If You Still Own Bonds… What Are You Thinking?

Fixed income has been a wealth-destroying proposition over the past decade or so.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

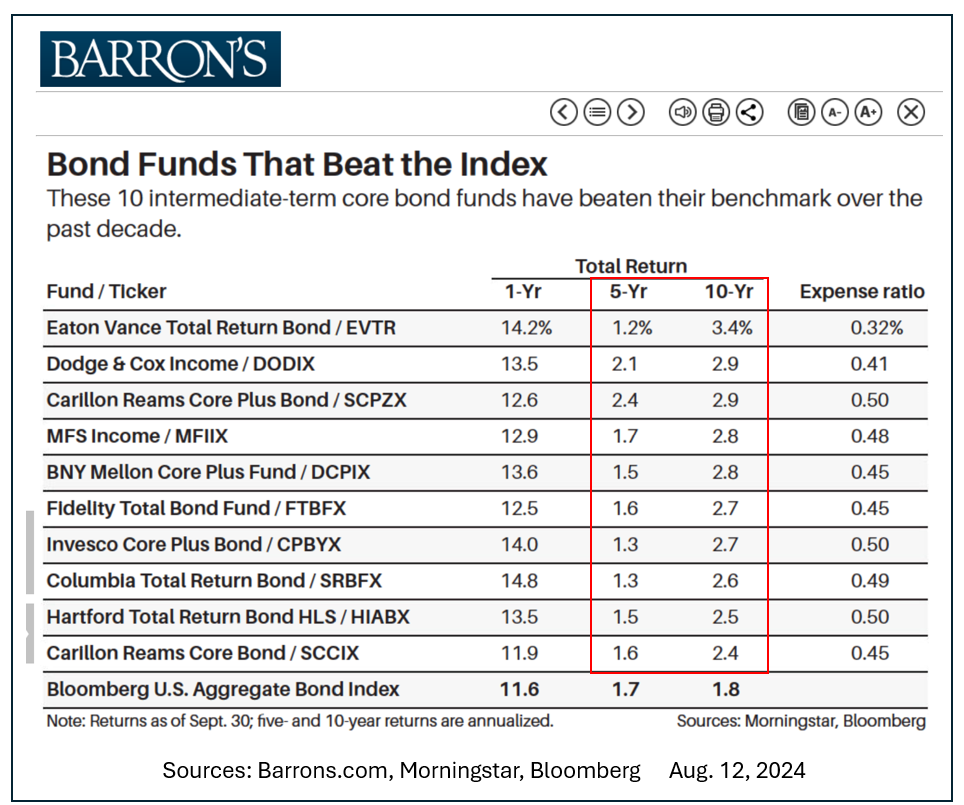

This week’s Barron’s featured an article showing bond funds that beat their benchmark index over one, five and 10-year periods.

The past 12 months looked good at first glance due to the Fed’s recent start to reversing some of the damage done from their extreme tightening cycle. These index-beating funds, though, showed putrid five- and 10-year total returns through Sep. 30, 2024.

None of these “best funds” came anywhere close to preserving buying power after inflation and taxes.

The funds’ expense ratios alone stole a large chunk of investors’ already anemic long-term results.

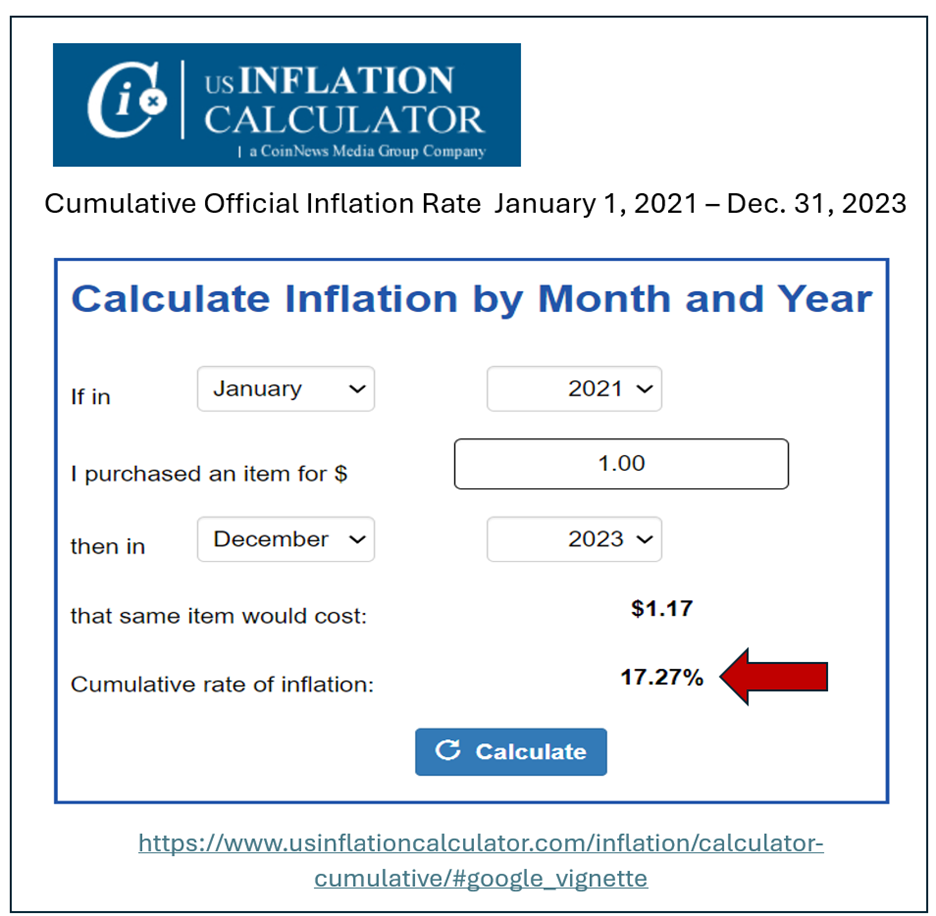

From January of 2021 just through the end of 2023, officially reported cumulative inflation was 17.27%. Add in another 3% or so for 2024 year-to-date and the cumulative loss of purchasing power is well above 20%.

That goes a long way towards explaining why so many people are unhappy, or worse, with today’s economic situation. The rate of increase has slowed from the 2022 peak above 9%, but prices continue to go up steadily while compounding on the sharp increase during 2022.

Owning fixed income has clearly been a wealth-destroying proposition over the past decade or so.

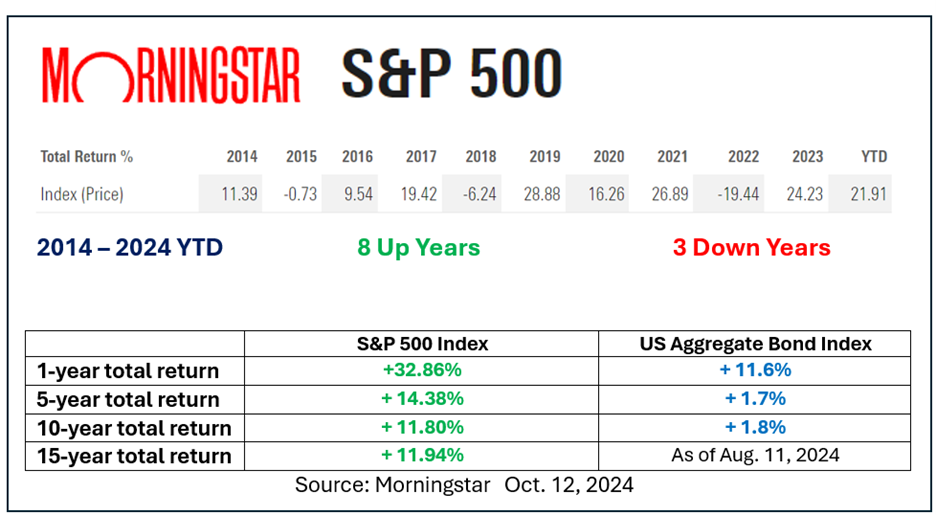

Holding equities, though, has been a much better choice. From 2014 though this year (so far) there were eight winning years versus just three losers. One of those, 2022, also saw losses across the board in all major bond categories.

The aggregate bond index performed reasonably well from September 30, 2023 through September of 2024, gaining 11.6%. That paled considerately, though, compared with the current 12-month gain of 32.86% of the S&P 500.

Five- and 10-year trailing total return comparisons were even more striking in favor of owning equities.

If you are thinking that 10–15 years is not a long enough period to be conclusive… think again.

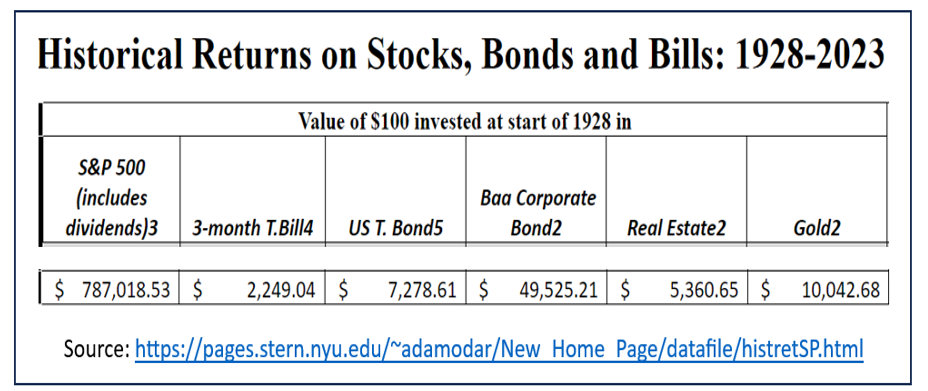

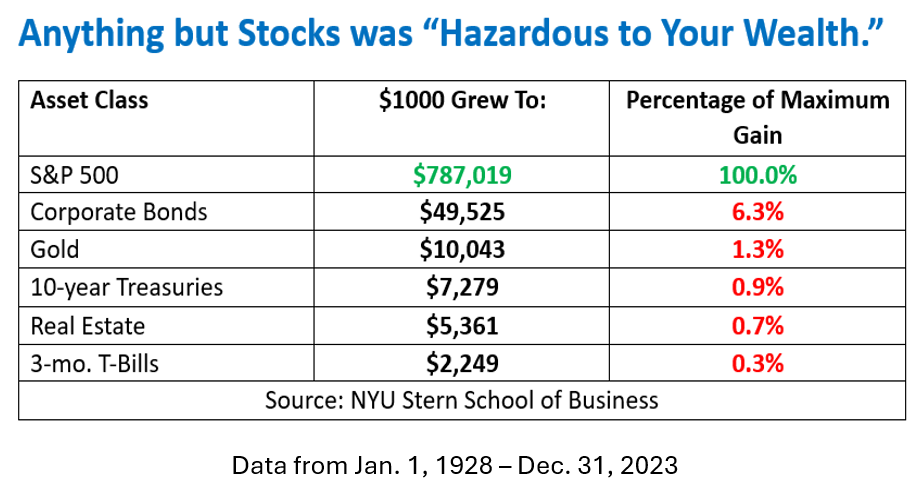

NYU’s school of business is nice enough to tabulate results on various asset classes at the end of each calendar year.

The graphic below shows the cumulative compounded returns on an initial $100 investment from the start of 1928 through Dec. 31, 2023.

This proves that the longer the period, the more incredible the case becomes for owning, and sticking with, equities above virtually anything else.

Corporate bonds earned only 6.3% as much as the S&P 500 index. Precious metals, 10-year duration government bonds, real estate and cash equivalents fared much worse.

Classic financial planners almost universally ignore these facts when recommending “stock, bond and cash” asset allocations to their clients.

Why is that? They know that people tend to react badly to the inevitable sharp selloffs which stocks occasionally suffer. That can cause them to pull their accounts costing the advisors money.

The longer the period, the more incredible the case becomes for owning, and sticking with, equities above virtually anything else.

Keeping lower-volatility bonds and cash as ballast against negative equity results lessens the chances of seeing customers abandon them.

That makes sense for financial planners even though it works against clients’ long-term interests relating to wealth creation over time. The Barron’s article on bond funds never mentions that fixed income almost always fails to perform when looking at increasing true purchasing power over people’s lifetimes.

Actual market history says stocks are your best bet to getting rich other than being smart/lucky enough to start a wildly successful company like Elon Musk, Larry Ellison or Jeff Bezos did.

Those men, now among the wealthiest on Earth, also defied classic financial advice by staking their futures on single-company investments rather than widely diversifying their holdings.

See my earlier article titled “Who Wants to Be a Millionaire - 2023 Edition" for proof that anyone can reach that milestone using a Roth IRA and sticking with 100% in equities.

More From Paul Price

- What Traits Make a Great Stock Investor?

- This Is the Single Most Important Factor in How Wealthy You’ll Be at Retirement

- Would You Buy an Investment That Guarantees No Profit for at Least 10 Years?

At the time of publication, Price had no positions in any index funds or ETFs and no bond or bond fund holdings. His Roth and Traditional IRAs are always 100% invested in equities. Both are now well into seven figure values.