Who the Heck Is LifeMD and Why Does It Have a Chance?

Let's take a close fundamental and technical look at a low-priced healthcare name with a potential earnings catalyst on the horizon.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Who the heck is LifeMD?

LifeMD LFMD is a small-cap direct-to-patient operation headquartered in New York City. A very small-cap operation, with a market cap of a rough $300 million, which is only about $50 million away from being classified as a micro-cap.

The company operates its business through two segments, Telehealth and WorkSimpli.

The Telehealth segment provides a platform that integrates clinician-centric electronic medical record system, and algorithmic models meant to aid in case-load balancing, scheduling, customer relationship management, communications and a cloud pharmacy. The technology combined with its 50-state affiliated provider network, enables and manages the virtual treatment of various health conditions, including urgent, primary and chronic care.

The WorkSimpli segment provides workplace and document services. The online software works as a platform for users to create, edit, sign and share PDF-formatted documents.

Earnings

LifeMD will report its second-quarter financial results the week after next. Current consensus estimates (of just four analysts) is for a GAAP loss of $0.12, adjustable to $0.04 on revenue of $48.2 million. A sales number like that would be good for year-over-year growth of about 34% and would be a third consecutive quarter of 30%+ annual growth. For the March quarter, LifeMD posted a GAAP loss per share of $0.19, adjusted up to $0.01 on revenue of $44.14 million.

At that time, LifeMD had not only seen growth across both business segments but had 42,000 weight-loss subscribers. That number had exceeded 50,000 by the time the March-quarter financials were released on May 8. On May 8, the company also guided full-year revenue to $205 million+, which was up from prior guidance of $200 million. Wall Street currently sees the full year at $206 million.

Fundamentals

Over the trailing 12 months as of March 30, LifeMD had generated operating cash flow of $16.6 million. Out of that number came just $300,000 in capex spending, leaving free cash flow of $16.3 million. Out of that number, the company paid $3.1 million in preferred stock dividends.

At that time, the balance sheet showed a cash position of $35.1 million and inventories of $2.4 million and current assets of $44.4 million. Current liabilities add up to $44.7 million, including shorter-term debt of $4.1 million, but also unearned revenue of $13.2 million.

This puts LifeMD's headline current and quick ratios at 0.99 and 0.94, respectively, which isn't so hot, especially for a tech firm. However, once adjusted for those unearned revenues, which are not financial obligations, these ratios rise to a much more acceptable 1.41 and 1.33, respectively.

What Wall Street Thinks

As far as I can tell, Sarah James of Cantor Fitzgerald is the only highly rated (5 stars at TipRanks) sell-side analyst that follows the stock.

She currently rates LFMD as a "buy" with a $15 price target.

What I Think

This is a very small business that trades at a fair price that does have a chance. The stock is not GAAP profitable, so there is no P/E ratio, but it does trade at 1.5 times sales.

Interestingly, at least as recently as two weeks ago, more than 11% of the entire float was held in short positions, so there is some risk of a short=squeeze happening at some point.

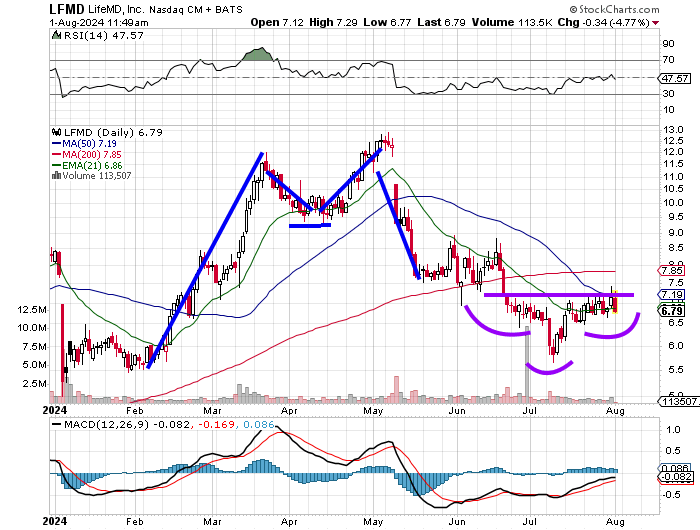

Notice in the chart, above, that LFMD formed a double-top reversal earlier this year with a $9.25 pivot. That story played out into severe selloff as was predictable.

Now, the stock battles with its 21-day exponential moving average (EMA) and 50-day simple moving average (SMA), as the daily Moving Average Convergence Divergence (MACD) has improved over the past three weeks. Though still negative, the 12-day EMA stands above the 26-day EMA, while the histogram of the 9-day EMA is firmly entrenched in positive territory.

You can also see that the stock has formed an inverse head-and-shoulders pattern with a neckline of $7.20 or so. A break above that spot into or post-earnings could produce a run at the 200-day SMA. That, if it occurred, would produce a price target around $9.50.

More Stocks Under $10:

- I've Got My Eyes on an Apparel Group After Surprise Profit Report

- This Iconic Retail Chain Got Rocked, But Absurd Yield Is Still Possible

- Time to Get Fired Up About Rocket Lab

At the time of publication, Guilfoyle had no positions in any securities mentioned.