I mean by this is that the more uncertain geopolitics become, or the rockier the stock rally gets, the more gold and Treasuries seem to catch a bid. Of course, in the case of Treasuries, that bid hasn’t been able to hold, but in gold and silver, it has defied gravity. Markets often overreact, but in this case, it feels like the markets are trying to tell us something.

For a larger view of this chart please click here.

The gold breakout above $2,100 has offered investors or traders few pullbacks to enter. Unfortunately, we believe this environment will continue. Despite violently overbought technical oscillators, we doubt the market will run into any real selling until we test the weekly trendline. This trendline is currently coming in at nearly $2,650, but because it is an inclining barrier, it will move higher over time.

Our fundamental backing for the chart prediction are expectations for the U.S. dollar rally to run into trouble near 107.00/107.50 and the Treasury market finding buyers due to favorable interest-rate differentials and the potential for a stalled equity rally, which would make bonds seem attractive.

Silver

In the commodity industry, we often refer to natural gas as the widow maker due to its ability to display erratic price action and unfathomable volatility. However, silver futures might come in at a close second — let’s call it the divorce attorney.

Although silver prices are generally less volatile than natural gas, they are similar markets in that they lull participants into complacency or indifference before taking market traders by surprise. Furthermore, while all markets pose a bit of a conundrum for stop-loss placement, silver can be a miserable venue for futures traders. Stop-loss orders are almost guaranteed to get hit prematurely, leaving responsible traders sidelined and watching the market move in their favor without them.

On the other hand, those traders without stops will eventually experience the wrath of sudden and unrelenting directional volatility. In short, when it comes to stop loss orders in silver, traders are darned if they do or darned if they don’t.

For a larger view of this chart please click here.

The silver market is forging a rare rally as investors seek alternative assets. Unlike gold, silver has both a precious metal and manufacturing component in its pricing. Perhaps that is the best explanation of why silver has difficulty making progress. Nevertheless, the monthly chart tells us that as long as the breakout above $25.70 continues to hold, we should see the low $30.00s ($32.65 to be precise) and maybe even the high $30.00s ($37.60). Some analysts expect the 2011 all-time high of $50.00, but we aren’t seeing that in the cards yet.

Meats

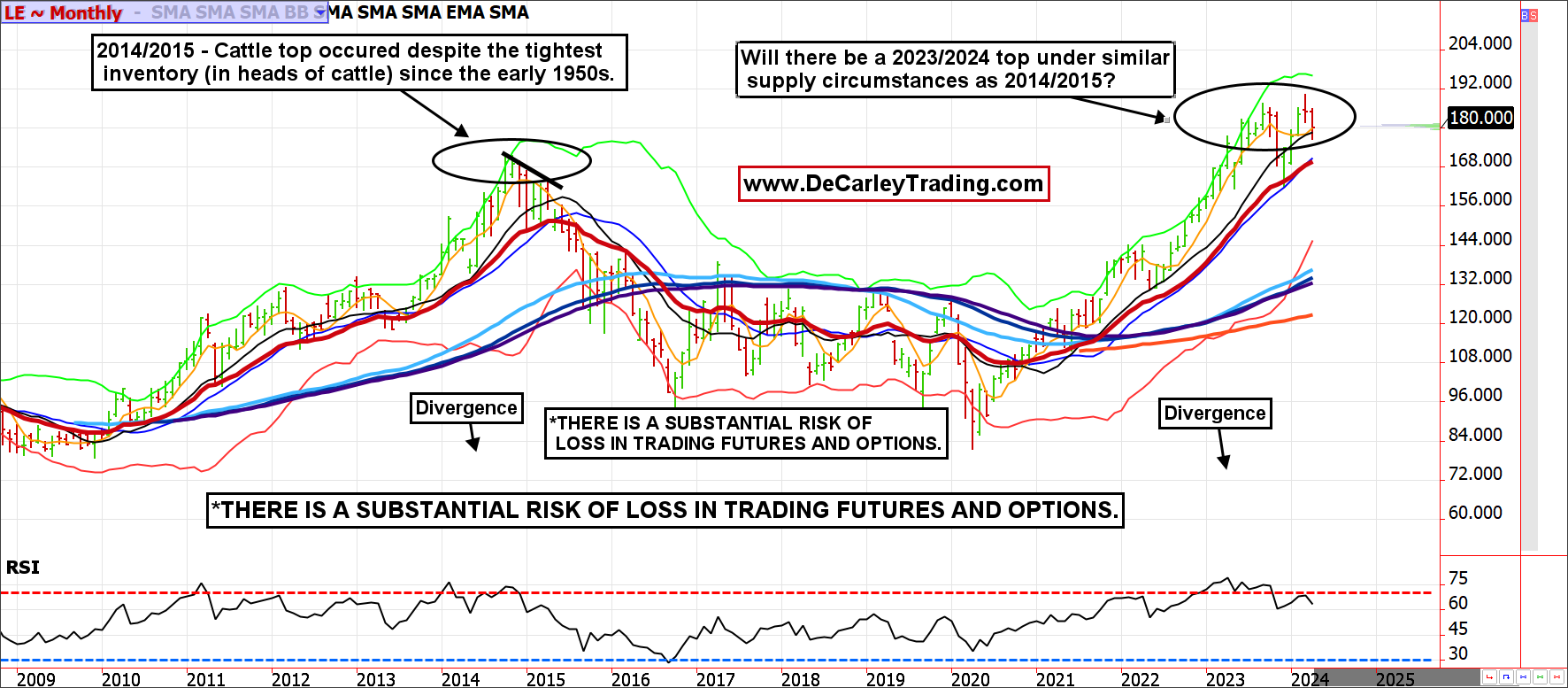

It isn’t a surprise to anyone that beef and pork prices are astronomically high. Thus far, high prices haven’t put much of a dent into demand, but they always do in the long run. While the cattle futures market has diligently priced in a tight supply backdrop, it seems to have forgotten that demand isn’t guaranteed. Consumers can, and eventually will, begin making the switch to lower-cost proteins.

In Las Vegas, steakhouses on The Strip successfully peddle individual steaks from $80.00 to $200.00 (some rare cuts are even higher priced), plus sides; this doesn’t seem sustainable. A reversal of the wealth effect could hasten the public into a lifestyle of more budget-friendly meals.

In other words, high-flying risk assets such as stocks and crypto have led to aggressive consumer habits, but if risk assets take a breather, so will the “appetite” for expensive “tastes” (those puns were intended).

For a larger view of this chart please click here.

We’ve been talking about the similarities between the 2014/2015 cattle market and what we are seeing today. We continue to lean towards a repeat of that scenario. For the sake of cattle producers, we would prefer to be wrong, but the odds suggest that will be the outcome.

Crude Oil

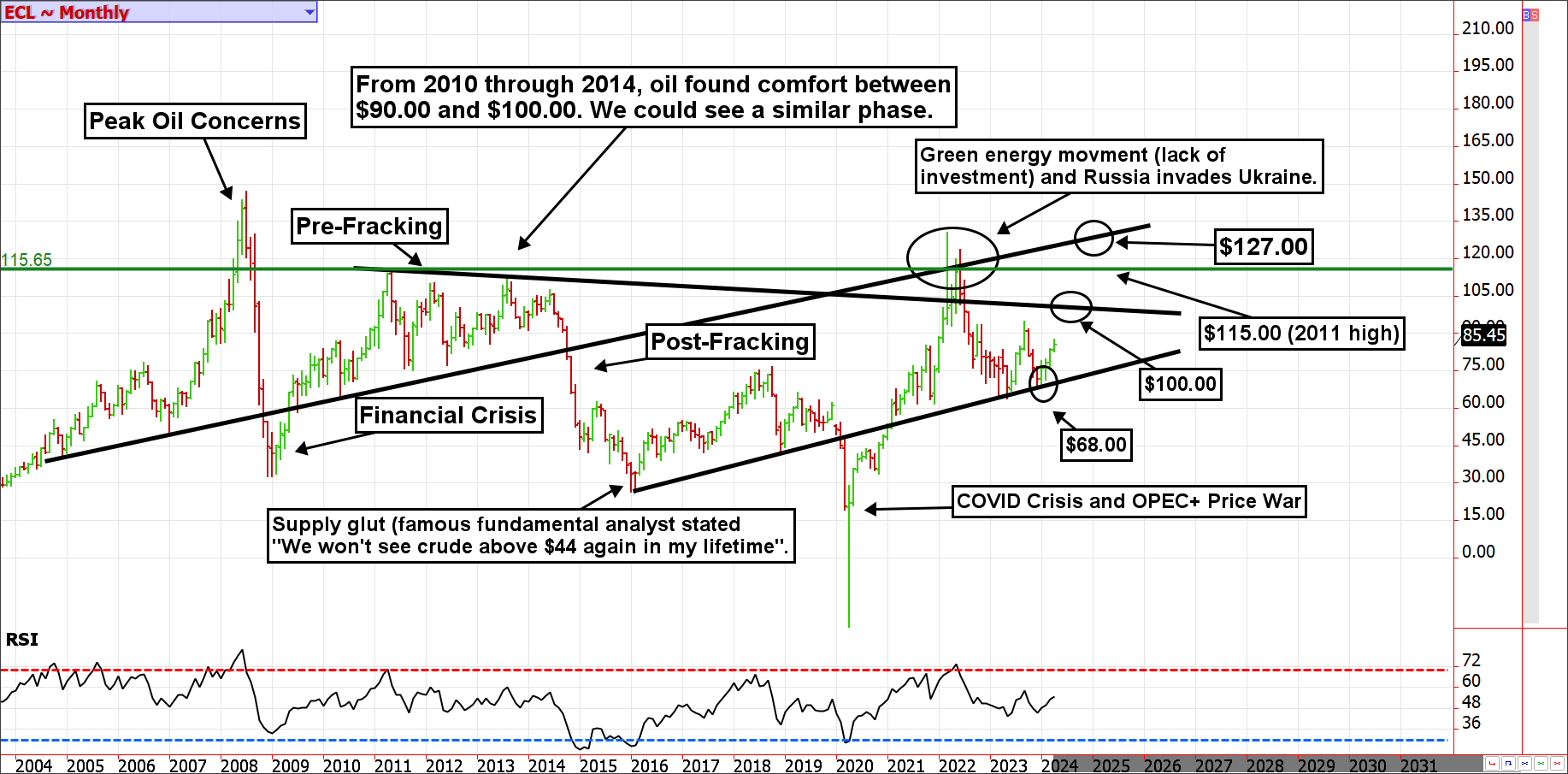

The oil market has rallied from monthly trendline support near $70.00 into the high-$80.00s without help from speculators, the U.S. dollar, or even Chinese demand. Yet, suppose any of these factors shift toward being favorable, rather than antagonistic, to crude oil. In that case, we should continue to see prices press higher toward the next trendline (currently near $100 per barrel).

For a larger view of this chart please click here.

Over the previous 30 trading sessions, oil and the U.S. dollar index futures contracts traded on the ICE exchange have settled in the same directly over 70% of the time. These assets are traditionally negatively correlated, so this is highly unusual.

Some attribute this to the transition some countries are making away from using the dollar as a reserve currency. Remember, oil is priced in U.S. dollars globally, which is what caused the negative correlation in the first place. The dollar index “should” run into resistance near 107.00; if so, we might see a negative correlation return to oil prices. This would be supportive of the oil rally.

According to the Commitments of Traders Report, speculators have only modestly participated in the rally. Large speculators are net long, about 308,000 futures contracts, but we have seen that figure as high as 730,000 in the last decade. If the situation in the Middle East continues to flare up, they might start feeling the FOMO.

Lastly, China has been in a slump, but betting against China in the long run hasn’t necessarily worked out. Someday, it will simply be because the aggressive tactics of Chinese leaders have built a house of cards, but this time probably isn’t “it.”