I Bought a Truly Hated Stock This Week. Here's Why

Having the temperament to buy what others are currently shunning takes a mindset that few people possess.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Few stocks repel media analysts like those which have recently cratered.

Nobody wants to admit they owned such a doggy name. Fewer still are willing to stick their necks out recommending a stock with such a terrible chart.

History says, though, that buying solid companies when they get extraordinarily cheap is typically a great way to make money.

Pessimistic expectations set very low bars to hurdle. That sets the stage for positive earnings surprises going forward. Owning shares of a company which just finished a bad year allows for easy year-over-year comps as new more profitable quarters begin to be compared with those trough earnings years.

Drugstore operator Walgreens Boots Alliance WBA is in the closing stages of a poor fiscal year 2024 (ends Aug. 31, 2024). Estimated earnings per share run from $3.20 to $3.23 down from $3.98 (adjusted) in FY 2023.

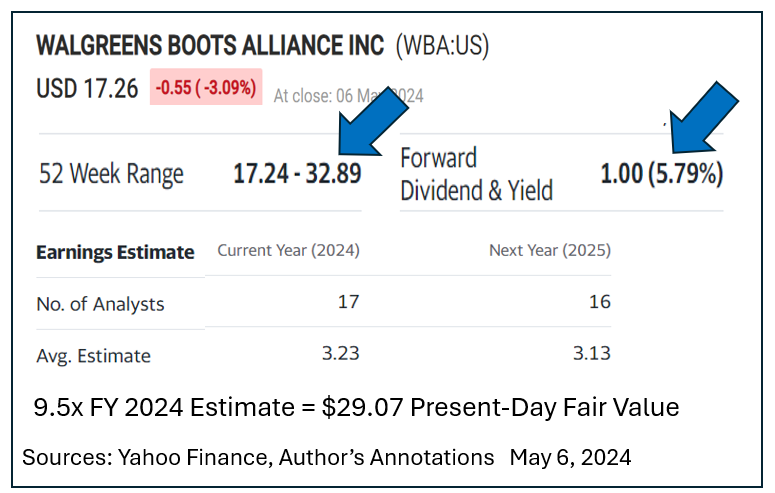

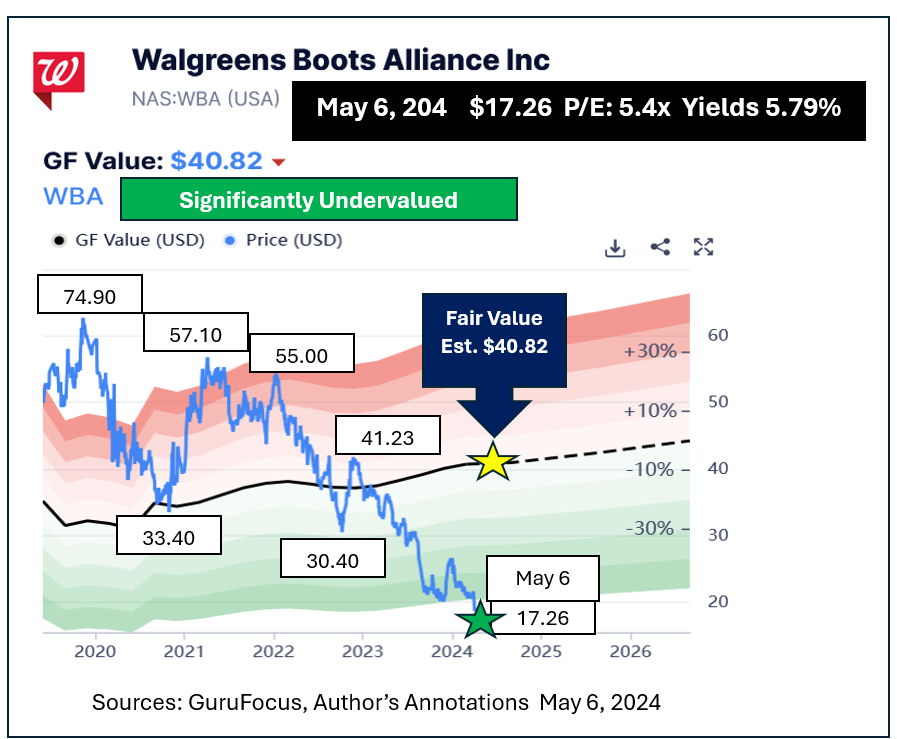

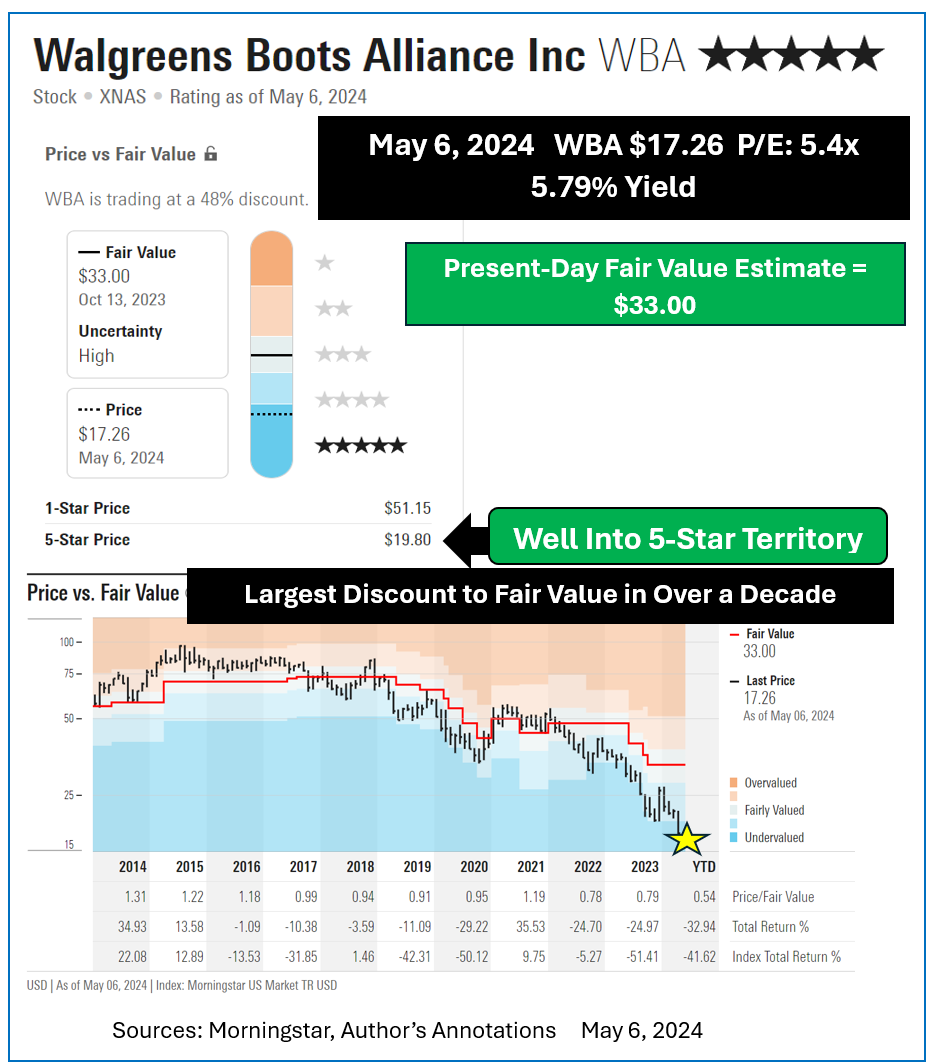

The stock has performed dreadfully. Its shares dipped from a 52-week peak of $32.87 to a 28-year low of $17.24 on Monday, May 6, 2024.

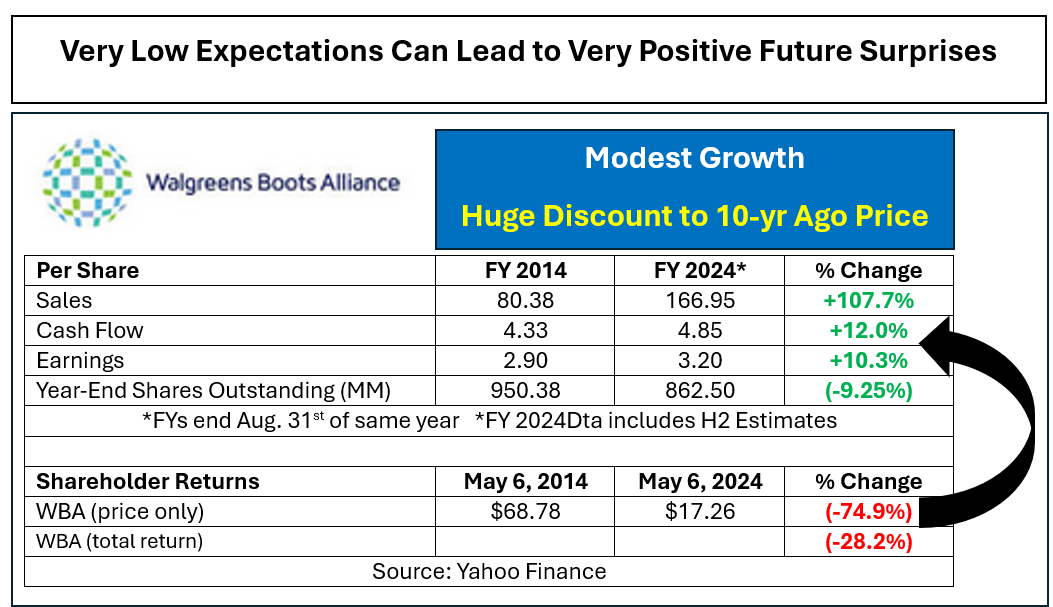

Over the most recent decade per-share sales more than doubled. Cash flow and EPS edged higher by 12% and 10.3%, respectively. Shares outstanding declined by about 9.25%. On balance WBA is now more valuable than it was 10 years earlier.

Instead, WBA now sells for an almost 75% discount to what it fetched on May 6, 2014. That discrepancy between value and price makes it likely that buyers of WBA today will have great gains for buying and giving WBA time to regress towards a more fitting valuation.

The stock’s 5.79% dividend, at an already reduced rate of 25 cents quarterly, provides a better income stream than the best bank CDs available. Those CDs offer no possibility of capital gains while WBA could easily be up 50% or more in relatively short order.

What Is WBA Worth?

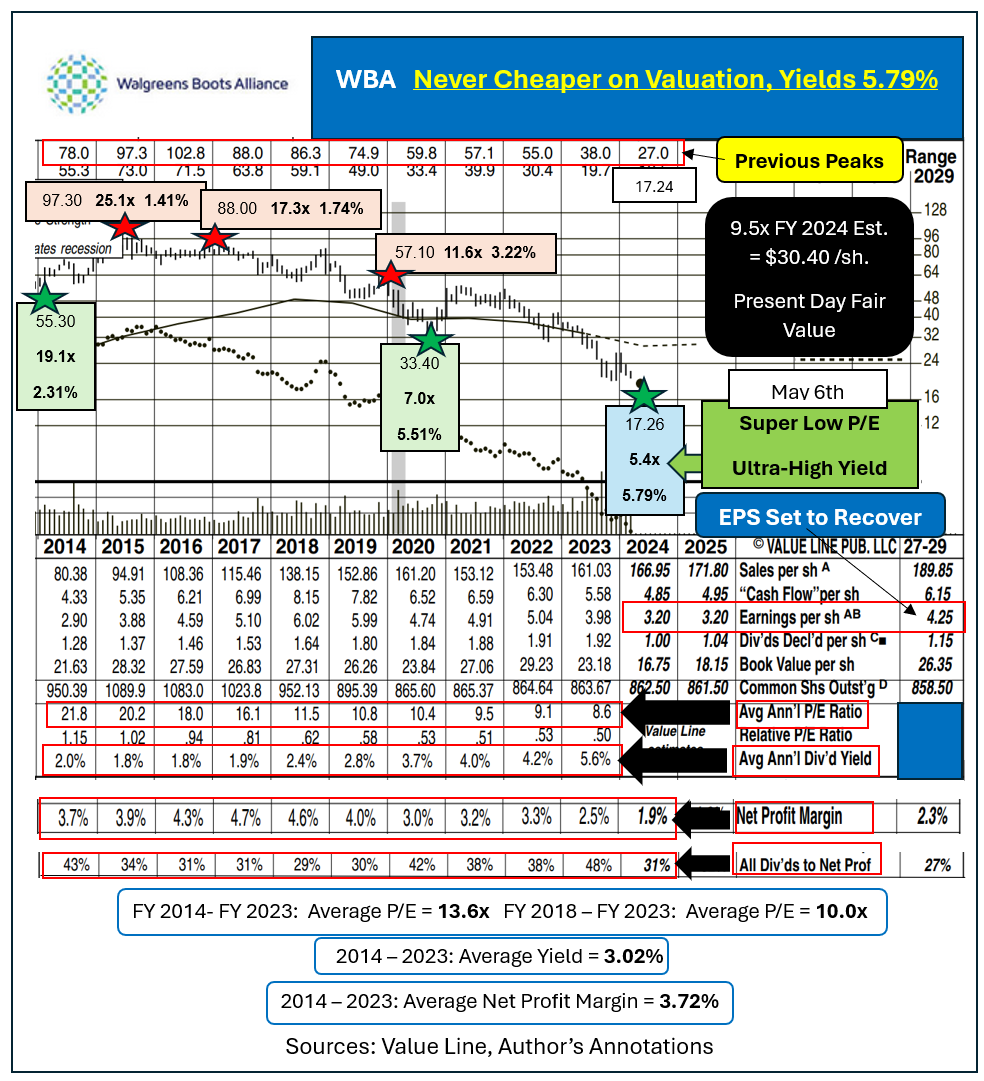

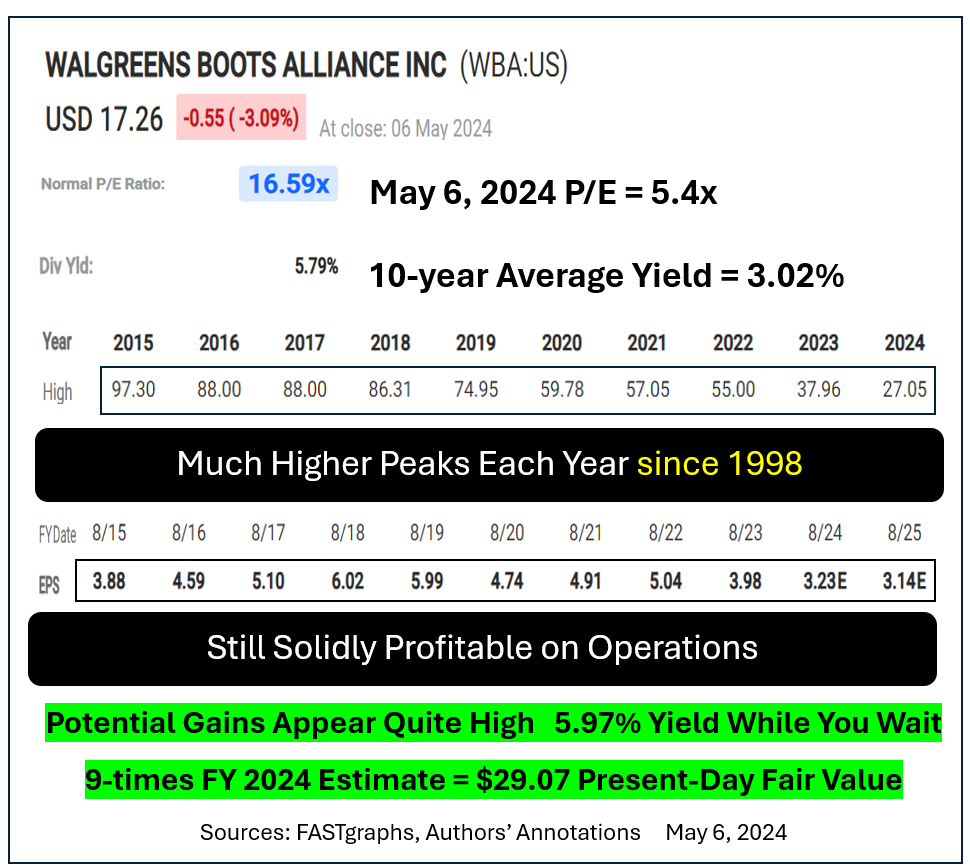

From 2014 through 2023 WBA's average P/E ran 13.6 times, accompanied by around 3.02% in current yield. Over the most recent six years WBA’s average P/E was a more mundane 10 times.

Since FY 2024 Walgreens average net profit margin tallied 3.72%. In the current year that is down to about 1.9%. That is the lowest ever for this company. Management is taking steps to fix that. The ultra-low profit margin is much more likely to regress towards the mean than to remain at a formerly unimaginable low level.

Assume a rebound to only 2.5% on expected FY 2025 sales per share of $171.80 and EPS could jump up to about $4.30 in the year beginning Sep. 1, 2024. History says that is not far-fetched. WBA earned between $4.59 and $6.02 during each of the seven years stretching from FY 2016 through FY 2022 on considerably lower sales per share than today’s.

If those EPS materialize, a P/E of even nine times would send WBA back up to $38.70. That would deliver a nice 124.2% gain plus dividends. That return will still look great if it takes a full two years to achieve.

My personal present-day fair value estimate for WBA is $30.40, 9.5 times this year’s EPS. Reaching that goal translates into an 81.9% total return if it takes 12 months to get there. Reverse engineering the already reduced $1 per share annual dividend rate to a more typical 3.02% calculates into a $33.11 target price.

Not everyone agrees on what fair value should be.

Yahoo Finance’s EPS estimate suggests a $29.07 current value for WBA. Hitting that by next spring would deliver greater than 74% in total return.

FAST Graphs also likes WBA. Its normalized P/E for them calculated to 16.6x. Apply a nine multiple to their FY 2024 estimate of $3.23 and you produce an (identical to Yahoo Finance’s) implied fair value of $29.07.

GuruFocus research views WBA as being in “significantly undervalued” status. Its present-day fair value seems somewhat optimistic at $40.82.

Longer-term, though, that north of $40 goal price does not appear unreasonable based on WBA’s previous trading history.

Independent research from Morningstar also loves WBA. It merits their highest, 5-star, buy rating since falling below $19.80.

The stock is now at the largest discount to fair value since 2008-09.

Morningstar’s present-day fair value estimate for Walgreens now sits at $33.

More From Paul Price:

Value Investors love buying mis-priced stocks when upside appears large, and risk seems low. Having the temperament to buy what others are currently shunning takes a mindset that few people possess.

You only get incredible values on decent companies when most traders see no good reason to buy just yet.

I added a couple of thousand shares of WBA to my personal holdings on Monday, May 6.

At the time of publication, Price was long WBA shares, short WBA options.