Coat Tailing Buffett’s Latest Big Buy? Not a Good Idea

Here's why it is likely too late to copy Berkshire Hathaway’s move into the insurer — unless you are betting on one thing.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

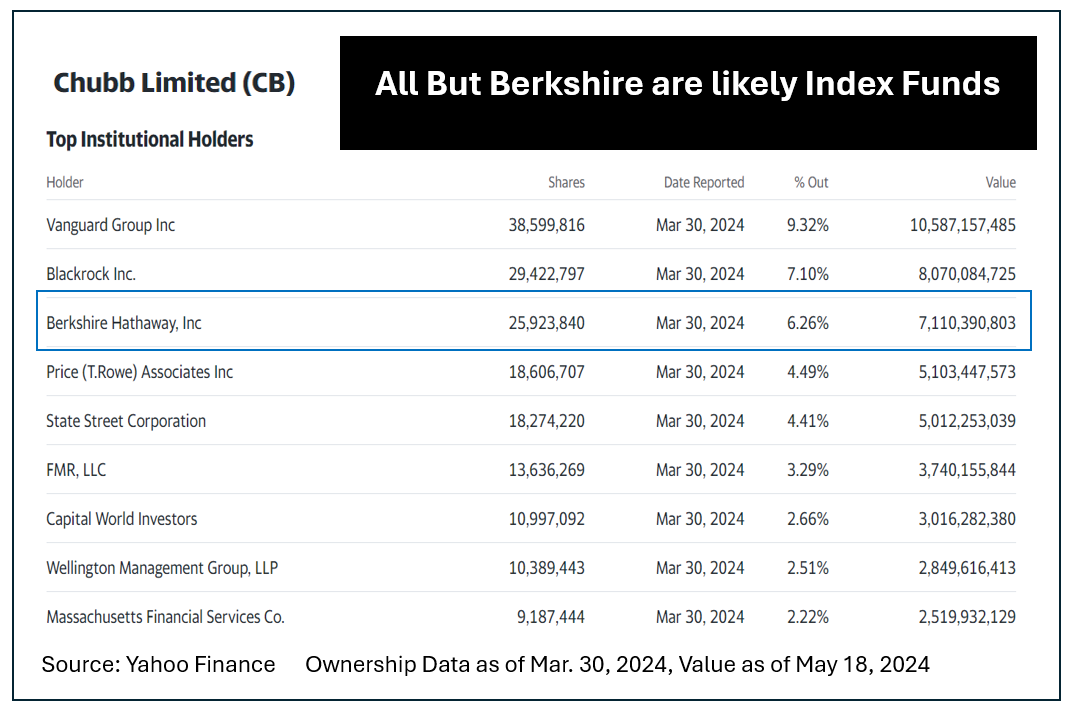

Berkshire Hathaway BRK.A BRK.B teased investors a few months back after getting a special dispensation to avoid disclosing large buys of a stock they said was still under accumulation.

That company turned out to have been Chubb Ltd. CB, the world’s largest publicly traded property-casualty insurance firm. From the third quarter of 2023 through March 30, 2024, Berkshire Hathaway bought up about 6.26% of the outstanding shares.

The end of March stake was worth about $7.11 billion as of May 20, 2024.

All other major institutional holders were almost certainly there as operators of index funds, rather than as active stock pickers.

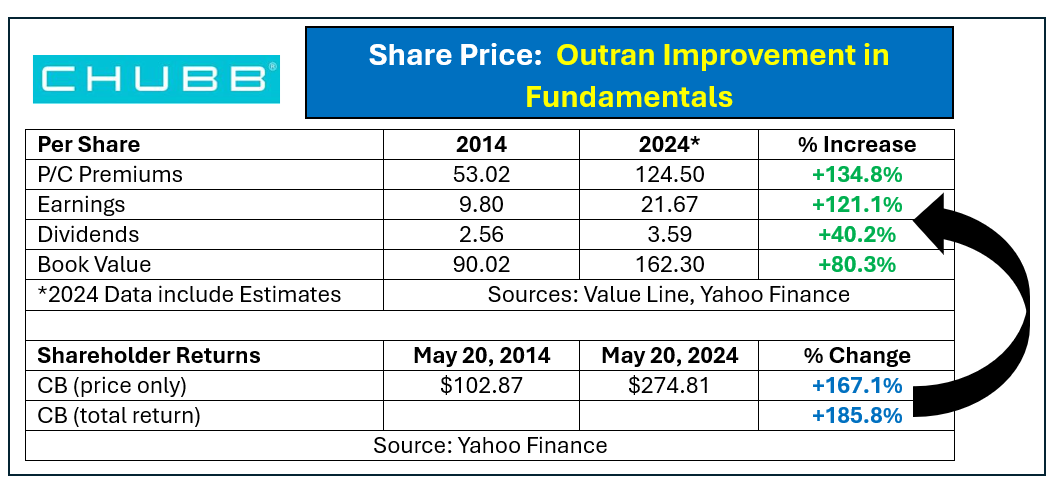

The past decade’s results show Chubb was a well-run and growing company. Assuming current year’s estimates prove reliable EPS grew by about 121% since the end of 2014 while dividends went up 40.2% and book value increased by north of 80%.

Unfortunately for investors buying in now, the stock price surged by more than the growth in fundamentals. The only way that can happen is through P/E expansion. Exactly 10 years ago CB’s P/E was 10.5x projected earnings and its yield was 2.48%. CB was changing hands for about 114.3% of book value.

As of May 20, 2024 the forward multiple sat at 12.3x while the current yield is only 1.32%. Chubb’s price to projected year-end book value is now quite high, at 169.3%.

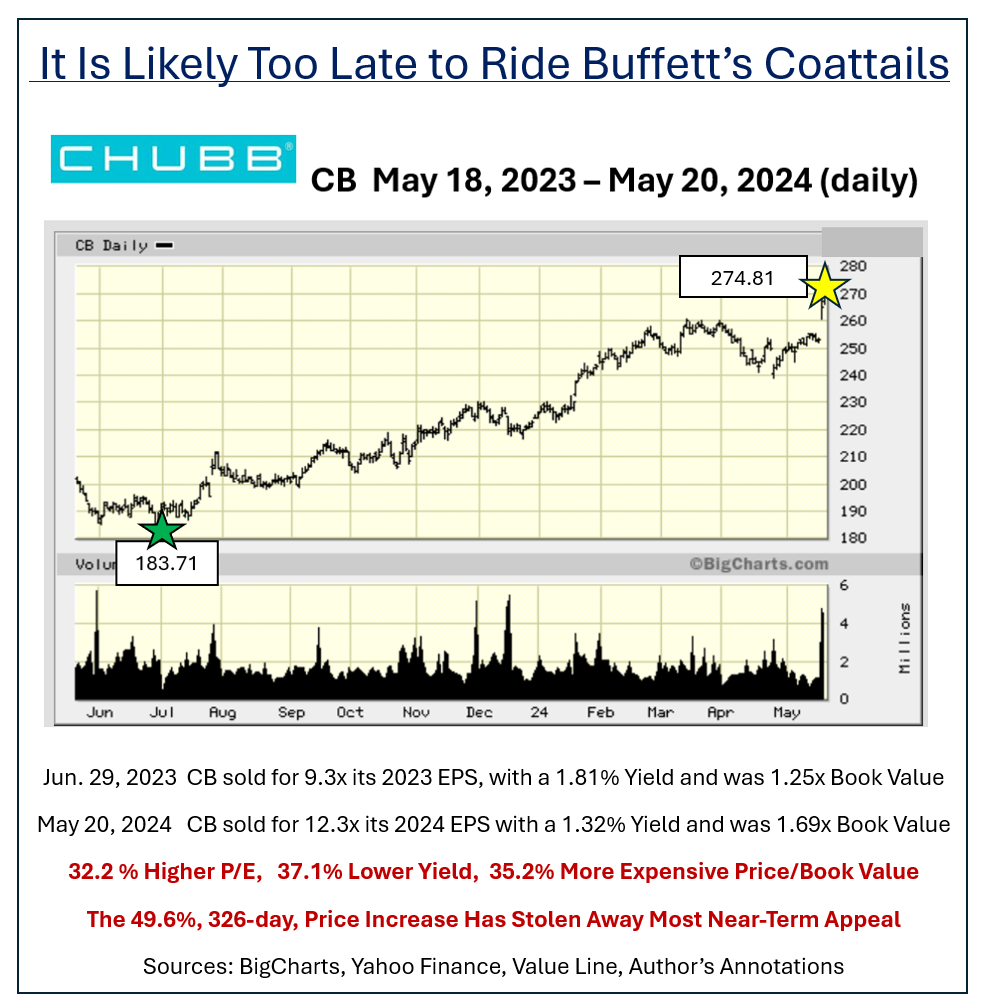

The stock’s almost 50% upturn from a June 29, 2023 low of $183.71 to last week’s quote of $274.81 took CB from a good valuation to somewhat above many historically normalized levels.

The “Buffett Effect” which refers to traders piling into recently disclosed purchases took CB up from about $253 to as high as $275.41 in a flash, as noted on the chart below.

What Is Chubb Worth?

Here are three ways to value Chubb right now.

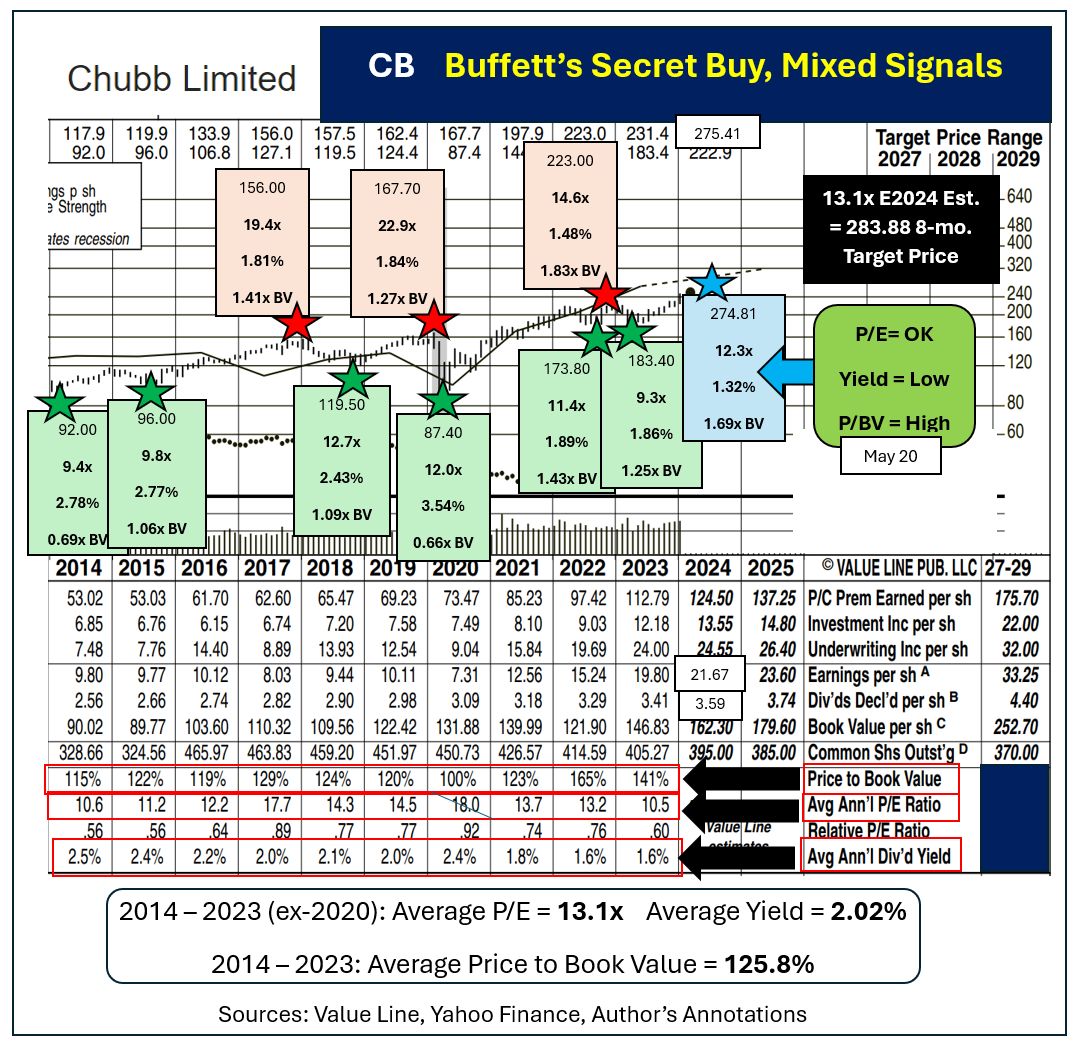

Normalized Price to Book Value of 125.8% (projected year-end 2024): $204.17.

Normalized P/E of 13.1 times estimated 2024 EPS = $283.88.

Reverse engineering the current $3.64 annual dividend to a historically average 2.02% = $180.20.

Two of those three methods say CB is pricey right now. Based on P/E there may be a small uptick left.

The six “best entry points” for Chubb (green-starred below) saw rallies begin from average P/Es of under 10.8x. Average yields at those moments ran 2.55%. Average Price to Book Value percentages ran just 103.3%.

Chubb’s three most obvious “should have sold” moments (red-starred) each came when the shares commanded above-typical P/Es. Yields at those times averaged sub-par levels of 1.71%. Price to BVs were elevated, at an average 150.3%.

Based on P/Book Value and yield, CB is now in dangerously expensive territory. Its medium-range P/E suggests neutral performance at best.

Buying CB now offers sub-par prospects unless Berkshire decides it wants to own the entire company and bids it up further to complete the deal.

I am not alone is seeing this.

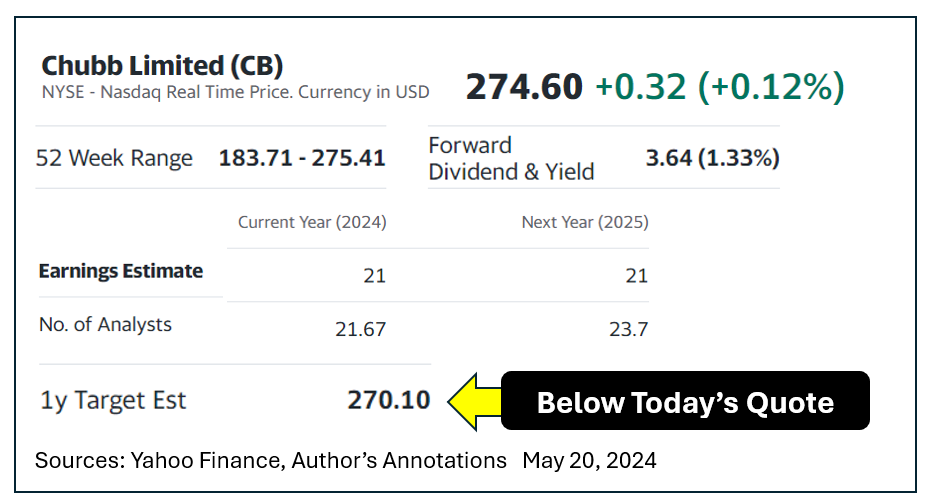

Yahoo Finance indicates a 12-month price target for CB of $270.10. That less-than-today’s price goal assumes record EPS in both 2024 and 2025.

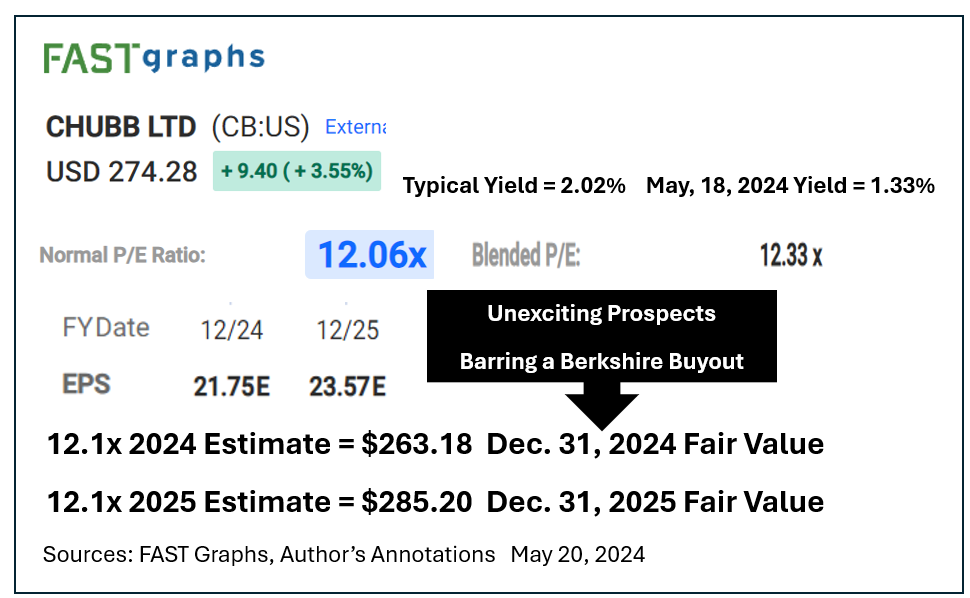

FAST Graphs calls a normalized P/E for Chubb as 12.06x. Applying a 12.1x multiple to their own EPS estimates for 2024 and 2025 calculate end-of-year price targets of $263.18 and $285.20, respectively.

Once again, there no good reason to own CB at today’s quote unless you are betting on a takeover.

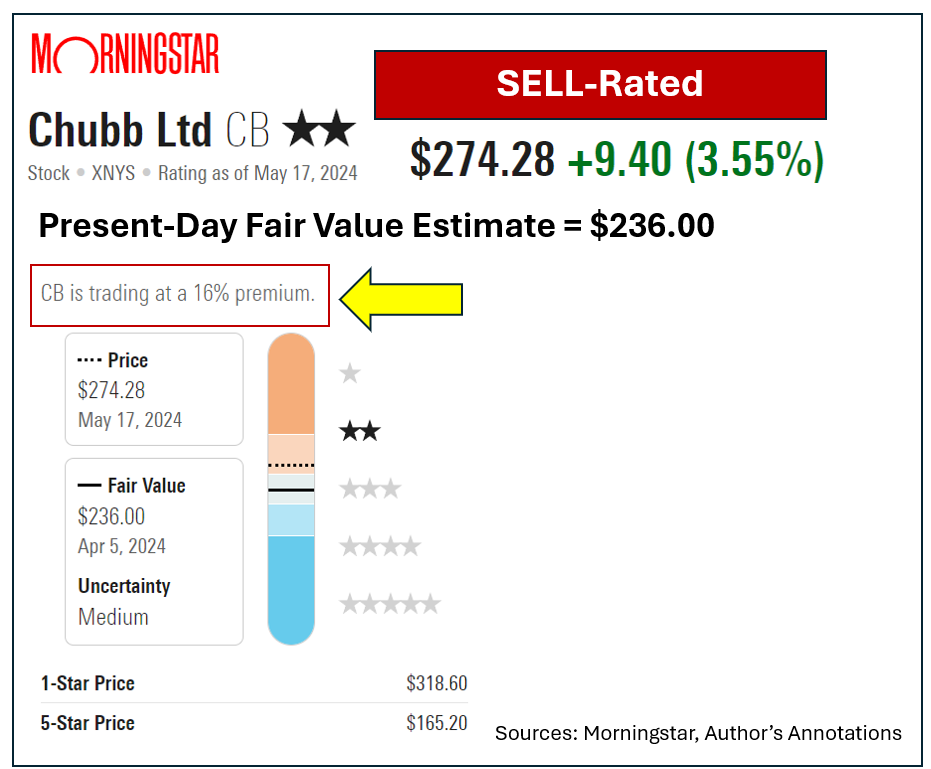

Research house Morningstar labels CB as a 2-star, out of five, sell. They say Chubb is fetching about 16% more than their present-day fair value estimate of $236.00.

More Paul Price:

- Forget Meme Players… What Is GameStop Really Worth?

- Is Value Investing Dead? You Make the Call

- Buying Income Is Hazardous to Your Wealth

Media talking heads love to praise Buffett for buying low. He is certainly ahead on his average cost basis on CB right now,

Think back to April of 2020 however, and the famous post-Covid panic interview with Becky Quicky on CNBC.

Traders and investors alike were dying to know what bargains Mr. Buffett had scooped up during the March 2020 plunge. Instead, Warren said he was a net seller of stocks back then while sitting on over $130 billion in cash. As of Mar. 30, 2024 that cash hoard had climbed to over $182 billion.

Instead he confesses he had sold off all his airline stocks while raising even more cash. When she asked why he did not buy he said, “I just couldn’t find anything worth buying.”

Berkshire has been a net seller of stocks for more than four full years now.

Berkshire Hathaway’s failure to buy Chubb in March 2020, briefly at south of $88 makes what he paid for it late last year and into 2024 look downright expensive.

Copying his move into Chubb, after its recent surge, is not promising unless you know that Berkshire is planning to make a bid for the whole company.

At the time of publication, Price had no positions in any stocks mentioned. He was a huge net buyer of stocks in March through October 2020.