Buying Income Is Hazardous to Your Wealth

Do not say you were not warned about the hazard of focusing on monthly income rather than total return.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Value Line’s April 19, 2024 issue covered full-page reports on both closed-end income and equity funds.

Income funds are typically owned by investors seeking “spending money” rather than those focusing on total return. That typically works out badly.

Why is that? There are two main reasons.

1 ) Stated yields are often notably higher than the actual total returns received over time.

2) Seeking out “spendable income” almost always delivers less to use later than if you invested wisely by being in the overwhelmingly better long-term asset class — equities.

I picked out four income funds and four equity funds to compare over the most recent five-year period ended Apr. 18, 2024.

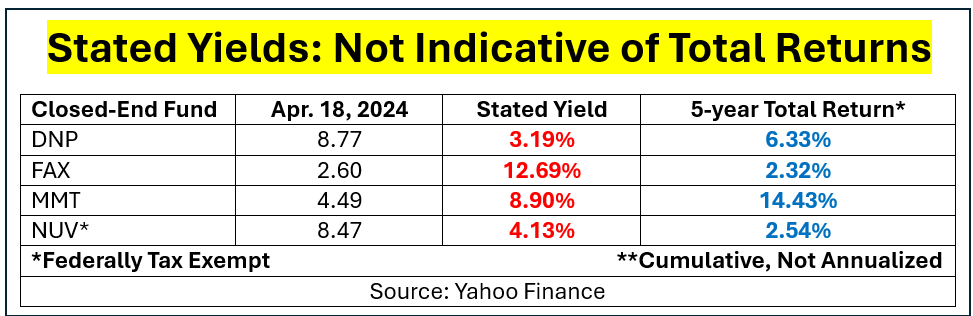

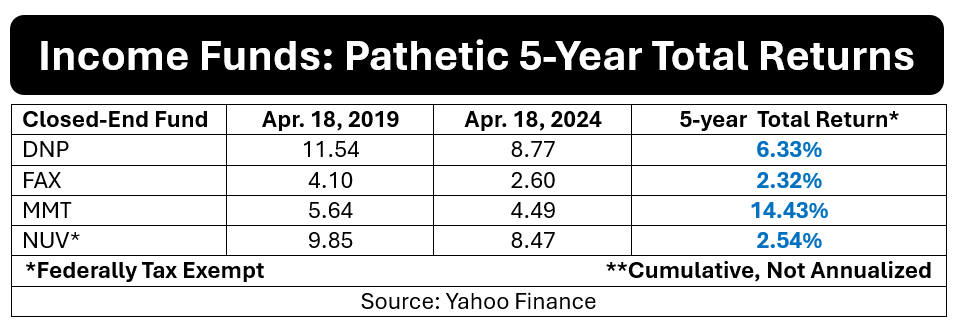

The bond funds were DNP Select Income DNP, Aberdeen-Asia Pacific Income FAX, MFS Multimarket Income Trust MMT, and Nuveen Municipal Value Fund NUV – a federally tax-free municipal bond fund.

The graphic below shows how deceptive stated yields can be. None of the four five-year total returns were anywhere close to what would have been derived from simply getting five times the current one-year yields.

FAX’s 12.69% stated current yield is particularly egregious in this regard. While its yield looks generous the actual trailing half-decade’s total return was the worst of all four income vehicles shown.

Actual data shown below illustrate how much the share prices declined over time, which detracted significantly from the total return figures.

A further negative to owning these funds was that income distributed on the non-municipal funds was taxable each year even as the poor annualized rates of return were achieved.

Avoiding federal taxation by owning the NUV muni-bond fund only netted about 0.5% annually in simple interest over the full five years. Trying to diversify with international bonds was even worse. So much for having decent actual money to spend.

An equal dollar value investment in all four of the income funds averaged only 1.28% annualized in simple interest per year.

How did that compare with “riskier” stock-based funds?

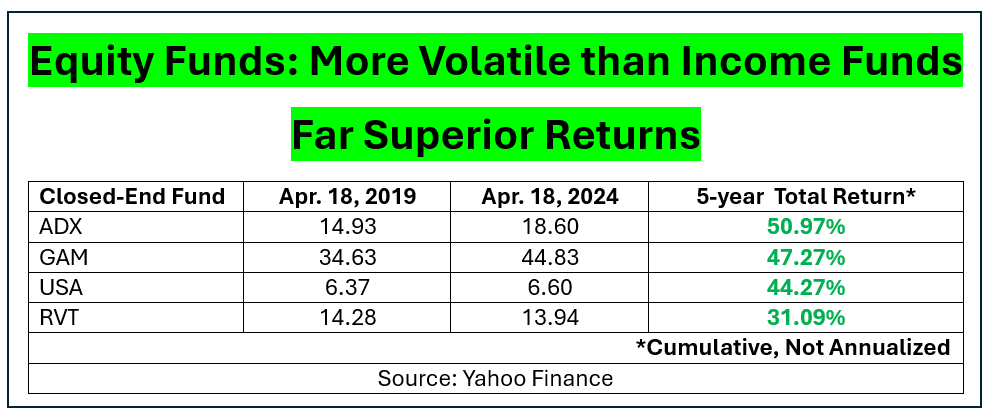

The four equity-based closed-end funds were Adams Diversified Equity ADX, General American Investors GAM, Liberty All-Star Equity Fund USA, and Royce Value Trust RVT- small-cap value fund.

The four stock-based funds showed five-year total returns ranging from 31.09% (for the out-of-favor RVT) to 50.97% (for the more traditional ADX). The benchmark S&P 500 ETF SPY earned 79.93% including reinvested dividends over that exact same period. That came out to a 15.98% annualized simple interest return.

An equal dollar investment in all four of the funds shown above averaged simple interest annualized returns of 8.68%. That was 6.78-times as much as the 1.28% annualized that the income funds averaged.

The half-decade documented was hardly a prime time for equity investing. Its starting point preceded the horrendous selloff during the Covid-panic of 2020 and a severe bear market in 2022.

Even relatively crappy equity funds far outperformed bond funds. The SPY’s total return was almost 12.5-times what was earned by opting for bond funds over index fund investing.

What Is the Lesson to Be Learned From All This?

Keeping even a part of your long-term assets (like 401(k), IRA or Keough plan money) in income-type investment choices is a fool’s game.

You will almost certainly end up with much less than if you simply accept market volatility as the price paid to become wealthy over time.

Having the most money possible in your retirement years is the only antidote to depending on government programs or having to delay your retirement due to lack of adequate cash.

Having modest monthly income to spend is inferior to accumulating enough in net worth to simply pay yourself generously out of dividends, capital gains and cash derived from occasional asset sales.

Do not say you were not warned about the hazard of focusing on monthly income rather than total return.

At the time of publication, Price had no positions in any of the funds mentioned or the SPY ETF. His own retirement portfolios are typically 100% invested in individual stocks, plus (short) covered calls when the premiums appear tempting.