Walmart: Far From Bargain-Priced

There are plenty of great buys out there. Let me show why Walmart isn't one of them.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The largest stock-price gains come when embedded growth has yet to be reflected in the share price.

That occurs when P/E compression has trimmed multiples from pricey to bargain levels. Walmart WMT, though, has experienced exactly the opposite. Over the past decade WMT went from a 15.1 P/E to its present multiple of about 28.5 times its FY 2024 estimate.

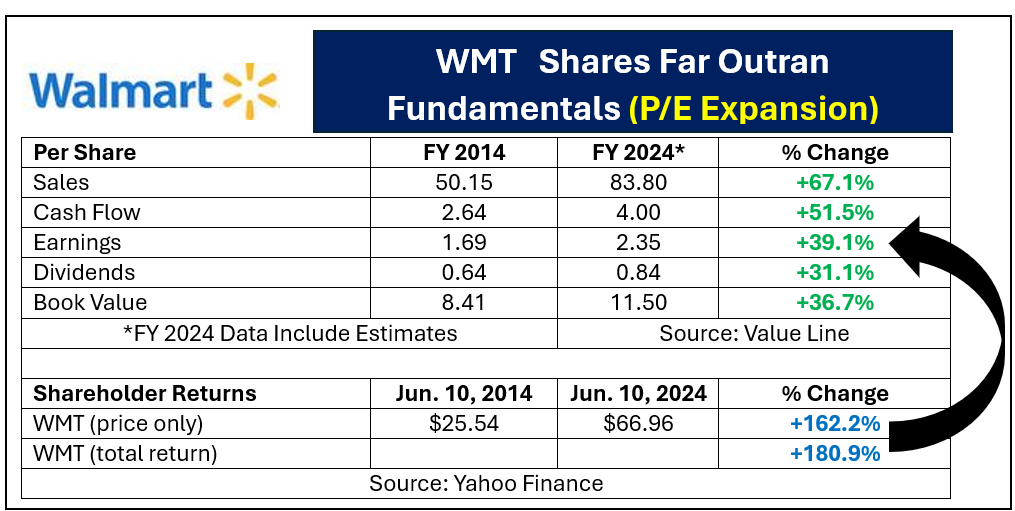

Long-time holders of the shares benefited greatly. Decade-long owners of WMT captured greater than 180% in total return even as EPS, dividends and book value only advanced by from 31.1% to 39.1%.

Those buying WMT now are paying highly inflated prices for shares which deserve to be selling well below today’s quote.

Why do I say that?

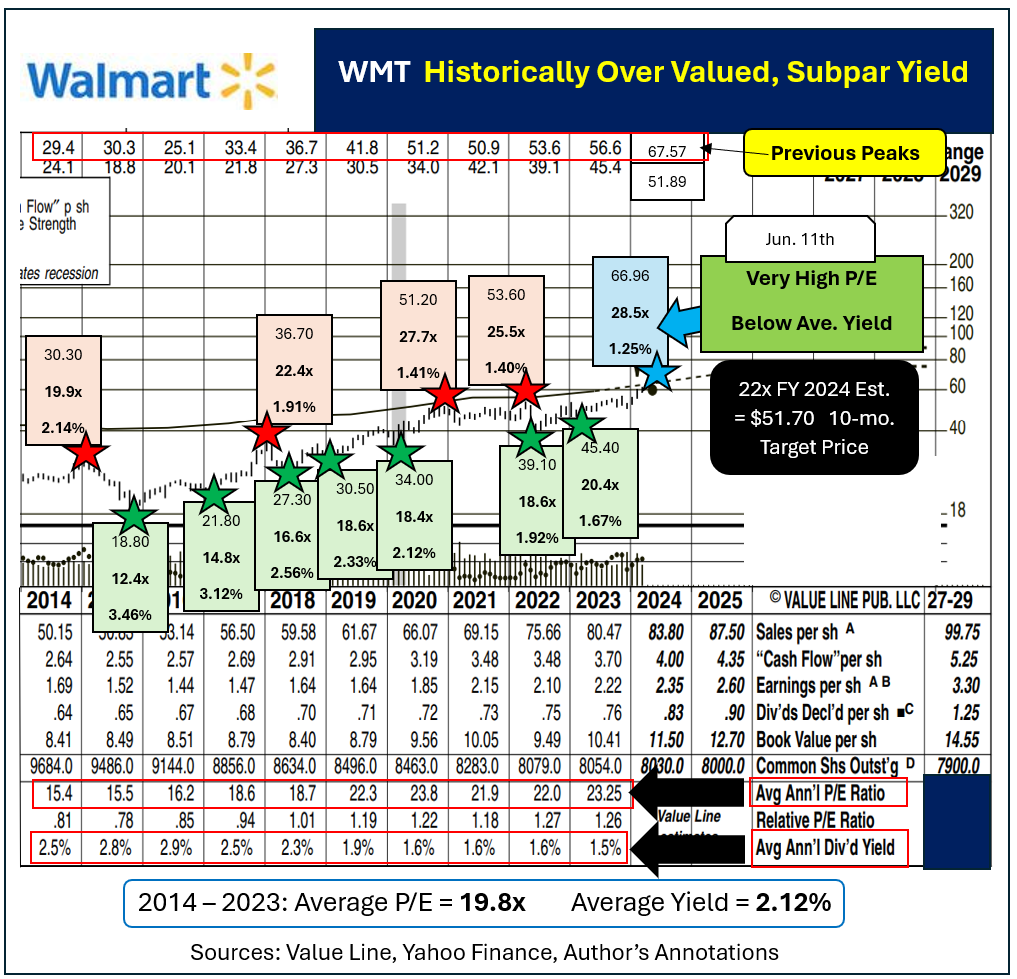

The data below show Walmart’s average P/E since 2014 was just 19.8x, accompanied by around 2.12% in yield. Based on Value Line’s EPS for WMT’s current year it now fetches about 44% above that long-term multiple. Its current yield is now almost 28% lower than its typical level.

Six of the most recent “best entry points” (green-starred below) saw investors pay between 12.4x and 18.6x forward earnings. Buying in when shares trade below their normalized valuations is almost always a winning move. The biggest gains came from getting into WMT when its yield was clearly above its average level.

Walmart’s four “should have sold” moments (red-starred) all occurred when the stock was selling for higher than its 10-year average P/E. Those multiples ranged from 19.9x to 25.5x earnings.

From today’s multiple the odds are heavily stacked in favor of P/E compression, rather than maintenance at this excessive level, or a further P/E expansion.

What Is WMT Worth?

Assume a still higher-than-typical P/E of 22x and the shares would sell for only about $51.70 by the spring of 2025. That implies downside risk of at least 22.7%. Reverse engineering the current annual dividend rate of $0.84 to a typical 2.12% generates a target price range of just $39.62.

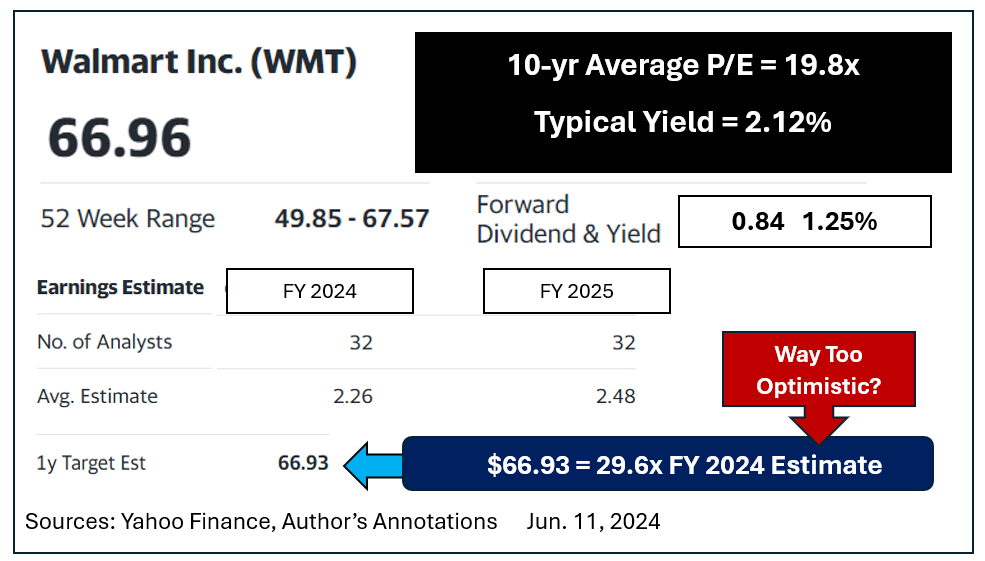

Yahoo Finance, who I often disagree with, carries a 12-month goal price for WMT of $66.93. I consider than way too optimistic as it assumes WMT will continue to command a greater than 51x multiple.

Even if they prove correct there is no obvious upside over the coming year.

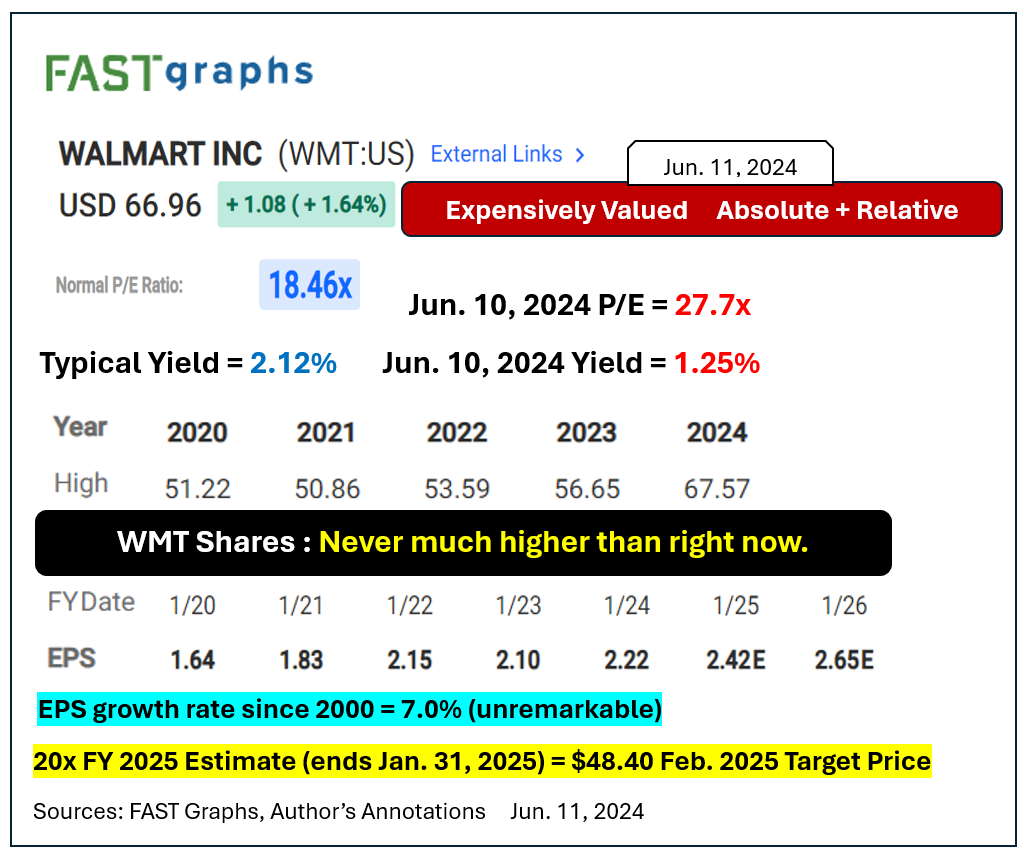

Research from FAST graphs calls Walmart’s normalized P/E as about 18.5x. Its EPS estimate for FY 2024 runs a bit higher than both Value Line’s and Yahoo Finance’s.

If WMT returns to a more logical 20x multiple on that higher earnings assumption the shares could fall back to about $48.40.

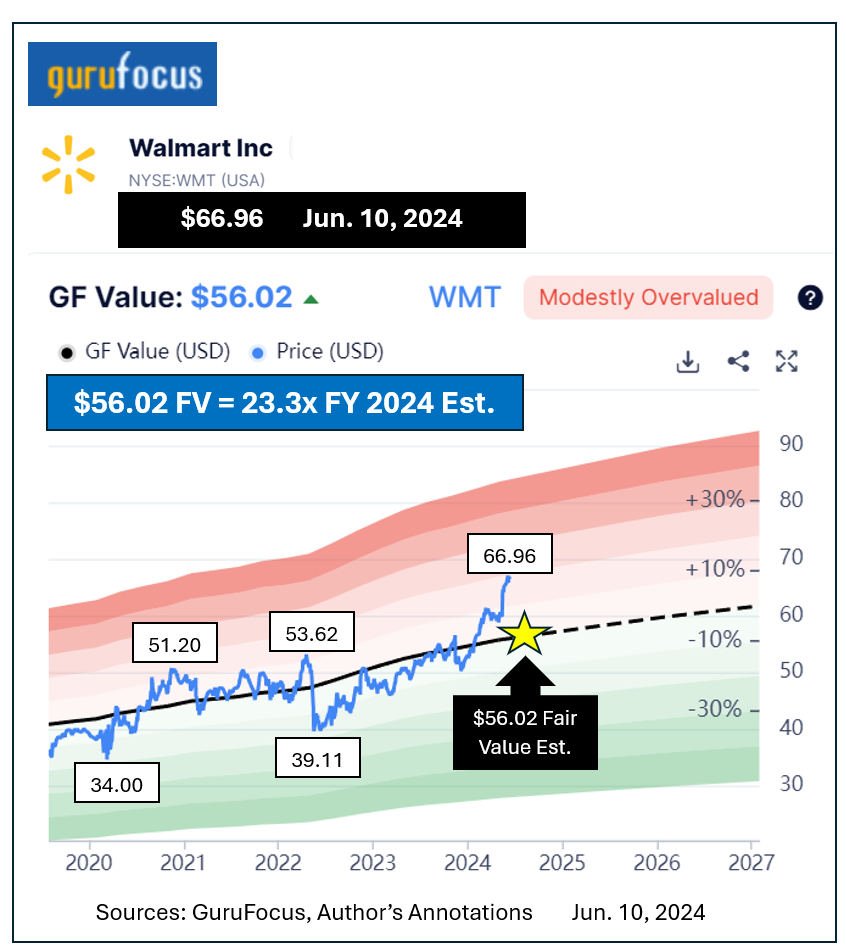

GuruFocus research sees present-day fair value for WMT as $56.02. That middle-of-the-road projection assumes the stock should trade for about 23.3x this year’s estimate.

That is perhaps a bit enthusiastic but not out of the question. Regressing to that price would deliver a 16.3% decline from its June 10, 2024 closing quote.

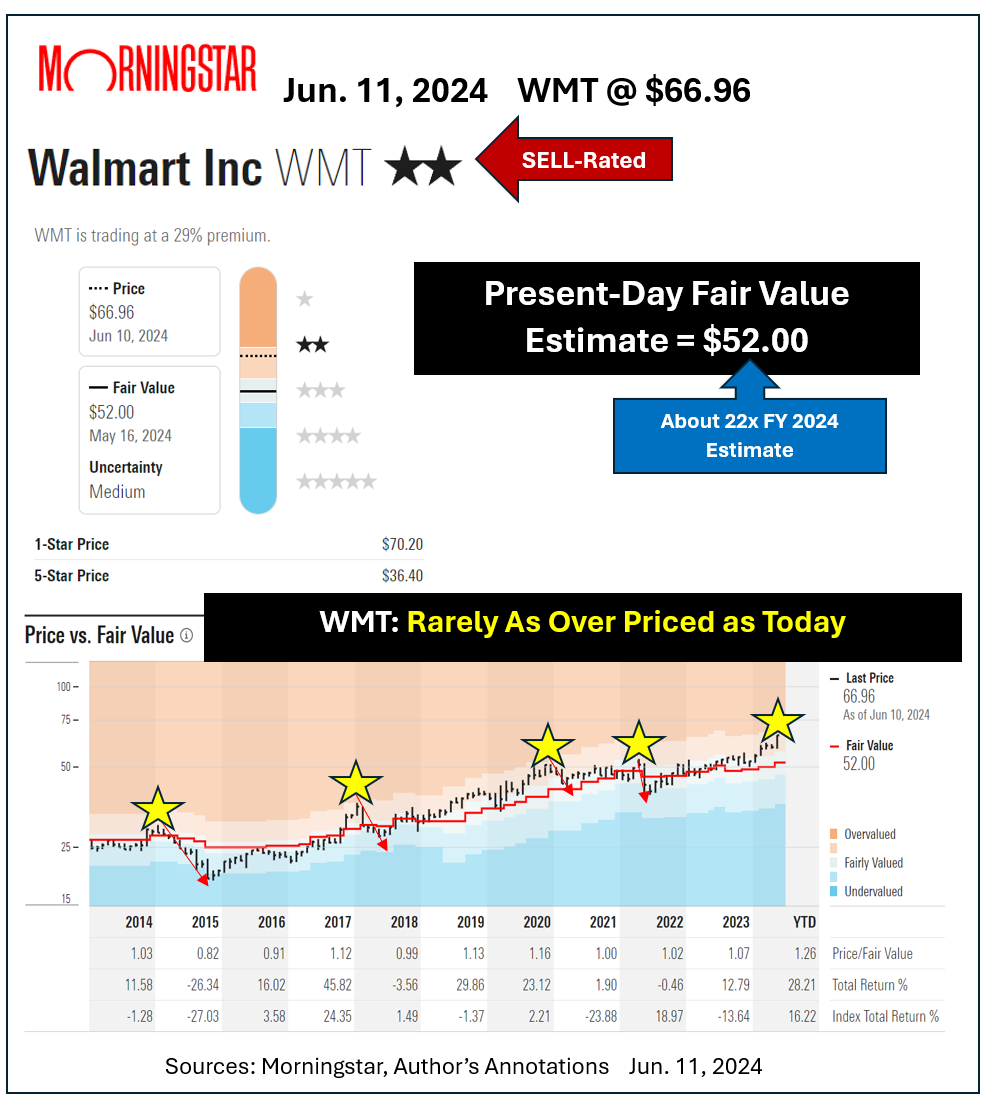

Independent research from Morningstar calls WMT a 2-star, out of 5, "sell." It sees present-day fair value as $52/share. If they are correct WMT could fall by around 22.3%.

Morningstar’s price-to-fair value chart clearly illustrates how overpriced WMT is compared with it past decade’s trading history.

Each of the four sojourns into similarly pricey territory (yellow-starred below) saw traders suffer fairly sharp corrections. The recent run-up figures to precede a similar fate for those who fail to sell, or insist on buying at WMT’s presently expensive valuation.

There are plenty of great buys out there. Why hold or purchase Walmart at such a foreboding time?

If you own WMT consider taking profits. If you were thinking about buying into WMT based on momentum and a great technical chart, think again.

More Paul Price:

- Forget Meme Players… What Is GameStop Really Worth?

- Is Value Investing Dead? You Make the Call

- Buying Income Is Hazardous to Your Wealth

At the time of publication, Price had no positions in WMT shares or options.