Time to Get Fired Up About Rocket Lab

This is another one of my lower-priced, long-term investment ideas where I am putting my money where my mouth is.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

It's been a few months since I've publicly taken a look at an old Sarge name: Rocket Lab USA RKLB. I have been getting sporadic requests for a follow-up piece on this one, so I figure this week is as good a time as any as the company reported its first-quarter results this past Monday afternoon. This is not a name followed by a lot of readers, but it's produced for the retail investor, and has been in rally mode since bottoming in mid-April.

Late Monday, for the three-month period ended March 31, Rocket Lab posted a GAAP loss per share of $0.09 on revenue of $92.767M. The bottom-line print beat Wall Street expectations by a penny, while the top line number missed by a smidge. That revenue number was also good enough for year-over-year growth of 69%. But that tells just a slice of the whole story.

Rocket Lab ended the quarter with an order backlog of more than $1B. During the quarter, the company launched four Electron missions for commercial and national security customers across launch sites located in the U.S. and New Zealand. It also kicked off a new program as the contractor for a $515M Space Development Agency to design, build and operate 18 satellites for the Tranche 2 Transport Layer-Beta.

The Space Development Agency is a direct reporting unit within the United States Space Force, headquartered at the Pentagon. A primary focus of the agency is missile defense using global satellite constellations made up of many low-cost satellites.

Operations

As revenues grew 69% to $92.767M, the cost of those revenues increased 41.3% to $68.593M, leaving a gross profit of $24.174M (+280%) on a gross margin of 26.1% up from 11.6%. Operating expenses advanced 28.4% to $67.253M, leaving an operating loss of $43,079M, narrowing from a loss of $46.017M.

After accounting for interest and taxes as well other income and losses and unrealized gains and losses on investments, Rocket's net loss was $47.598M versus a loss of $46.187M. After dilution, this works out to a GAAP loss per share of $0.09, which compares to a loss of $0.10 for the year-ago period.

Guidance

For the current quarter, Rocket Lab sees revenue of $105M to $110M. At the midpoint, this would be above the $105M that Wall Street was looking for, while also reflecting annual growth of roughly 74%. The company sees a GAAP gross margin between 24% and 26%, and GAAP operating expenses between $74M and $76M. Interest income is expected for the quarter to reach $1M, while the company expects to suffer an adjusted EBITDA loss of $23M to $25M.

It's not in Rocket Lab's guidance, but Wall Street's consensus is for a full-year GAAP loss of $0.41 per share for this year and then the Street sees that loss being more than halved (to $0.15) for full-year 2025.

Fundamentals

For the three months reported, Rocket Lab generated operating cash flow of -$2.588M, versus -$25.383M for the comparable period one year ago. Tack on capex spending of $19.177M, which was up from the year-ago period, and the company is left with free cash flow of -$21.765M, which was an improvement from -$38.059M for the year ago comp. Obviously, Rocket Lab is not yet in a position to start thinking about returning capital to shareholders.

Checking out the balance sheet, Rocket Lab has a beefy cash position of $492.522M and inventories of $99.901M. This leaves the company with current assets of $725.623M. Current liabilities add up to $232.462M including short-term debt of $10.996M. These numbers put the company's current ratio at a very robust 3.12, and its quick ratio at a still muscular 2.69.

Total assets amount to $1.182B, including $137.865M worth of "goodwill" and other intangibles. At less than 12% of total assets, this is not a problem. Total liabilities less equity comes to $702.978M, including $396.546M in long-term debt. This is a very strong balance sheet, and that debt-load could be paid off completely out of cash. The one catch is that most of that debt — $343.829M — is in the form of convertible senior notes, so the company is at risk, if the stock price rises steadily, of some further dilution.

These notes, for the most part, come due in 2029, and run with a conversion price (there's a formula) of approximately $5.13 per share of common stock.

Wall Street View

I have only seen two sell-side analysts react to Monday's release, and neither did anything earth-shattering. They are both rated at five stars by TipRanks.

Jason Gursky of Citigroup reiterated his "buy" rating and $5.45 price target for RKLB, while Matthew Akers of Wells Fargo reiterated his "hold" rating as well as his $4.25 target.

My Thoughts

This is another one of my lower-priced, long-term investment ideas where I am putting my money where my mouth (keyboard) is. I have been buying RKLB on dips, which worked out very well for us for most of the first three and a half months of the year. The business is growing. The more the U.S. Space Force relies upon Rocket Lab the better.

Over the past months, the company secured two contracts from the Space Force, one for $14M and another for $32M, adding some more beef to that already enormous backlog. The balance sheet is strong and will be able to sustain considerably more cash burn if necessary.

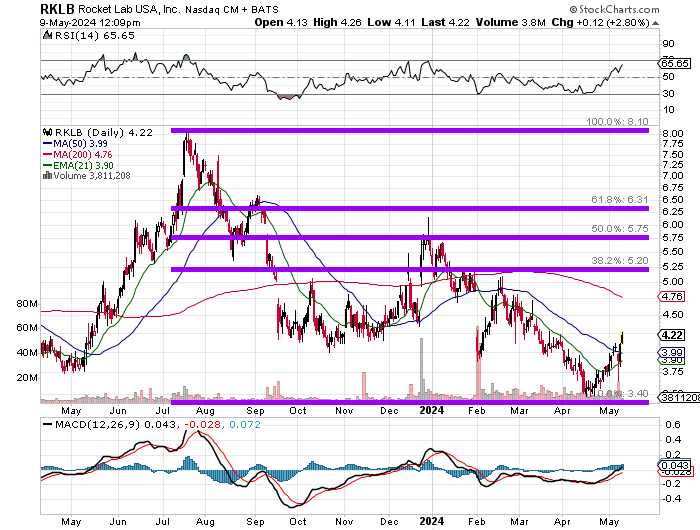

Readers will see the sharp rise in this stock's Relative Strength Index (RSI) reading and the steady improvement in its daily Moving Average (MACD). The stock has now retaken both its 21-day exponential moving average (EMA) and 50-day simple moving average (SMA).

There is no reason to think that the 200-day SMA at $4.76 cannot come into play, and if it does, then investors can think about a 38.2% Fibonacci retracement (at around $5.20) of the stock's July 2023 through April 2024 selloff. At that point, convertible note holders will wake up and the stock in all likelihood will go through some growing pains. That said, that's my price target for now: $5.20. My average point of entry is currently $3.98.

At the time of publication, Guilfoyle was long RKLB equity.