I've Got My Eyes on an Apparel Group After Surprise Profit Report

G-III Apparel Group beat expectations on profit, showing year-over-year growth, and I'm looking out for a buy signal.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

On Thursday morning, G-III Apparel Group GIII released the results of the firm's fiscal first quarter. For the period ended April 30, 2024, the manufacturer of coats, jackets, trousers and sportswear posted a GAAP EPS of $0.12 on revenue of $609.747 million. The surprise profit landed about $0.15 above expectations, and the revenue print fell short of projections while showing year-over-year growth of 0.5%.

The firm raised guidance for net income for the full year, which is why the stock is trading higher. We'll get to that down below. The firm did also amend and upsize its asset-based lending (ABL) credit facility to $700 million and extend the associated maturity into 2029.

A Dive into GIII Operations

As sales grew 0.5% to $609.747 million, the cost of those sales decreased 1.7% to $350.854 million. This took gross profit up 3.6% to $258.893 million. This was on a gross margin of 42.5%, up from the year ago comp of 41.2%.

Administrative expenses increased 3.8% to $236.621 million as depreciation and amortization grew 33.3% to $8.768 million, leaving operating income of $13.504 million (-11.5%). After accounting for other income and losses, interest and taxes, net income attributable to shareholders hit the tape at $5.802 million, up from the year ago print of $3.236 million. After dilution, this works out to a GAAP EPS of $0.12, up from $0.07 for the same period last year.

Guidance on GIII

For the current quarter, GIII projects net sales of roughly $650 million, which would be down from the year-ago comparison and below consensus view for $665 million as well. Net income for the quarter is seen at $10 million to $15 million, which would work out to EPS of $0.22 to $0.32. That would be down from $0.35 for the year ago period as well as below the $0.33 that Wall Street had in mind.

For the full year, the firm projects net sales of about $3.2 billion and net income of $170 million to $175 million. This works out to a GAAP EPS of $3.58 to $3.68. While, again, these numbers would all be contractions from the year prior, Wall Street had been looking for revenue of $31.9 billion and an EPS of $3.54. so this guidance is being taken as a positive.

GIII's Fundamentals

The firm released limited information regarding cash flows and its balance sheet at this time. Readers know how much I love that. Last quarter, the firm released its earnings on March 14, and its statement of cash flows and balance sheet in a Form 10-K on March 25, so we are probably about a week and a half away from seeing more complete data that would enable a proper fundamentals analysis of the name.

We do know that GIII Apparel ended the quarter with a cash position of $508.434 million, inventories of $479.671 million and total assets of $2.565 billion. Total debt load came to $426.351 million, which is not only less than the firm's cash position, it's down 21.5% over the past 12 months. The balance sheet is probably in decent shape based on those numbers, but we'd like to see it when the quarterly performance is reported.

My Thoughts on GIII Investment

The full-year guidance is stronger than expected, yet still shows declines. The quarterly guidance is not so hot. We can't really do a proper fundamental analysis, but Wall Street is liking what it saw this morning. In addition to the above material, GIII announced this morning that the firm had acquired a 12% stake in All We Wear Group, which will now manage DKNY, Donna Karan and Karl Lagerfeld on the Iberian Peninsula.

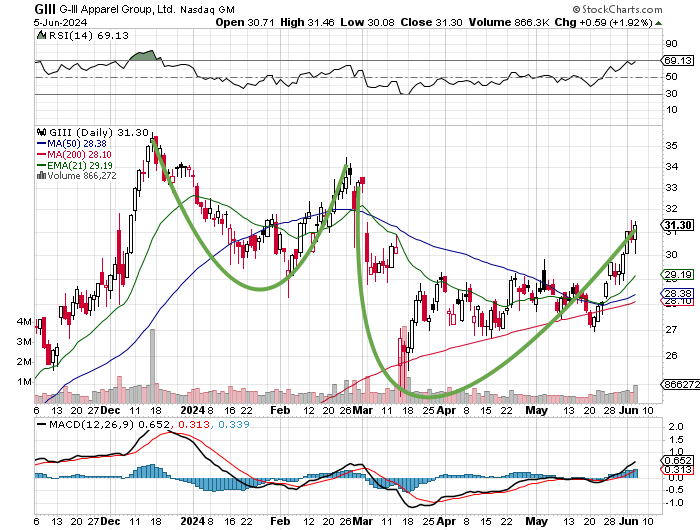

Relative strength is solid. The daily MACD is looking bullish. The stock has developed a second cup pattern since the start of December. This has me trusting the current pattern a little less. The pivot stands at $34.

I don't think I buy into this name unless I see that pivot taken and held, or if I just love what I see in the cash flows and the balance sheet once that data is more complete. For me this is a "hold" until one of those two conditions is met. I cannot yet bless the name.

At the time of publication, Guilfoyle had no positions in any securities mentioned.