Doug Kass: I've Been Wrong, But Here's Why I Remain Bearish

Fifteen reasons I continue to view this market cautiously — and you should too.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

As indexes continue to hit new all-time highs, I continue to hold on to a cautious view of the markets.

Here's why:

* Equity performance has been top heavy — with five large-cap technology companies skewing returns. Nvidia NVDA has accounted for 35% of the S&P Index's 2024 performance while four others (Google (GOOGL), Meta META, Microsoft MSFT and Amazon AMZN) are responsible for another 26% of the annual return. Not since the 1960s have five stocks accounted for so much (61%) of the total market return.

* Corporate profit performance is also reliant of mega-cap tech. In 4Q2023 corporate profits rose by +14% but without the seven largest tech stocks there was a -9% drop in profitability. In 1Q2024 corporate profits rose by +6% (but without the contribution of the Mag 7 there was a -2% decline in profits.

* Corporate profit expectations are unrealistic. According to my friend David Rosenberg’s (Rosenberg Research), arithmetically “backing out” from current valuations, the markets expect +17% per year growth in profits over the next five years. This compares to the actual long-run average for earnings growth in a five-year span over the past century of just +6%/year. A profits forecast of +17% is thus a near and highly unlikely two standard deviation event — particularly given the likelihood that the next Administration may be forced to increase both individual and corporate tax rates to fund the U.S. deficit.

From David:

Outside of the distortions around COVID-19 in 2020, this embedded EPS growth forecast was only exceeded by the prior Tech mania in the late 1990s. And we know how that ended — inevitably, that five-year forward earnings growth view reverted to the mean as the sector (typical with manias) became beset with excess capacity. And while it would have been impossible, at the peak in early 2000, to tell anyone that the S&P 500 Tech sector would then endure a two-year -80% bear market, that is exactly what ended up happening. There are clear differences between now and then, but the storyline is that all manias end up confronting the classic Bob Farrell rule #1 on mean reversion.

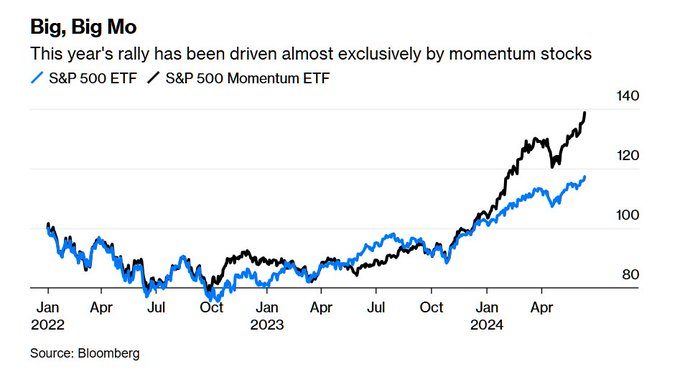

* The market is not broadening out. Breadth remains weak and the equal-weighted S&P Index is only +3% year-to-date (at last Friday's close).

* Traditional valuation metrics are generally in the 90% tile or higher.

* The breathtaking reset in valuations (since October) could mean reverse. From Rosie:

Regarding the consensus earnings forecast for 2024, it is unchanged since mid-October at $244.80. For 2025, the consensus in mid-October was $270.18 and now is sitting at $277.07. That is the grand total of a 2.6% increase in profit views for next year. What has the S&P 500 done since that time? Try +26%! A 10x surge relative to earnings expectations. So, no — this has been and remains a multiple driven market. It definitely is not an earnings-driven market, despite what the talking heads on bubblevision tell you...

* Interest rates are likely to remain higher for longer. For the short-to intermediate- term, higher rates will provide more competition to historically high equity valuations as they will continue to provide equity-like returns with no risk nor volatility.

* Equities have rarely been as overvalued against interest rates as they are today. Consider that the S&P dividend yield stands at only 1.32% compared to a 5.37% yield on the six-month Treasury note — an uncommon wide of 4x! The equity risk premium is at the lowest level in nearly two decades.

* Global economic growth is expected to be weak (relative to consensus). Elevated mortgage rates will dull housing and continue to threaten commercial real estate, the impact of stacked or cumulative inflation (since 2020) will weigh on the overly indebted consumer and the cost of capital for most companies will be rising (in the face of a maturity cliff in 2025).

* Inflation (particularly of a service-kind) will remain sticky. Beneath the Skin of CPI Inflation: A Stunning Outlier Services CPI Drove Down Everything Else | Wolf Street

* Consensus S&P EPS may be too high. Among other issues, the current move away from globalization and towards reshoring will be corporate profit dampening. Moreover, the likelihood of higher corporate tax rates seems to be rising.

* Political risks are underappreciated. Extreme partisanship will likely translate into continued fiscal irresponsibility from both parties (and a general neglect towards addressing burgeoning U.S. deficits and lofty U.S. government debt loads).

* Geopolitical risks are unlikely to abate.

* Investor sentiment remains bullish and fear is absent.

* Market structure and investor positioning are potentially toxic market influences.

I am honest and transparent. I also take ownership for my mistakes.

As long-time readers know, I approach both my roles in writing my Daily Diary on TheStreet Pro and managing Seabreeze as an intimate relationship. It is more than a job to me. I commit 12-13 hours a day towards an objective of providing value-added information/views to our subscribers and of achieving superior investment returns to my Limited Partners.

But during certain periods of time, one's effort is not rewarded. As Warren Buffett once said, "No matter how great the talent or efforts some things just take time. You can't produce a baby in one month by making nine women pregnant."

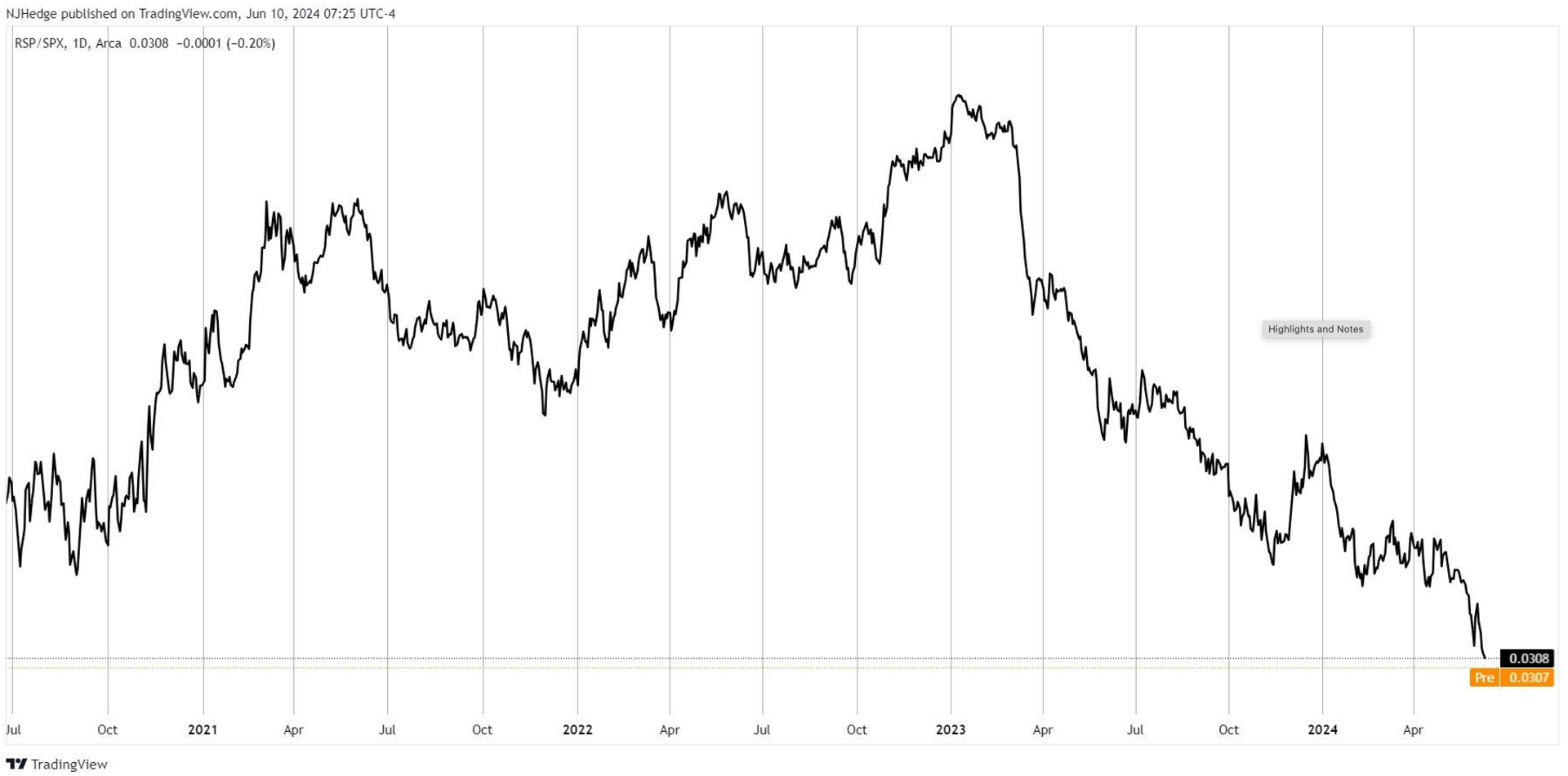

The chart below (RSP v SPX) vividly shows the market’s narrowness. As seen, the equal-weighted S&P (RSP) has dramatically underperformed the market cap-weighted (and heavily tech-influenced) S&P:

The disproportionate role of five stocks continues to be a conspicuous market feature. Consider that Nvidia's market cap has increased by over $1 trillion in the last thirty days. That increase in value exceeds (by $115 billion) Berkshire Hathaway's BRK.A BRK.B total market capitalization of $885 billion. The difference is that it took Warren Buffett six decades to build Berkshire Hathaway to that market cap!

My approach towards value investing will not change, even as many investors chase a small handful of stocks and neglect a much larger body of equities.

Our volume of Benjamin Graham's The Intelligent Investor will not be discarded in the trash:

There are periods in which intelligence and a strong work ethic don't translate into superior investment performance. Just look at Warren Buffett's underperformance during the dot-com boom era — a point in time that many pundits "wrote him off. But, over time the market is more than a voting machine — it’s a weighing machine. As proof positive, just look at Berkshire's superior investment returns in the decade following the dot-com boom bust (in which the Nasdaq dropped by -80%).

That said, I remain very confident that our analysis, logic of argument, hard work and experience will translate into valuable info in my Diary and in good returns. My approach of assessing upside reward vs. downside risk (with an eye towards having a "margin of safety") remains the foundation of all of our investments.

I have long felt that interest rates are the overriding determinant of stock prices. And that investor sentiment and liquidity are a distant second and third.

But there are times (again I look to Buffett) when the markets are a popularity contest and behave like a "voting machine" rather than a "weighing machine." This has been the case since November as animal instincts, fear of missing out (FOMO) and liquidity have overwhelmed the markets.

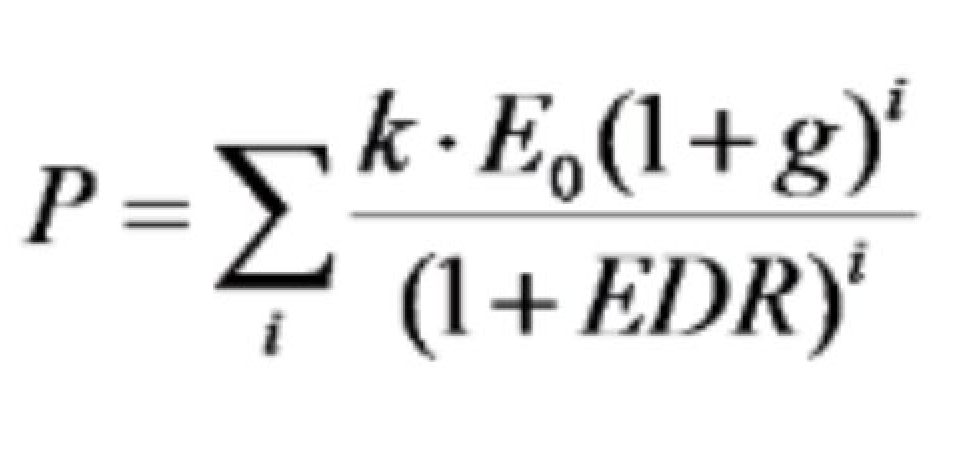

However, over extended periods of time, equity prices are best expressed in the discounted cash flow model below.

Determining valuations based on discounted cash flow models is the foundation of security analysis and our approach to individual stock selection. (Valuations are equal to the expected future cash flows (i.e. dividends) discounted to present value using an Equity Discount Rate ... where P denotes the equity price, E0 is current earnings, k is the payout ratio, g is the growth rate of dividends, and EDR is the Equity Discount Rate).

In the last six months not only have interest rates been ignored in the recent market rally but, arguably and somewhat surprisingly, so have many macroeconomic issues.

But, as the wise man once said, “This too shall change.”

I wanted to end here by highlighting several concerning charts and tables that form some of the basis for our negative market view:

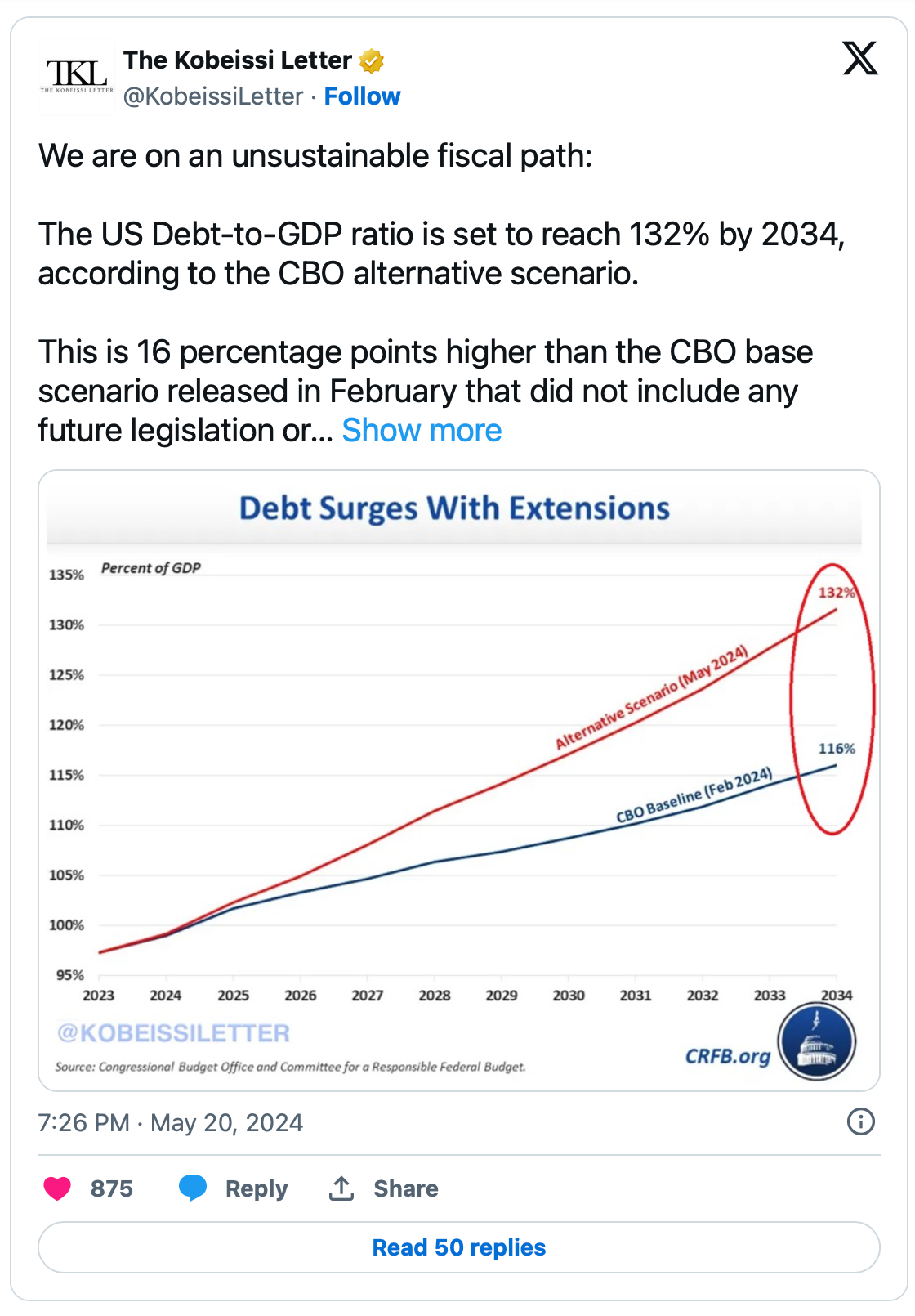

U.S. Deficit and Debt

We are on an unsustainable path of government debt creation and fiscal imprudence. The unprecedented partisanship that exists in Washington, D.C., is unlikely to change as we lean into a presidential election in November. Nor will the political schism between Democrats and Republicans narrow post-election. Fiscal discipline will likely continue to be ignored by both political parties until it is too late:

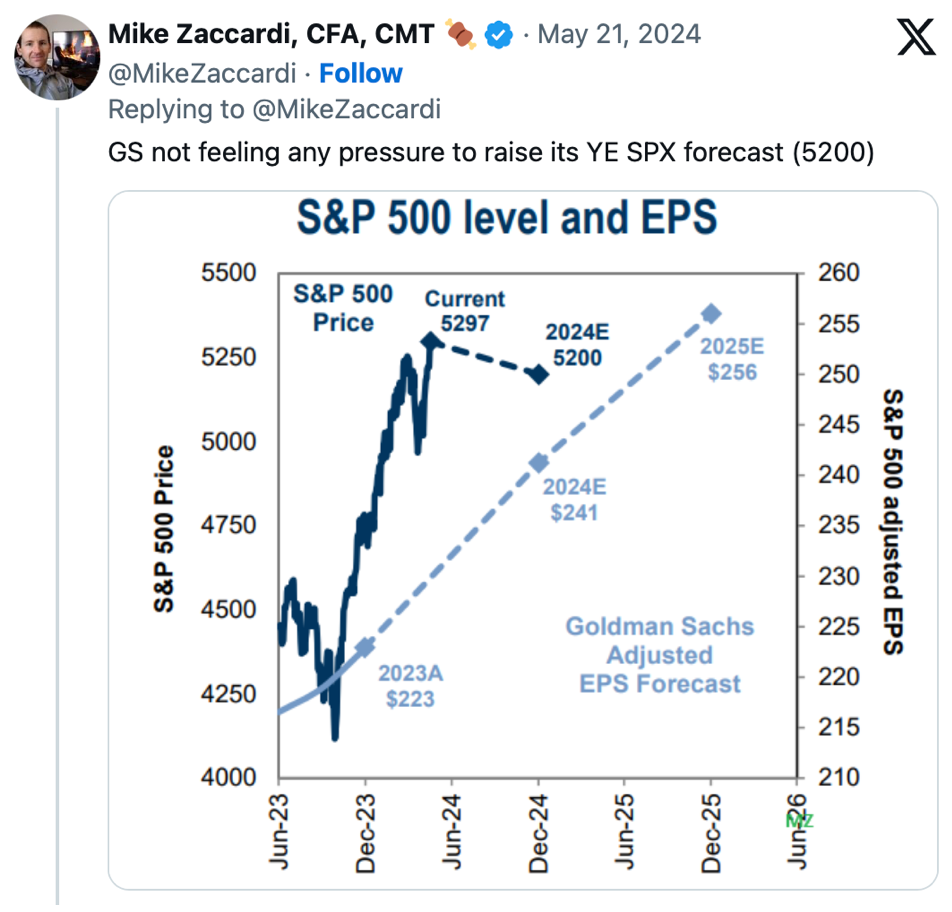

Earnings, Price to Book Value and Equity Risk Premium

By most historical metrics, stocks are valued in excess of the 90% tile. Compared to interest rates equities are more expensive at any time in more than two decades:

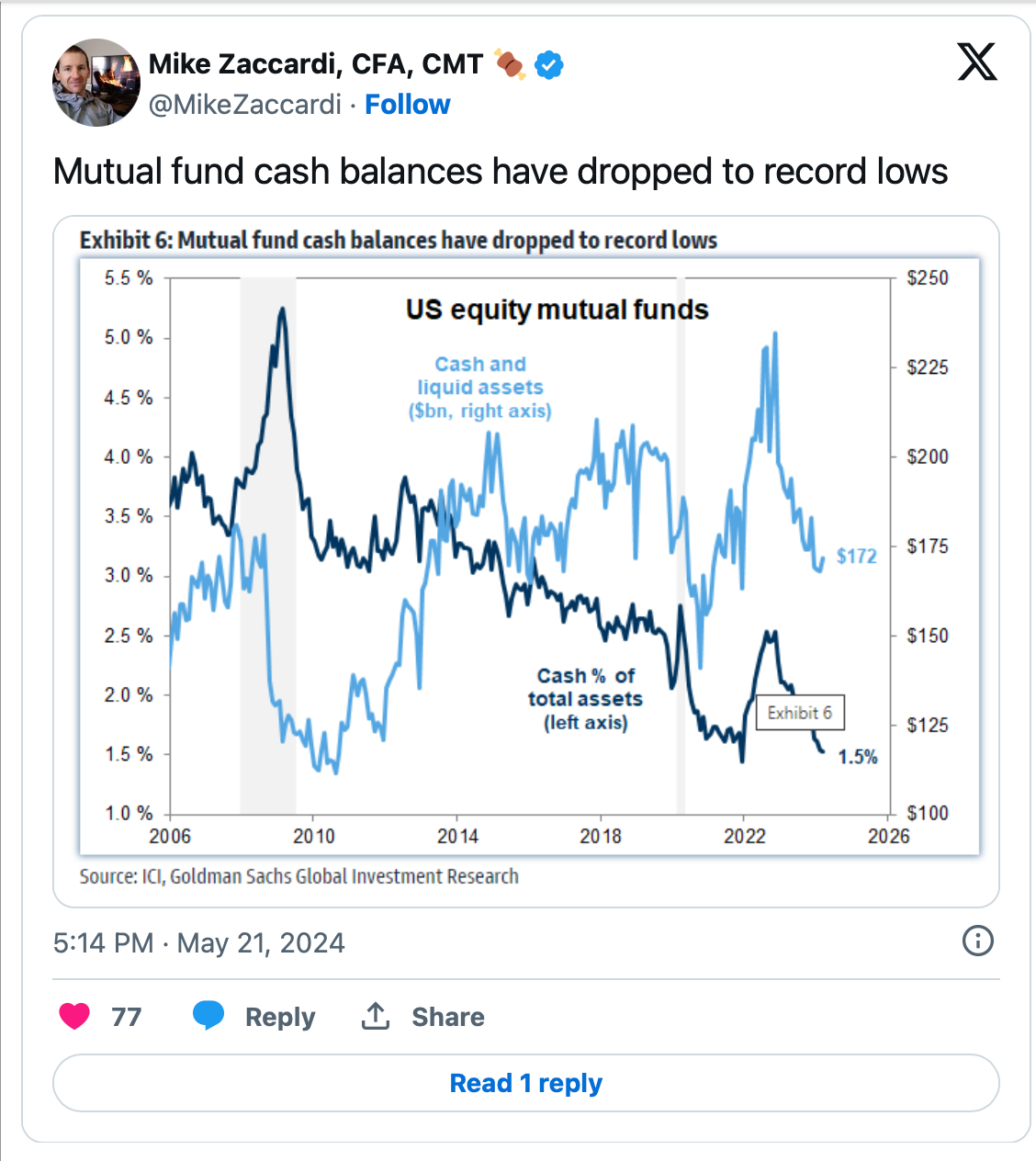

Mutual Fund Cash Balances

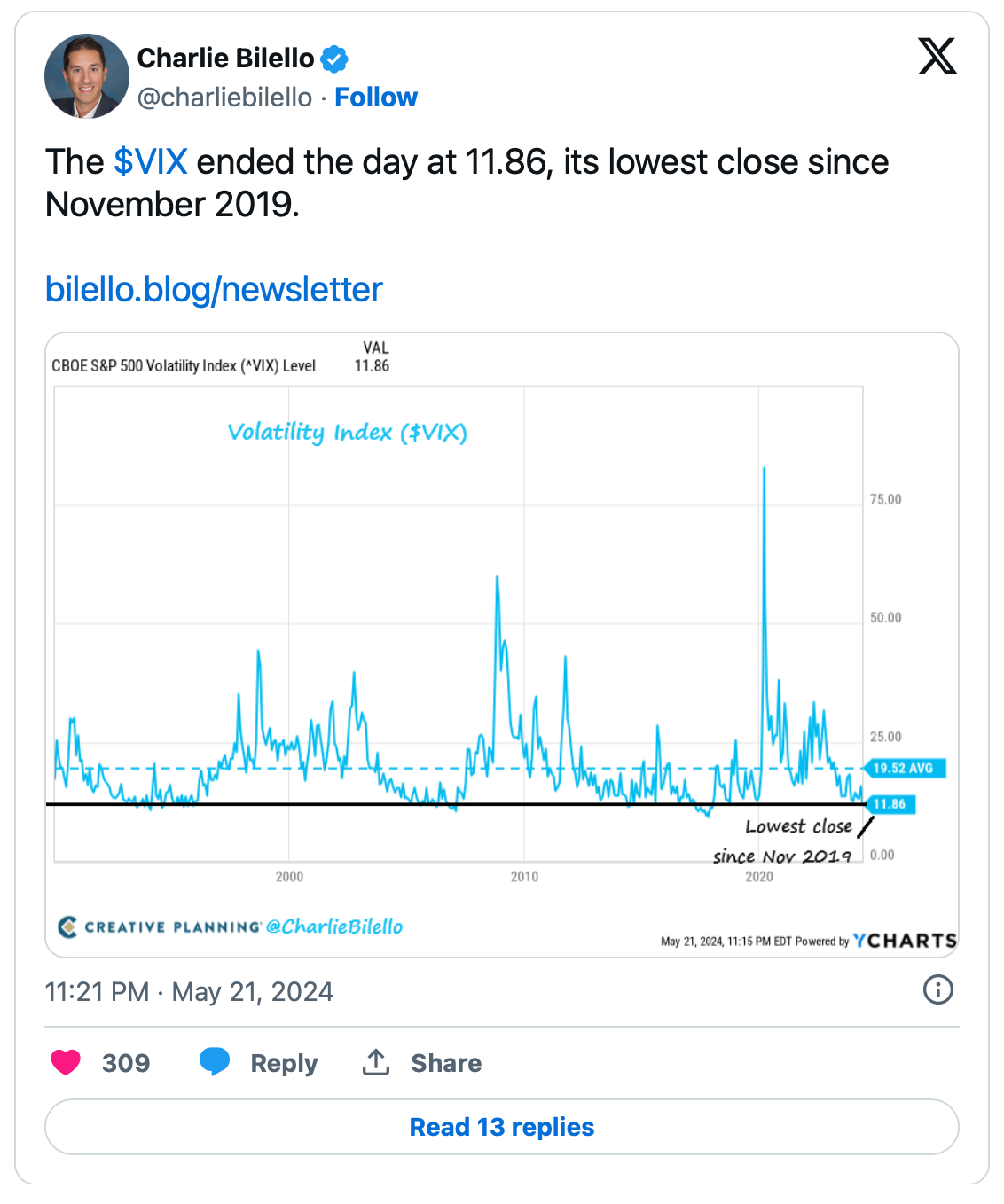

The VIX

VIX is a measure of investor sentiment and risk appetite. Recently VIX closed at 11.86 — at the lowest since November 27 2019. It still remains under 13 today:

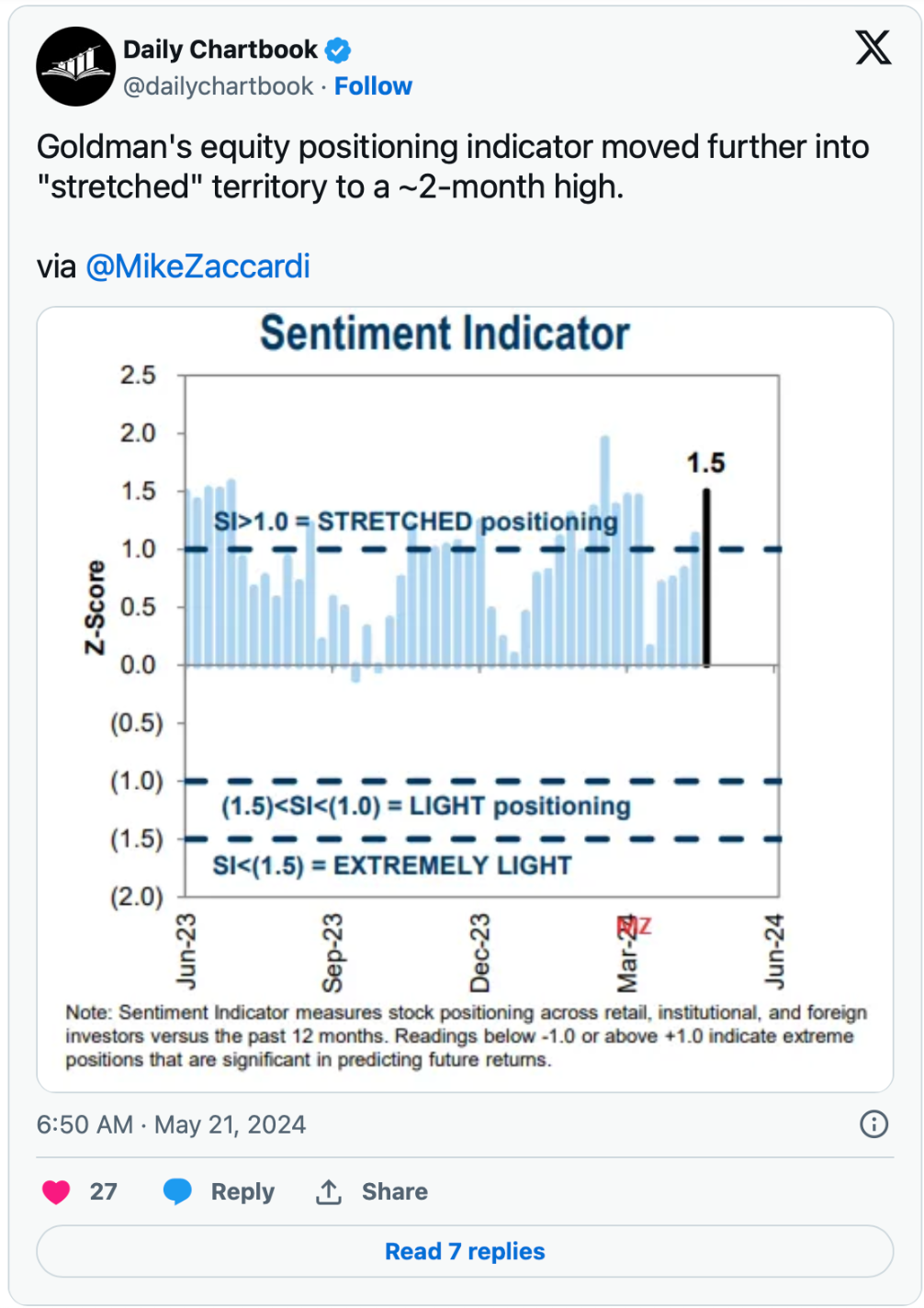

As investors position much more bullishly:

Inflation

Depending on your methodology, core services inflation rose by five to six percent last month. Now commodities (goods inflation) have begun to revive. Higher inflation for longer means higher interest rates for longer:

The Economy

As risks of higher inflation increase, the risks of slowing domestic economic growth are on also on the rise. I call this "slugflation" — a condition unfriendly to equities:

Some of My Holdings

Representative longs include Occidental Petroleum OXY, Chevron CVX, Exxon Mobil XOM, Green Thumb Industries GTBIF, Trulieve TCNNF, DraftKings DKNG, Elanco Animal Health ELAN, Freshpet FRPT, Morgan Stanley MS, Goldman Sachs GS, Procter & Gamble PG, Green Brick Partners GRBK and Valvoline VVV.

Representative shorts include McDonald's MCD, Starbucks SBUX, Winnebago WGO, Walgreens Boots Alliance WBA, Medical Properties Trust MPW, FIGS FIGS, Pool Corp POOL, Sleep Number SNBR, B. Riley Financial RILY, Petco Health and Wellness WOOF, Blackstone Mortgage BXMT, Chegg CHGG and Freedom Holding FRHC.

Bottom Line

Investors see an Investing Nirvana today.

I see a great many uncertainties and a number of market-unfriendly outcomes.

Above all the market remains bifurcated and is not broadening out:

“Today the spread between the S&P [500]’s 0.85% gain and the Dow's -0.09% loss was 0.94 bp. Going back to 01/04/1982, the [S&P 500-Dow Jones] spread was greater than 0.90 bp only 71 times. That's 71 times over 10,700 days. 20 of those happened in 2000.”

- Walter Murphy

Rosie (Dave Rosenberg) responds:

That is a major “yikes!” We are living in a world of 1-in-150 events. The fact that the last time we saw such a massive divergence was back in 2000 surely is cause for pause. The stock market has hit such an extreme in terms of concentration risk that we have Nvidia’s market cap now exceeding the entire FTSE-100 in the U.K. and just three stocks in the S&P 500 (Nvidia, Microsoft, and Apple) represent over 20% of the index.

And equities remain as overvalued against interest rates than at any time in over two decades.

It is as simple as that....

More Pro:

- Fun Facts That Help Investors Make Money

- We Are Calling Up a New Portfolio Position From the Bullpen

- These Positions Can Help Traders Profit From Copper Gains

Note: The above has been extracted from some previous Diary submissions and from commentary provided to my investors at Seabreeze Partners.

At the time of publication, Kass was long and short the above names.