The Meta Effect, Semis Surge, Wall Street Says, ‘What War?’

Markets brush off fighting with Iran as Meta talks about making its own AI chips; South Korea’s SK Hynix lists on Nasdaq; I give a chart checkup on the market.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

What a day! Sort of. There is no doubt that domestic financial markets showed incredible resiliency on Thursday and that this came on top of a midday rebound for U.S. equities on Wednesday. War? The markets don’t seem to care, at least not right now. Does Wall Street continue to see a quicker-than-reality resolution to the shooting in and around the Strait of Hormuz and the higher energy prices that conflict is causing?

It would appear so. Bloomberg News cited an American official who said that talks between the U.S. and Iran regarding a long-term peace deal were ongoing. Markets were strong on Thursday. The S&P 500 rallied for a gain of 0.81%, while the Nasdaq Composite added 1.3%. Even more impressively, the tech-centric Nasdaq 100 jumped 1.62% for the day. In addition, the Dow Transports ran 2.07% and all of the small to midcap indices gained between 1.21% and 1.24%. All because a U.S. official was optimistic on peace talks? Not exactly.

Cause

On Thursday morning, Reuters reported that Meta Platforms (META) planned to begin manufacturing its in-house AI chip this September. This move is part of a broader effort to expand computing capacity and use its own custom hardware to enhance AI-driven capabilities across the Facebook and Instagram platforms. Broadcom (AVGO) is set to help design this chip and Taiwan Semiconductor (TSM) will manufacture it. TSM is currently the largest position in the Sarge-folio. Meta will also be sourcing RAM from Samsung, storage from SanDisk (SNDK), and fiber-optic equipment from Sumitomo Electric. SanDisk, after sales earlier this week, is still the third largest holding, in dollar terms, in the Sarge-folio.

The new chip is meant to supplement and ease the expense associated with the large quantities of GPUs that Meta (and other hyperscalers) must purchase from designers such as Nvidia (NVDA) and Advanced Micro Devices (AMD). This move by Meta runs parallel to already underway in-house custom chip design programs at Alphabet (GOOGL), Amazon (AMZN), and Microsoft (MSFT). As much as these efforts illuminate the search for those firms engaged in the huge AI-focused capital spending arms race, I think it also reflects just how strong demand is for these kinds of chips. The broad need for computing power continues, in my humble opinion, to be insatiable.

Effect

That news created strength across the tech space and especially across the semis on Thursday, which may seem counter-intuitive to first-level thinkers. The Technology sector SPDR ETF (XLK) popped for a gain of 2.18% for the day. This strength, at least on Thursday, was, of course, driven by the semis. While the Dow Jones U.S. Software index “only” gained 0.89% for the day, the Philadelphia Semiconductor Index added 3.06%. Arm Holdings (ARM), SanDisk and AMD led that group.

Readers will also see, eslewhere, that the S&P Financial sector SPDR ETF (XLF), while it may have put in a double top (bearish) earlier this week, developed a “golden cross” on Thursday, as its 50-day simple moving average overtook its 200-day SMA:

This is a bullish signal. In addition, for this fund, both Relative Strength and its daily moving average convergence divergence are exhibiting bullish-looking characteristics.

Then There’s SK Hynix

The American depositary receipts of South Korean memory-chip giant SK Hynix (SKHY) will list and trade at the Nasdaq starting Friday. The deal raised a rough $26.5 billion at a price of $149 per ADR. SK Hynix is South Korea’s second largest company, behind Samsung and boasts a $1 trillion market cap. The company operates fabs in both South Korea and China and is currently building an advanced chip-packaging facility in West Lafayette, Indiana.

That construction will be supported by $458 million in funding from the U.S. Chips and Science Act. SK Hynix, Samsung and U.S.-based Micron Technology (MU) are the planet’s largest producers of high-bandwidth memory. Note that MU is the one memory/storage basket name where the Sarge-folio has not changed its weighting as that trade faded over the past two weeks. MU is currently number 8 in our book.

High-bandwidth memory involves stacking multiple dynamic random-access memory (or RAM) dies vertically on an interposer creating very wide interfaces, which is essential for the design of powerful AI chips. I am sure that at least part of the reason that the memory/storage basket stumbled of late was due to managers having to create room for the addition of SK Hynix to that basket without having to increase the overall weighting (exposure) of that trade versus the rest of their books.

Marketplace

As mentioned above, the action was strong on Thursday. Seven of the 11 S&P sector ETFs closed out the regular session in the green as bond traders also pushed yields lower across the curve. You already know that Tech led the way. Discretionaries (XLY) and the financials (XLF) followed. The staples (XLP) rode out the session in the caboose. Growth and cyclical sectors easily outpaced the defensives on Thursday.

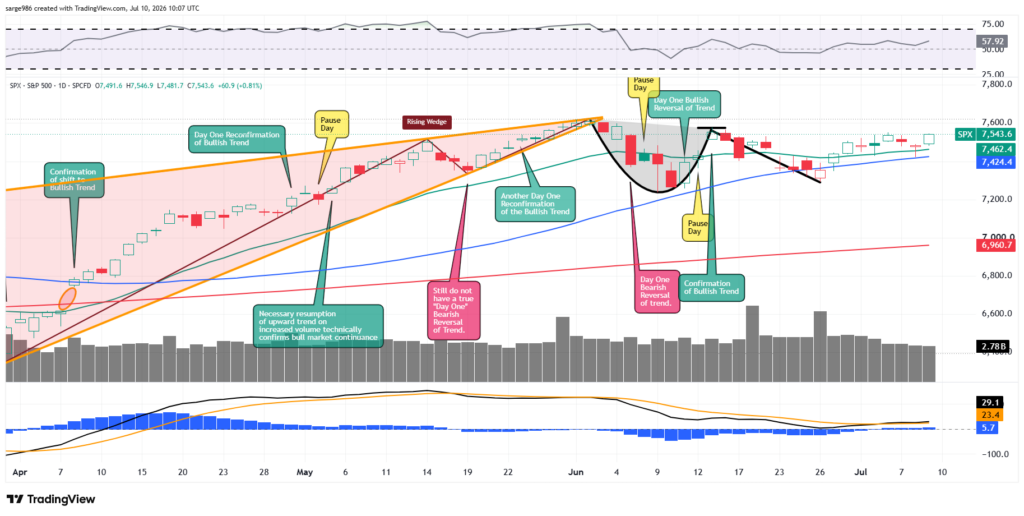

Winners beat losers at the NYSE, on Thursday, by a rough five-to-three margin and at the Nasdaq by almost precisely two to one. Advancing volume took a 62.3% share of composite NYSE-listed trade and a close to impressive 67.8% share of composite Nasdaq-listed activity. Those looking for a declaration of a bullish “Day One” reversal or a reconfirmation of the bullish trend will have to wait as the trading volume was light for the day. On a day-over-day basis, activity contracted across NYSE-listings, across Nasdaq-listings and across the membership of the S&P 500.

However, check out this:

Both the Nasdaq Composite and Nasdaq 100 managed to take back their 50-day SMAs on Thursday. Holding this line throughout the Friday session going into the weekend, could force portfolio managers to increase long side exposure to tech stocks and even smaller caps in the short term.

Interestingly, throughout this period, the S&P 500 has not lost its 50-day simple moving average and has been able to maintain support at its 21-day exponential moving average.

The implication? The swing crowd and the pros are still on the same side of the football.

Economics (All Times Eastern)

1:00 p.m. – Baker Hughes Total Rig Count (Weekly): Last 580.

1:00 – Baker Hughes Oil Rig Count (Weekly): Last 445.

The Fed (All Times Eastern)

No public appearances scheduled.

Today’s Earnings Highlights (Consensus EPS Expectations)

Before the Open: DAL (1.48)

At the time of publication, Guilfoyle was long TSM, SNDK, NVDA, AMD, MU equity.