There Is No Need to Go to War Over This Stock Pick

A major price plunge from these shares has created a major buying opportunity.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Helen of Troy HELE owns and distributes well-regarded brands in the beauty and household goods categories. Their major brands are shown below.

From 2008 through 2021 the firm posted fabulous results and steadily increasing share prices. Fiscal year 2008 EPS were $1.59. Stimulus checks fueled FY 2021’s EPS, which hit record earnings of $12.36 per share. The stock surged from $21.20 on July 24, 2008 to as high as $265.97 in January of 2021.

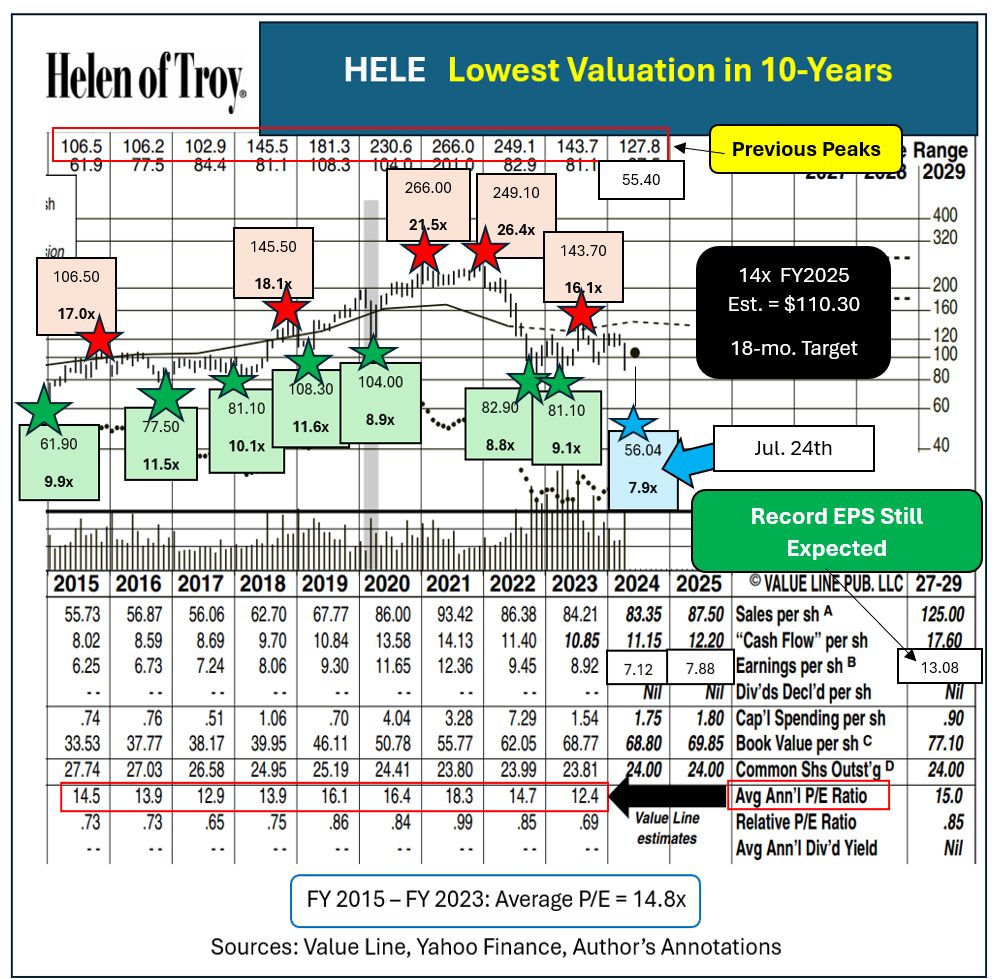

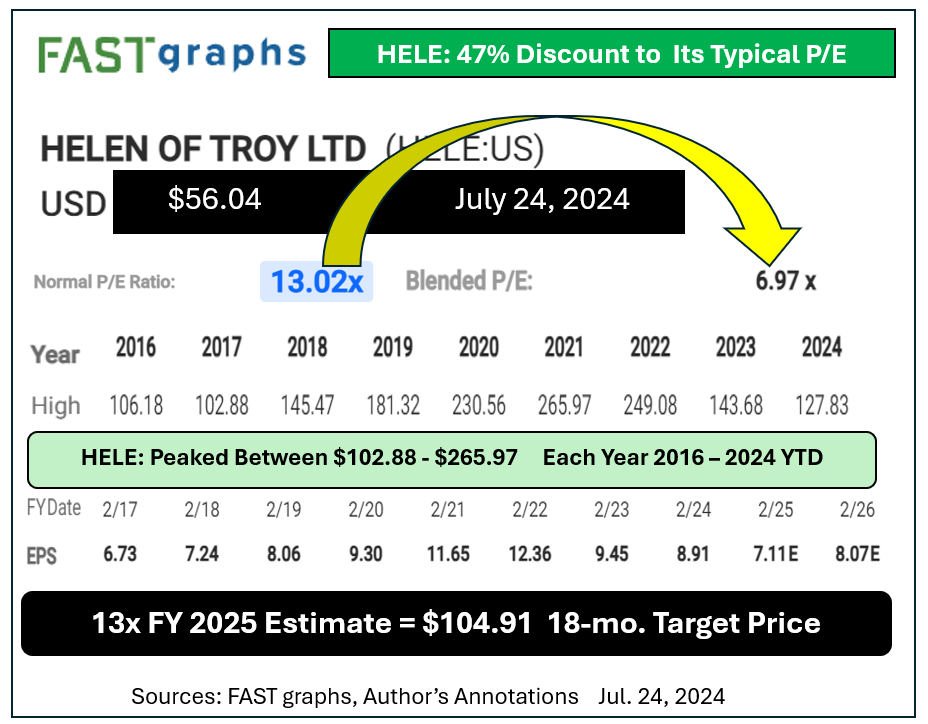

Results retreated a bit in FY 2022 and declined slightly more in FY 2023. Even so, HELE peaked from $102.90 to almost $266 during each of the 10 calendar years from 2015 right through 2024 year to date.

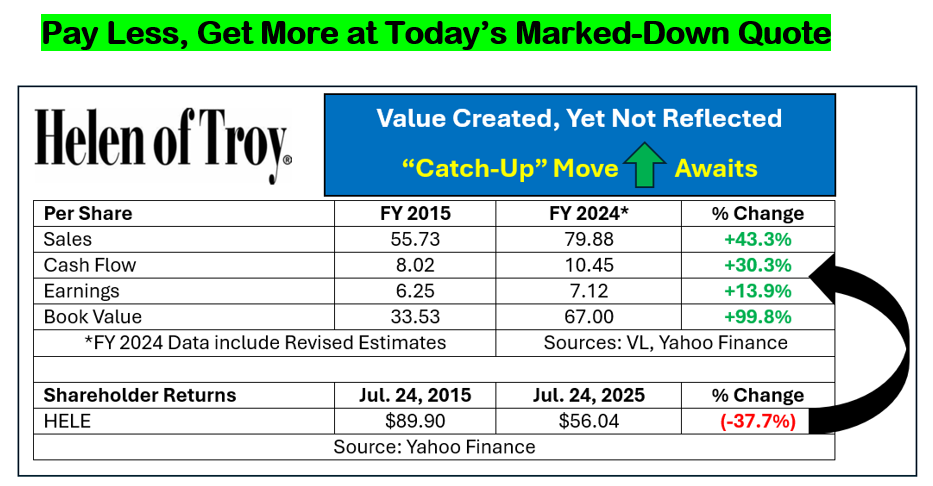

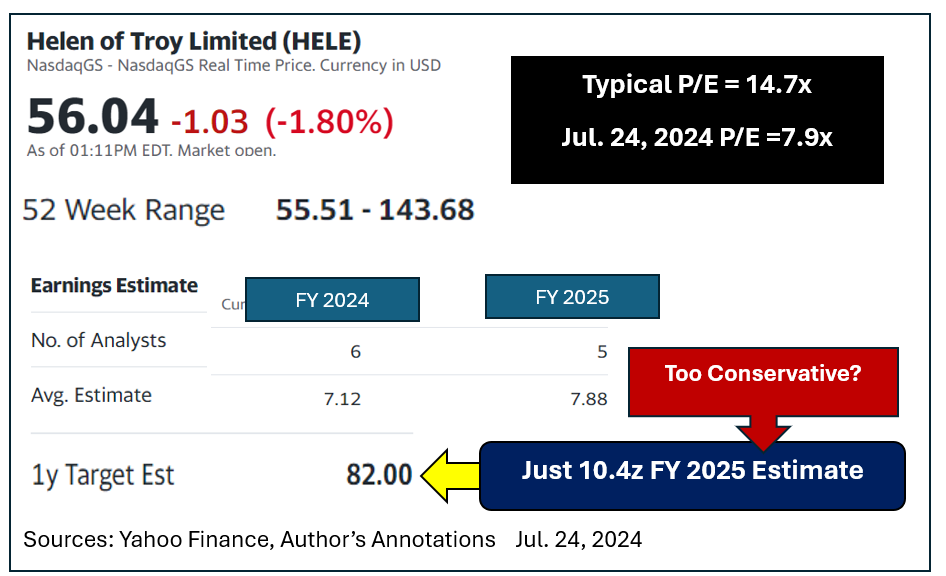

After a disappointing fiscal first-quarter report (ended May 31, 2024) the shares cratered. As of July 24, 2024 the stock was changing hands below $56. Reduced EPS guidance now sits at $7.12 for the year ending Feb. 28, 2025, then rebounding to around $7.88 in FY 2025.

That major price plunge has created a buying opportunity.

Since 2015 the most important business metrics have grown (cumulatively) from $13.9% to 99.8% as detailed below. The stock price, however, is now almost 38% cheaper than where it was exactly nine years earlier.

That left HELE shares at its lowest P/E multiple in more than a full decade.

What Is Helen of Troy Worth?

Since 2015 the stock fetched an average 14.8 times earnings. At south of 8 times what are expected to be trough earnings this year upside potential appears extremely high.

A reversion towards the mean valuation of 14 times FY 2025’s already reduce estimate would justify an 18-month target price of $110.30. That implies a decent chance at seeing about 97% upside by February of 2026.

I am not alone in sensing this opportunity.

Yahoo Finance carries a year-ahead goal price of $82 for HELE. Reaching that target would deliver a 12-month return north of 46%.

Better still, Yahoo Finance’s price target only assumes a 10.4x multiple on their own FY 2025 estimate. That is compared with a 9-year average P/E of 14.7x.

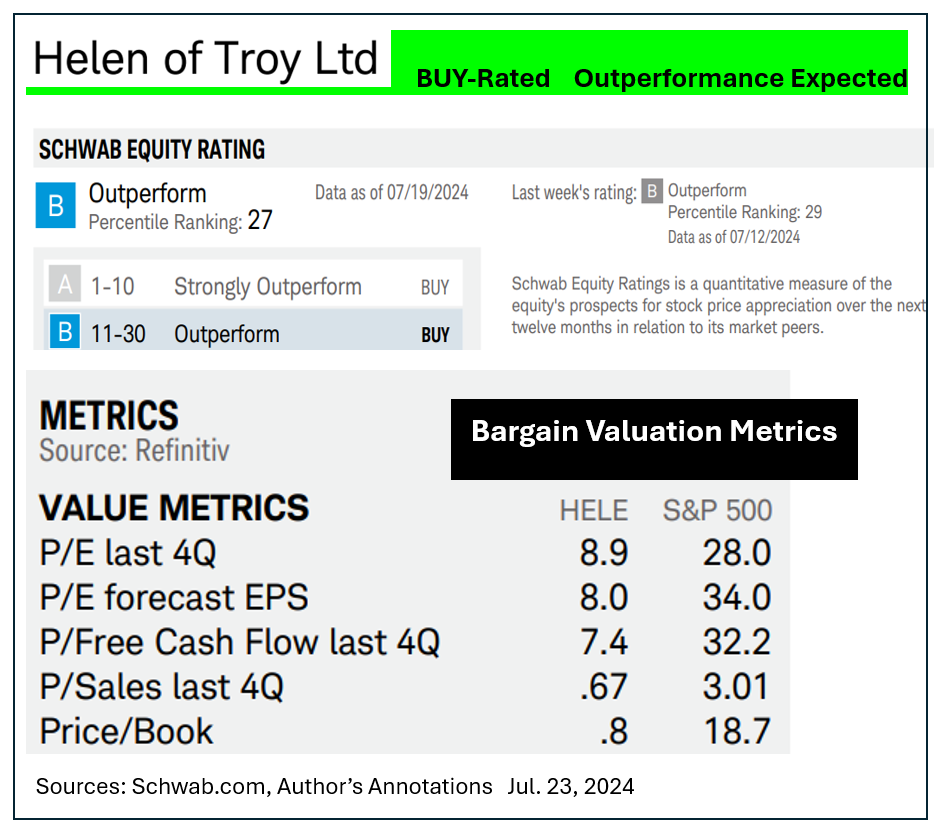

Schwab research labels HELE an ‘outperformer” over the coming year.

All major metrics show how cheaply it is now offered compared with the broader market.

Quantitatively-based FAST graphs calls about 13 times earnings normal for HELE. Based on that, more conservative P/E, the shares could easily reach almost $105 by February of 2026.

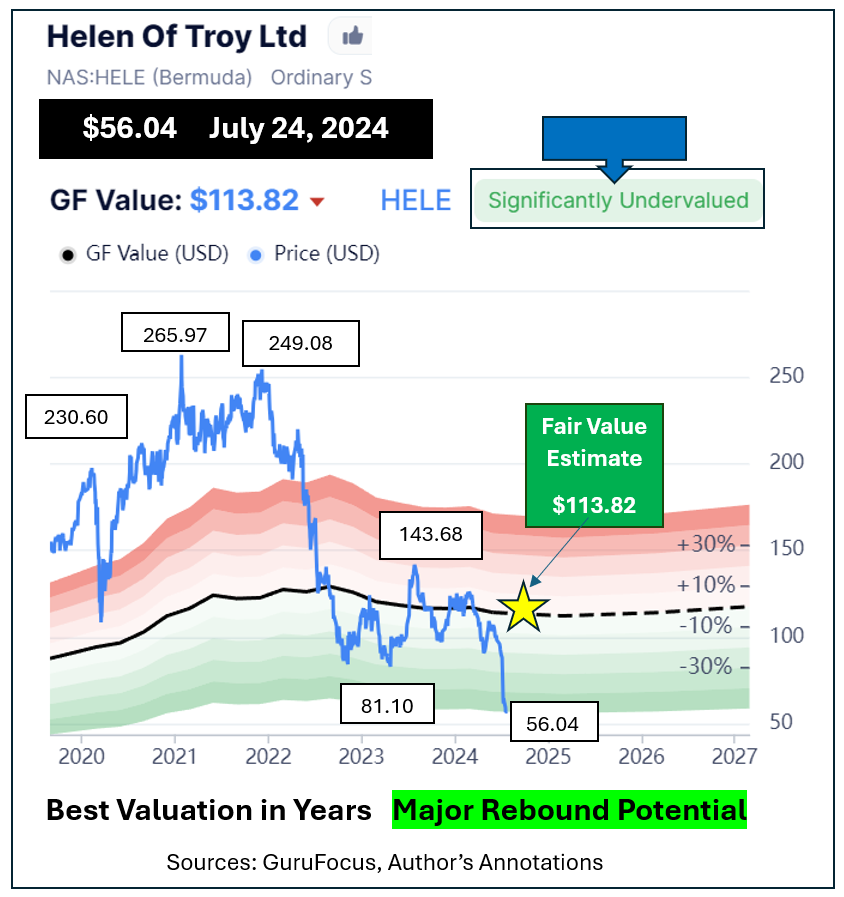

GuruFocus research aggressively calls present-day fair value for HELE as $113.82. The goal is not crazy. The stock traded at more than double that price during segments of each of the three years stretching from 2020 through 2022.

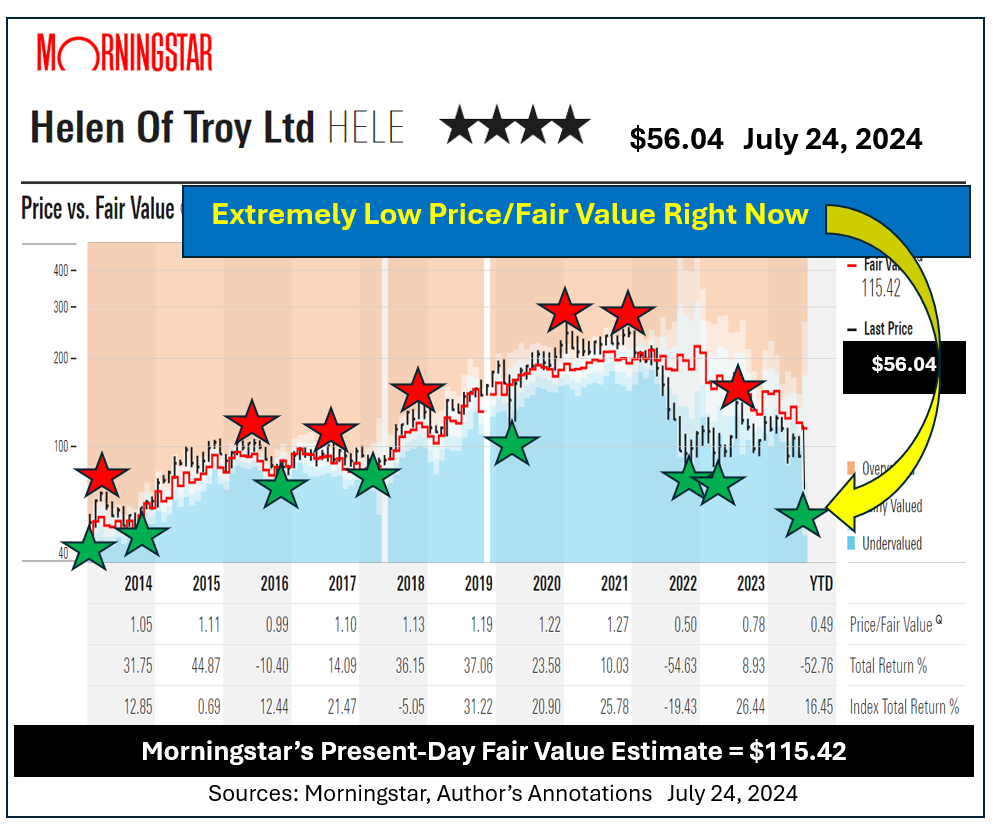

Morningstar research labels HELE a 4-star (out of five) buy today. Like GuruFocus it sees present-day fair value as north of $110.

Morningstar’s unique price-to-fair value chart implies today’s quote represents the lowest price to fair value relationship in more than a full decade.

Also notable: There were six distinct large selloffs followed by even better percentage rallies in HELE since 2014. There is no reason to think the current plunge will not be followed by a similar surge.

Barring a significant unexpected event, Helen of Troy offers a low-valuation entry point with modest downside yet large upside potential.

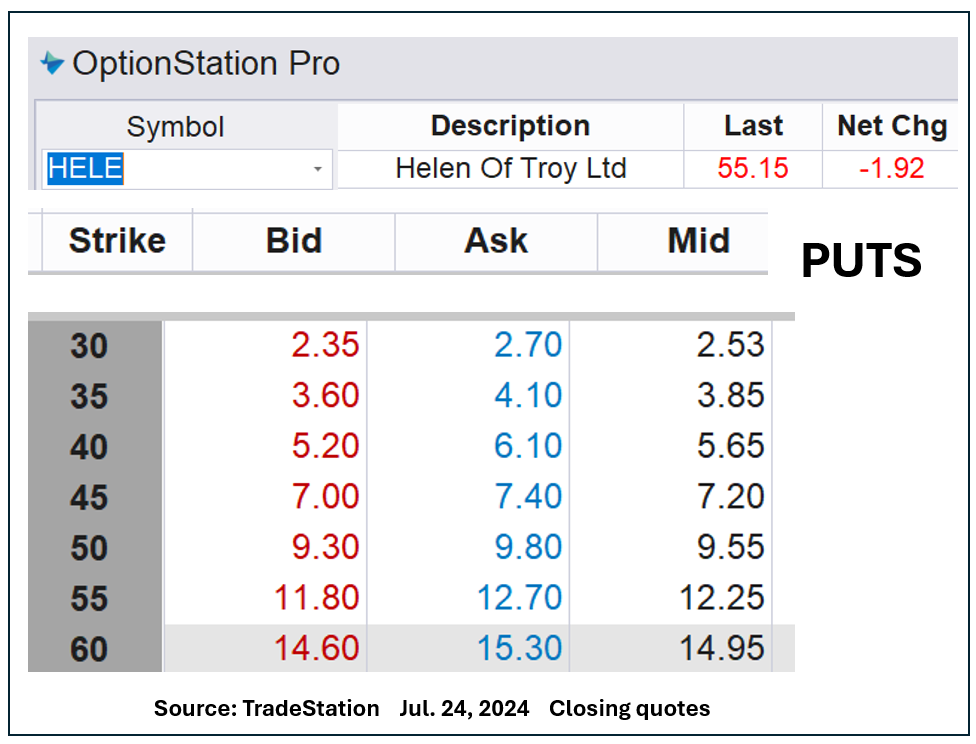

Options are available extending out as far as Jan. 16, 2026. Premiums are extremely juicy for anyone willing to sell naked puts while the near-term mood is unusually bleak.

I was a seller of Jan. 2026 expiration date LEAP puts at strikes of $45, $50 and $55.

Actual pricing on the puts, with HELE closing at $55.15, is shown below.

Worst-case, forced purchase prices on the $30 strike would be about $27.50. On the $35s it would be $31.10, the forties would drop break-even to $34.35 or so. Shorting $45 puts at $7.20 takes the “if put” price to just $38.60. Getting paid $9.50 per share to buy at $50 makes your break-even on the short-put trade only $37.60 per share.

For reference, HELE has not changed hands for under $47.40 since 2013. EPS that year came in at $3.54, rather than the $7.12 estimate for the current fiscal year.

Buy some HELE shares, short some naked puts out to Jan. 2026, or consider doing both.

More Paul Price:

- Short-Term Variations Make Us Crazy. They Also Create Opportunities.

- Investing Is a Marathon. Trading Is a Sprint.

- Fun Facts That Help Investors Make Money

At the time of publictaion, Price was long HELE shares, short HELE puts as described.