Nvidia Denies, Trading NVDA, Another Lockheed Parabolic Run? Jolting JOLTS

Many are caught now between feeling bullish ahead of a shift into easier monetary policy and not wanting to be overly exposed going into a period of much slower economic activity.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Late Wednesday afternoon, Nvidia NVDA denied that the firm ever even received a subpoena from the U.S. Department of Justice in regard to an antitrust investigation. Reports had circulated on Tuesday that the high-end chip designer had been subpoenaed, and that the stock of Nvidia had taken a 9.53% beating that day, leading the broader U.S. equity market lower. There were no specifics given in the reports seen on Tuesday, but the company is known to have a rough 80% share of the data center AI-focused market.

A Nvidia spokesperson told CNBC: "We have inquired with the US Department of Justice and have not been subpoenaed. Nonetheless, we are happy to answer any questions regulators may have about our business." Elsewhere, a company spokesperson also told Seeking Alpha: "Nvidia wins on merit. as reflected in our benchmark results and value to customers, and customers can choose whatever solution is best for them."

Imagine reading or hearing in the news that your company has been subpoenaed by the DOJ and seeing your stock surrendering almost 10%, and having not received said subpoena? You end up having to check with the agency just to make sure that you're not missing something. Just incredible.

I remain long a reduced (from the peak) core position. As for the trade I put on overnight Wednesday into Thursday, I am out of those at an even $109, having entered at $105.84.

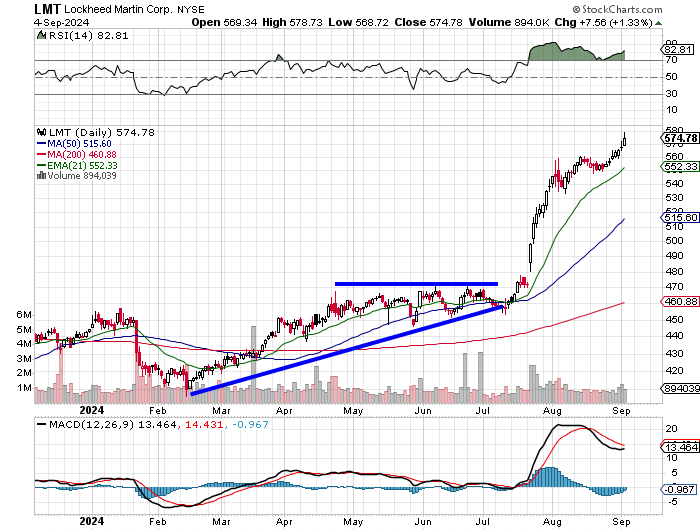

As mentioned in my piece last week, the pivot has moved from the left side of the cup to the right side and now stands at $130. The new much deeper size of the handle does not change that. My target for now, remains $156. According to TipRanks, the average target among top-rated analysts for this stock is $150.66.

However, the daily Moving Average Convergence Divergence (MACD) is no longer postured bullishly, and the 21-day exponential moving average (EMA) has crossed back underneath the 50-day simple moving average (SMA). These are technical negatives that do increase the likelihood that the stock could retest either the low of August 5 or the 200-day SMA.

I think I would add should such a test arise, but I would have the stock on a short leash in that case, especially if a new bout of weakness arose in response to something legal.

Marketplace

It felt as if traders took Wednesday off. In one respect, that's a negative as there was no rebound coming off of Tuesday's selloff. On the other hand, where's the catalyst that would drive traders and investors to put risk back on ahead of this Friday's August employment survey results after having just reduced exposure? Something would have to be more convincing than a weak JOLTs report for July.

Many are caught right now between feeling bullish ahead of a shift into an easier regime for monetary policy and not wanting to be overly exposed going into a period of much slower economic activity.

On Wednesday, the S&P 500 gave up just 0.16%, as the Nasdaq Composite slid 0.3%. Among other key indexes, the Dow Transports led to the upside at +0.39%, followed by the Philadelphia Semiconductors at +0.25%. The KBW Banks lagged at -0.61%.

Six of the 11 S&P sector SPDR ETFs shaded into the green on Wednesday, again led by defensives as the Utilities XLU gained 0.85% and the Staples XLP rose 0.47%. Energy XLE led the losers, down 1.38%, with no other fund among the 11 losing even half of one percent.

Breadth for the session really tells us nothing at all. Winners beat losers by a smidge at the NYSE, while losers beat winners by roughly 5 to 4 at the Nasdaq.

Advancing volume reversed from the winners/losers tally, however, taking just a 44.7% share of composite NYSE-listed activity and a 51.1% share of composite Nasdaq-listed trading volume. Aggregate trading volume was down substantially on a day-over-day basis for listings of both exchanges as well as across the membership of the S&P 500.

Jolting JOLTS

It's dated news, but it is employment related. For July, JOLTS job openings fell to 7.673 million, for a downwardly revised 7.91 million in June, according to the Bureau of Labor Statistics. This is now the fewest job openings seen in this report since early 2021.

The number of job openings per unemployed worker has now dropped to a ratio of 1.1 to 1 after having soared to as much as 2 to 1 in 2022. Layoffs in July increased to 1.76 million, which makes July the worst month in that regard since March 2023.

Abbreviated Beige Book

The Fed's Beige Book was released on Wednesday afternoon. The economy, according to this anecdotal account that had been collected across all 12 districts by the Cleveland Fed, is not falling apart rapidly, nor is it rocking. I guess "stagnant" would be the best word for now.

On Labor Markets..."Employment levels were generally flat to up slightly in recent weeks. Five Districts saw slight or modest increases in overall headcounts, but a few Districts reported that firms reduced shifts and hours, left advertised positions unfilled, or reduced headcounts through attrition - though accounts of layoffs remained rare."

On Inflation... "On balance, prices increased modestly in the most recent reporting period. However, three Districts reported only slight increases in selling prices. Non-Labor input cost increases were largely described as modest to moderate and as generally easing, though one District described input cost as ticking up."

Boston... "Economic activity increased modestly."

New York... "On balance, regional economic activity remained flat."

Philadelphia... "Business activity declined slightly."

Cleveland... "District business activity declined slightly in recent weeks."

Richmond... "The regional economy contracted slightly this cycle."

Atlanta... "Economic activity in the Sixth District declined slightly."

Chicago... "Economic activity increased slightly."

St. Louis... "Economic activity has remained unchanged."

Minneapolis... "District economic activity fell slightly."

Kansas City... "Economic activity in the Tenth District remained stable."

Dallas... "The Eleventh District economy expanded modestly over the reporting period."

San Francisco... "Economic activity remained stable."

Another Revision

In response to the BEA's release of the national trade balance for July and a strong report for July Factory Orders from the Census Bureau, the Atlanta Fed revised its real-time Q3 GDPNow model up to growth of 2.1% (q/q, SAAR) from 2.0%. The input for gross private domestic investment was tweaked higher, offset partially by a tweak to the downside for personal consumption expenditures.

Atlanta will revise the model again on Monday in response to a scheduled revision to July Wholesale Inventories.

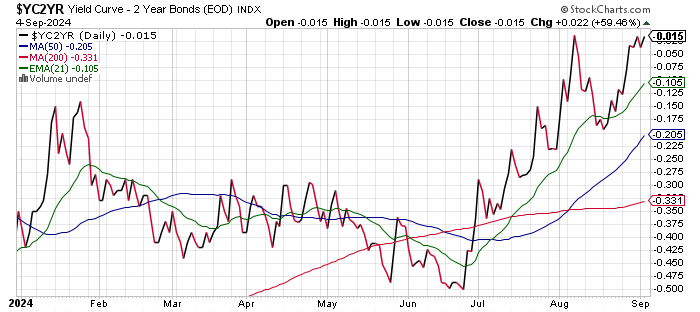

Untwisted?

Not exactly. While in response to the weak JOLTs report and the sort-of-weak Beige Book, the spread between the yields of the U.S. 10-Year and 2-Year Notes actually un-inverted or "normalized" briefly on Wednesday. That got some folks in the financial media with only a shallow understanding of debt markets and their relationship to economic performance and projecting, a little excited.

That spread went out looking like this:

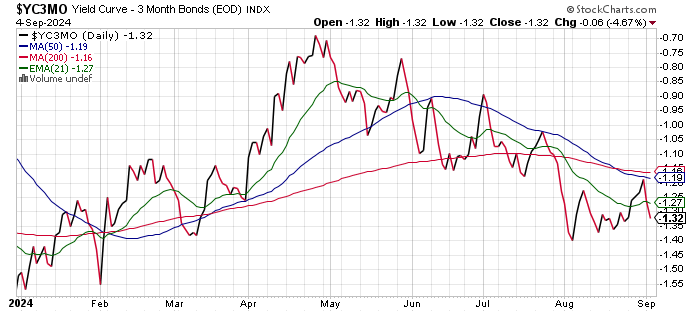

But the far more important spread between the 10-Year Note and 3-Month T-Bill is still not cooperating, and in fact is moving in the other direction of late:

Prepare for Ludicrous Speed

You kids watching long-time Sarge name Lockheed Martin LMT? The stock, which is also position in TheStreet Pro Portfolio, broke out of an ascending triangle pattern back in mid-July, consolidated a bit and now appears to be preparing for perhaps another parabolic run.

Despite a persistently technically overbought Relative Strength Index (RSI) reading that is nearing its own two-month mark, the stock appears to be gearing up for maybe another run.

The daily Moving Average Convergence Divergence (MACD), which has started to look bearish, now has a 12-day exponential moving average (EMA) curling upward back towards its 26-day EMA as the histogram for the 9-day EMA that had gone negative, appears to be headed back for positive territory.

My price target remains $594. The average target for top-rated analysts according to TipRanks is $579.73.

Economics (All Times Eastern)

08:15 - ADP Employment Report (Dec): Expecting 139K, Last 122K.

08:30 - Initial Jobless Claims (Weekly): Expecting 229K, Last 231K.

08:30 - Continuing Claims (Weekly): Last 1.868M.

08:30 - Non-Farm Productivity (Q2-rev): Flashed 2.3% q/q SAAR.

08:30 - Unit Labor Costs (FQ2-rev): Flashed 0.9% q/q SAAR.

09:45 - S&P Global Services PMI (Aug-F): Flashed 55.2.

10:00 - ISM Non-Manufacturing Index (Aug): Expecting 51.0, Last 51.4.

10:30 - Natural Gas Inventories (Weekly): Last +35B cf.

11:00 - Oil Inventories (Weekly): Last -846K.

11:00 - Gasoline Stocks (Weekly): Last -2.203M.

The Fed (All Times Eastern)

No public appearances scheduled.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: SAIC (1.25)

After the Close: AVGO (1.20), DOCU (0.80), PATH (0.03)

At the time of publication, Guilfoyle was long NVDA, LMT and XLU.