Forget Meme Players… What Is GameStop Really Worth?

Management has been given a green light to invest excess balance sheet cash in securities of other companies. That makes GameStop into a mini mutual fund with very uncertain prospects.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

All it took for GameStop GME shares to skyrocket this week was the following graphic from Roaring Kitty posted on X (formerly Twitter).

After three years or so of radio silence, Roaring Kitty was “leaning in” on meme stocks once again.

Masses of his followers put up their own money to “punish evil short sellers.” In the short-run at least they succeeded wildly.

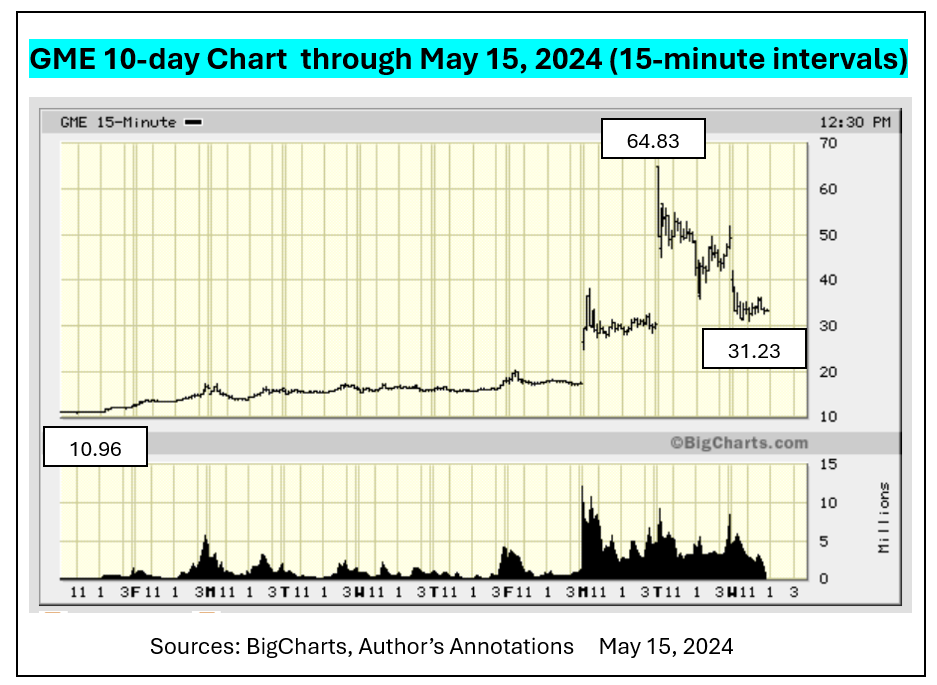

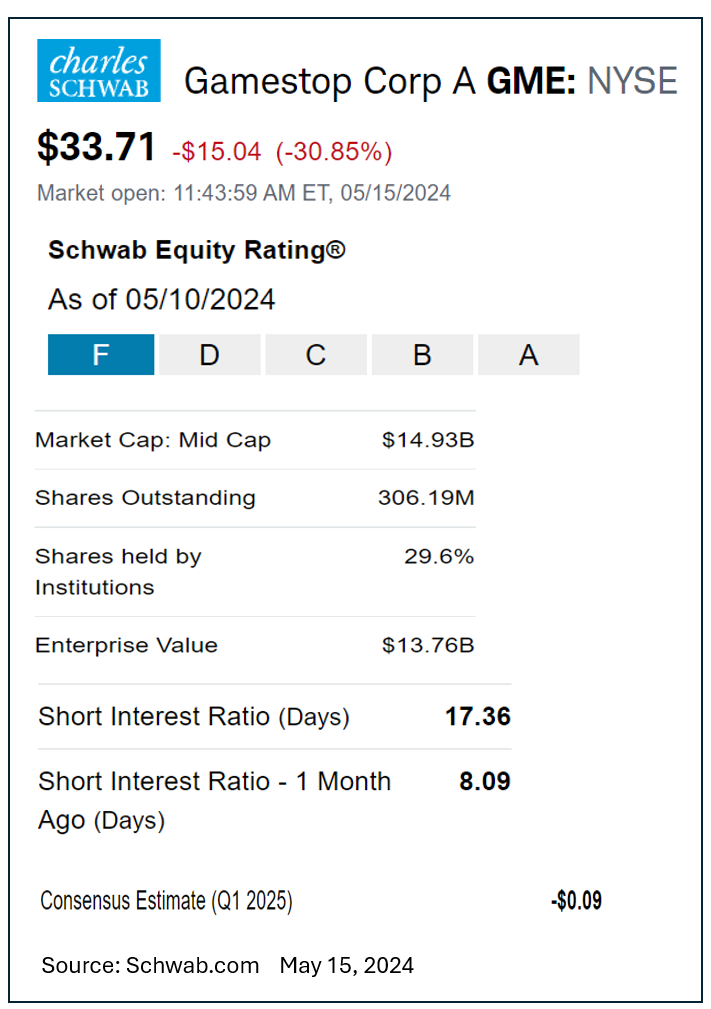

Even after calming down a bit GME was still fetching about $33 around noon on May 15.

TheStreet Pro tasked me to calculate a fair value estimate for GME to bring some sanity to this situation.

Here goes.

At present GME is worth whatever people are willing to pay for it. Over the long run it will settle back into some semblance of what it should be valued for based on fundamentals, plus some premium assigned simply to the likelihood that weeks like this can push it higher due to meme-stock manias.

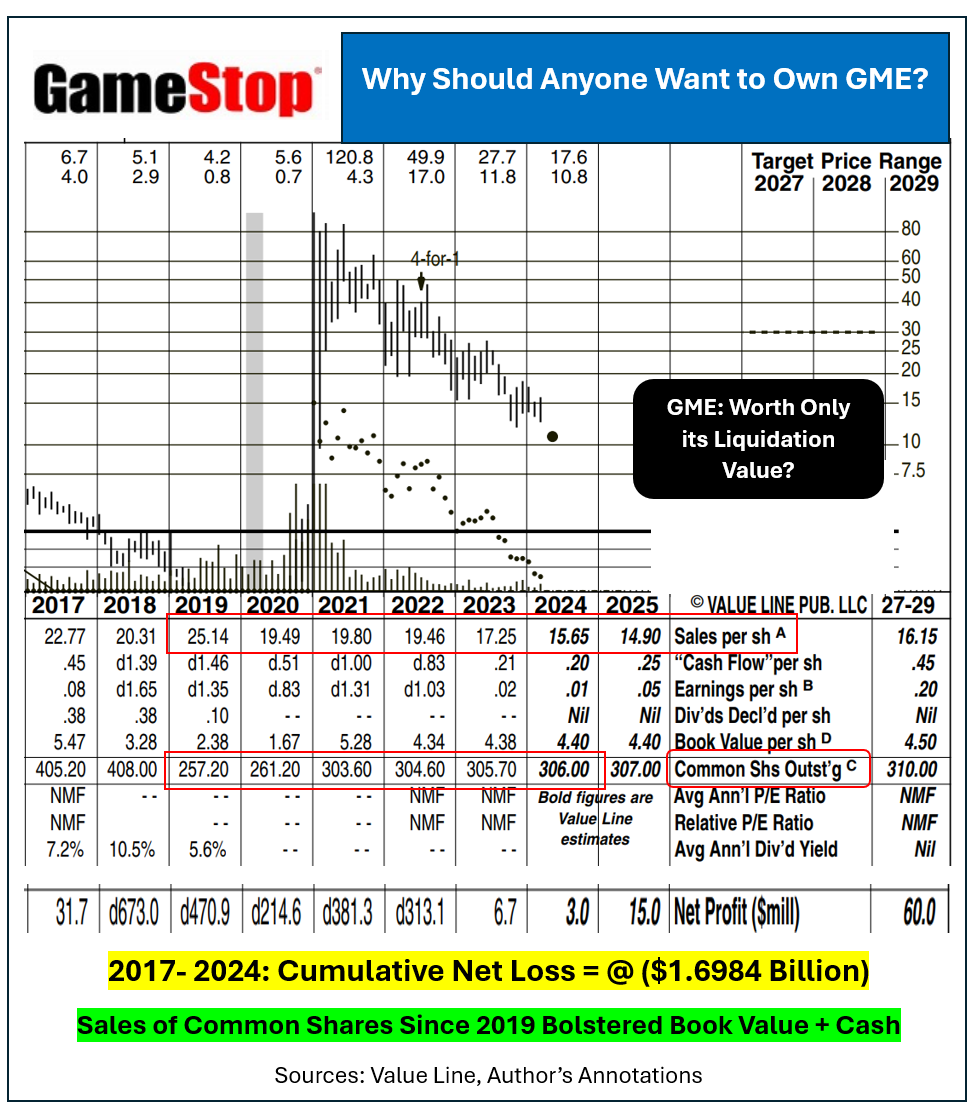

Revenues have been falling since 2019. Cumulative net losses since 2017 total about $1.7 billion assuming 2024 plays out as expected.

Book value advanced from a low of $1.67 per share at the end of 2020 to around $4.40 as management took advantage of previous meme-stock rallies to issue secondary shares at highly inflated prices.

Those equity sales allowed for cash holdings, as of Feb. 3, 2024, to stand at $1.199 billion versus total debt of just $28.8 million. That turned this crappy retailer’s shares into a net debt-free status.

Barring a return to the significant losses incurred from 2018 through 2022 the company is in decent financial strength.

Management has been given a green light to invest excess balance sheet cash in securities of other companies. That makes GameStop into a mini mutual fund with very uncertain prospects.

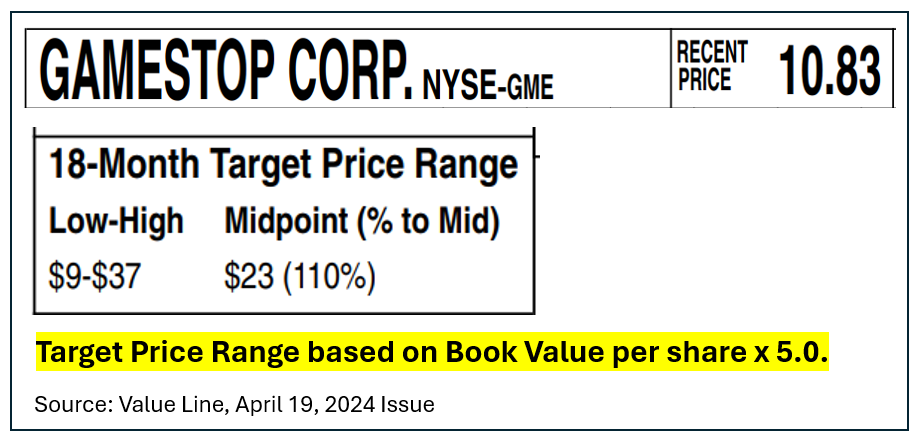

Back in April, when GME fetched $10.83, Value Line looked for a midpoint goal price of $23 by around October 2025. That was based strictly on a 500% of book value valuation. That seems absurd to me.

Berkshire Hathaway BRK.A BRK.B only commands about 1.5-times book value at relatively high points in terms of valuation.

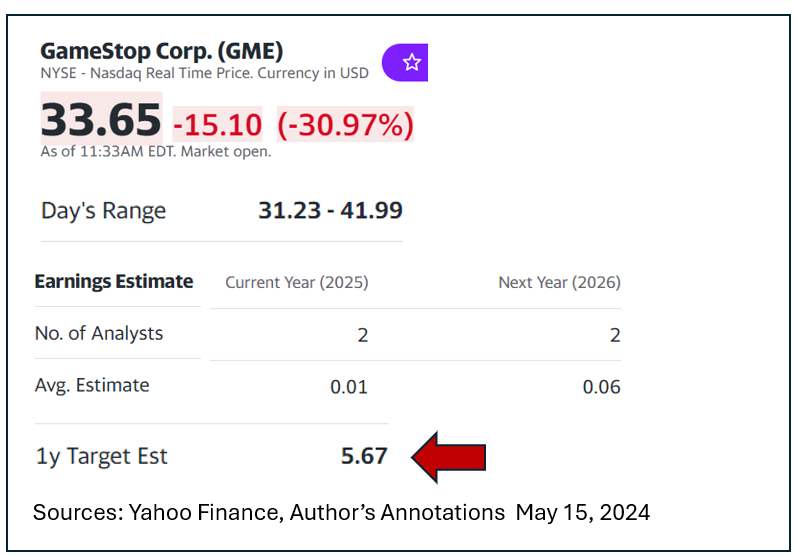

Yahoo Finance calls for GME to be $5.67 by this time next year. That would represent about 1.3-times book value and a crazy high multiple of just a few cents per share in earnings.

Charles Schwab’s research organization rates GME with an “F” based on its actual business value.

At its May 15, 2024 quote of $33.71 GME has a market cap of $14.93 billion versus a book value of about $1.35 billion.

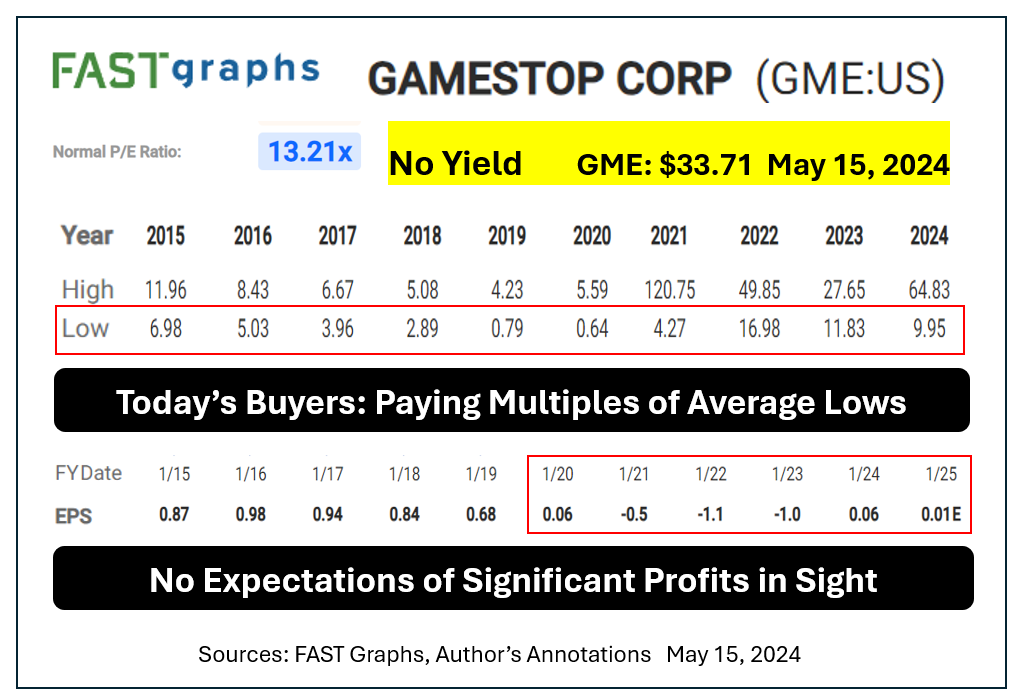

Quantitatively based FAST Graphs research thinks GME might post EPS of 6-cents this year. Most, or all of that, would come from interest earned on the treasury cash, not from selling video games.

There is no clear 12-month target stated, which seems appropriate based on fundamentals.

More From Paul Price:

Anyone holding GME shares today is simply gambling on where mindless trading will push the stock up or down.

The true value of GME based on facts would be its liquidation value. That would probably weigh in at no more than a dollar or two considering the commitments for leases and expenses for termination of the operating business.

What else is there to say?

At the time of publication, Price had no positions in GME, BKR.A or BRK.B.