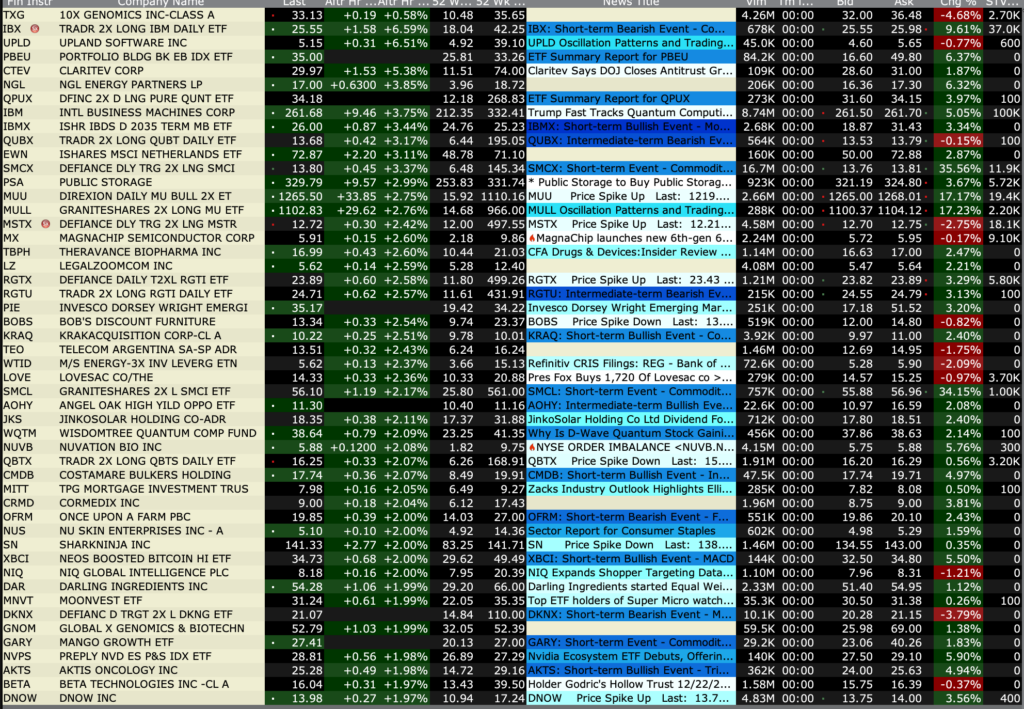

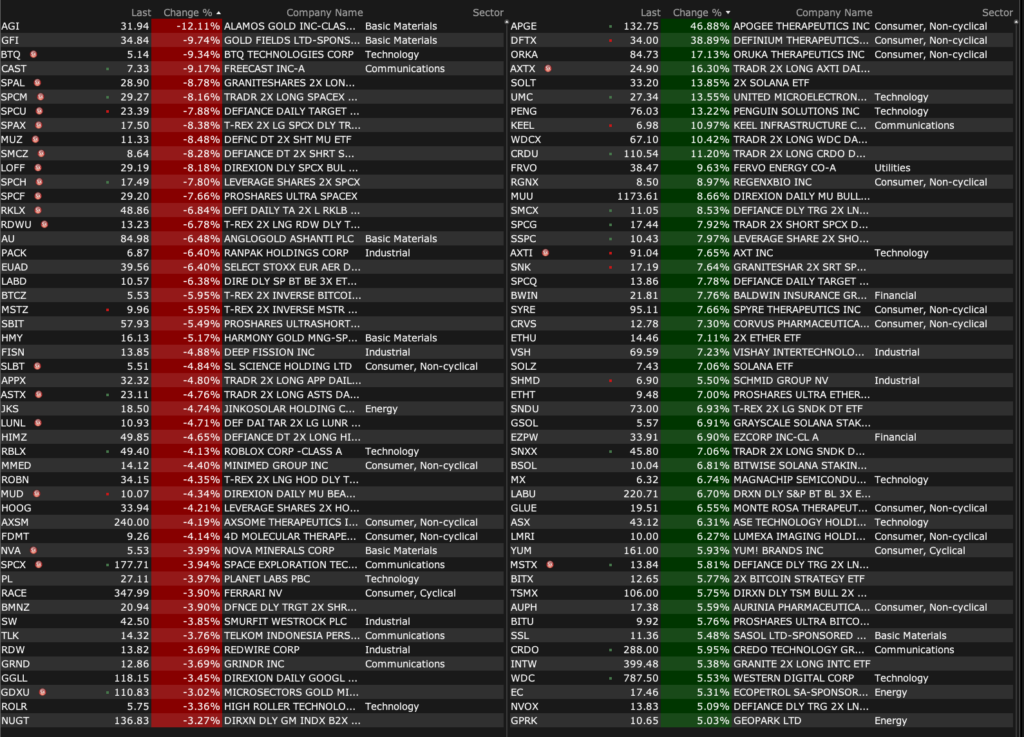

Monday’s After-Hours Advancers and Decliners

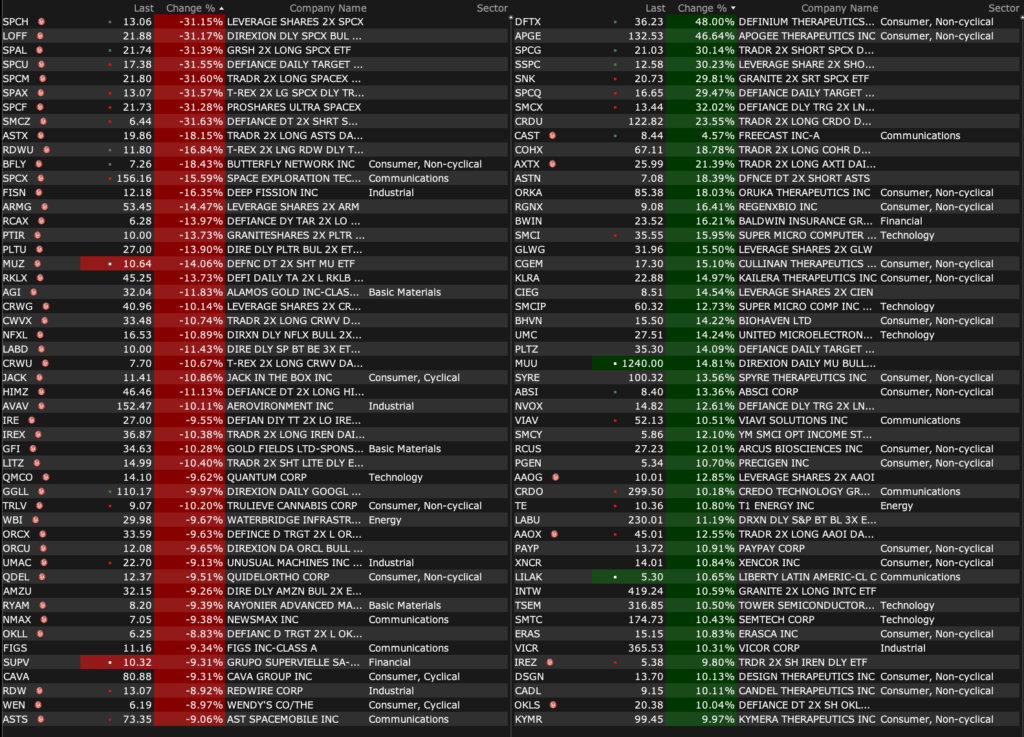

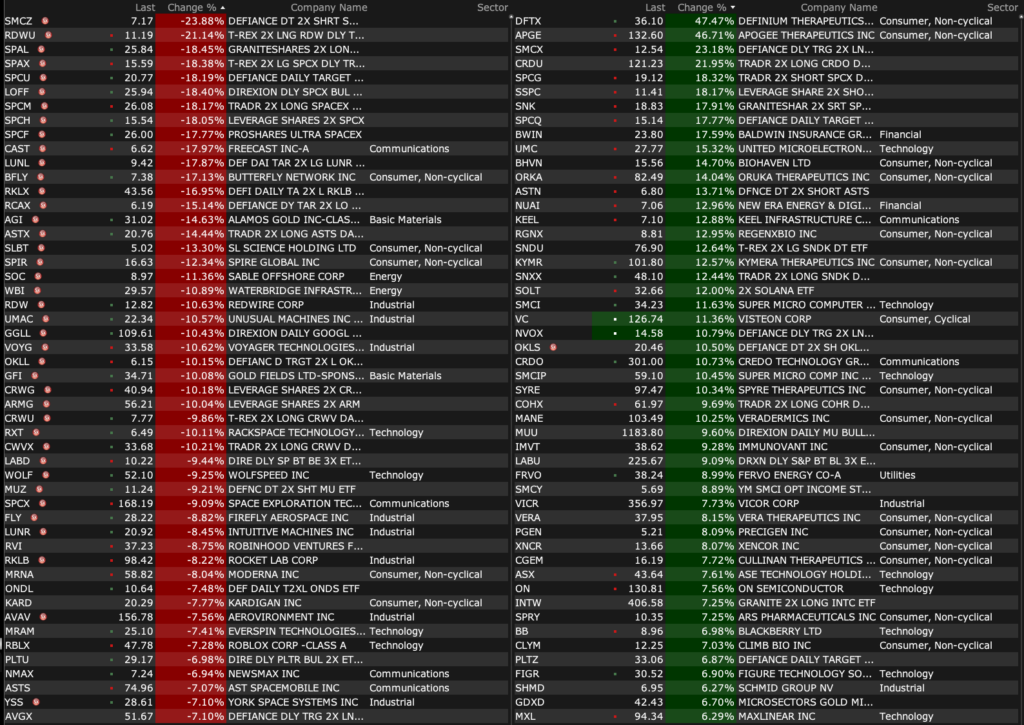

After-Hours % Advancers

After-Hours % Decliners

Position: None

BY Doug Kass · Jun 22, 2026, 4:45 PM EDT

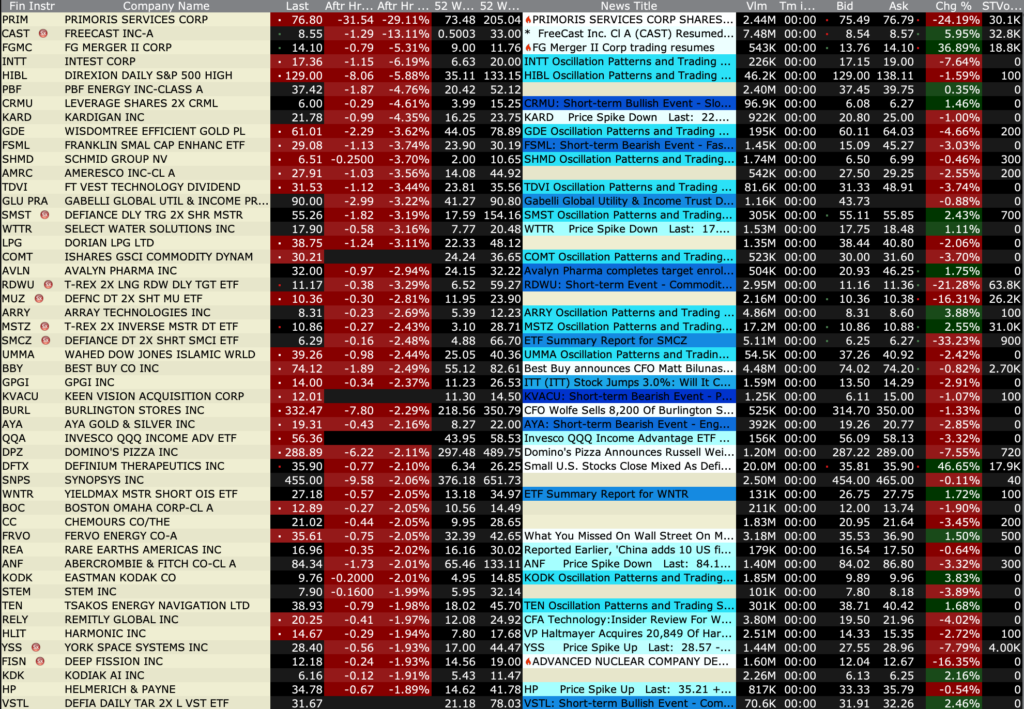

After-Hours % Advancers

After-Hours % Decliners

Position: None

BY Doug Kass · Jun 22, 2026, 4:45 PM EDT

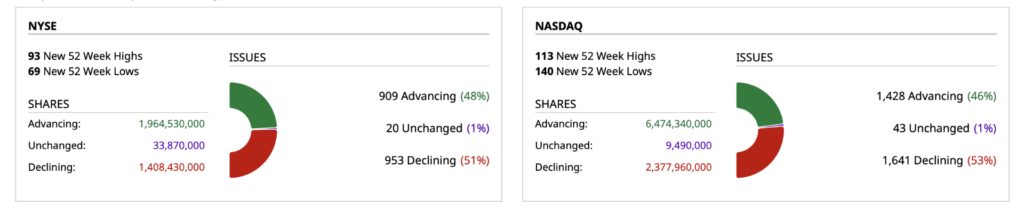

Closing Volume

– NYSE volume 7% below its one-month average

– NASDAQ volume 25% above its one-month average

– VIX index: up 5.61 to 17.32

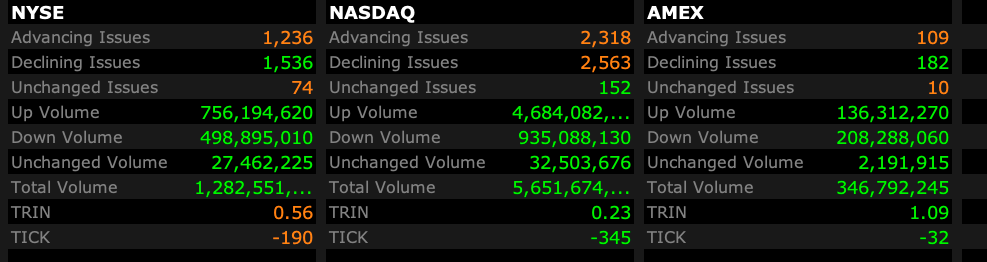

Breadth

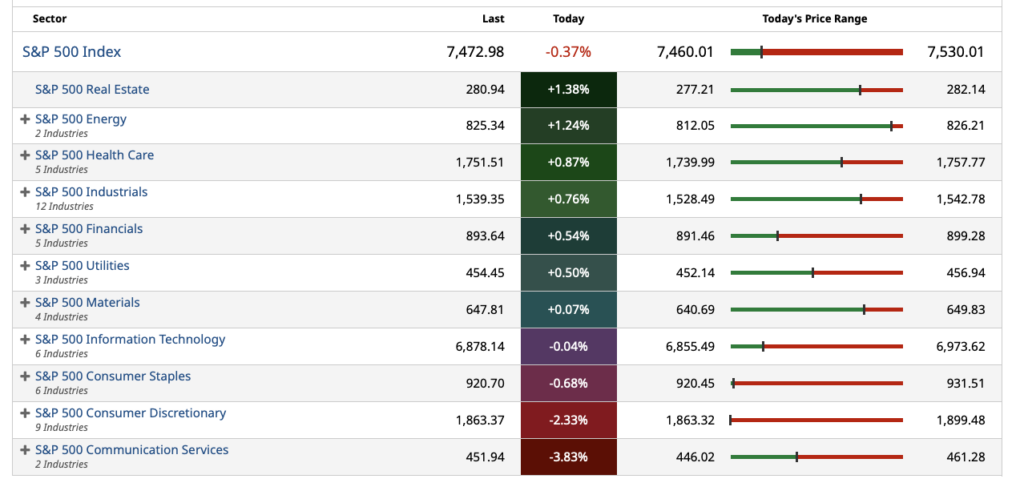

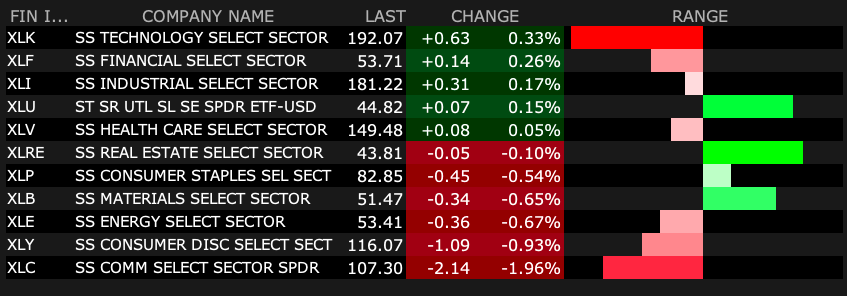

S&P 500 Sectors

% Movers

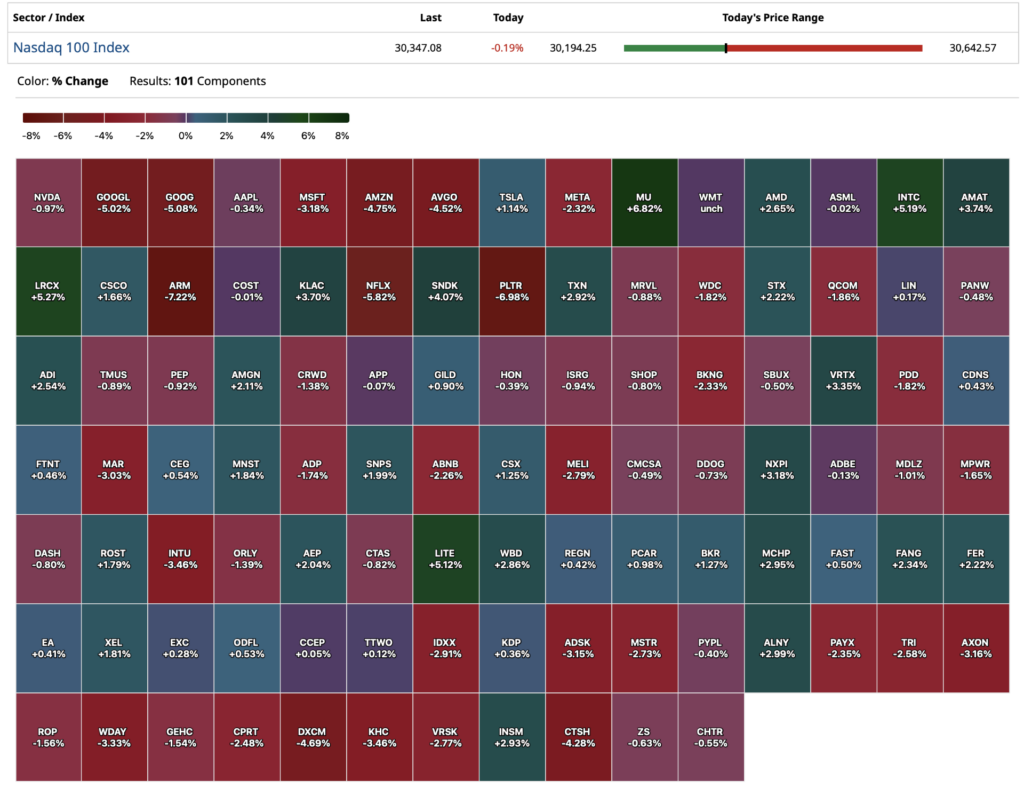

Nasdaq 100 Heat Map

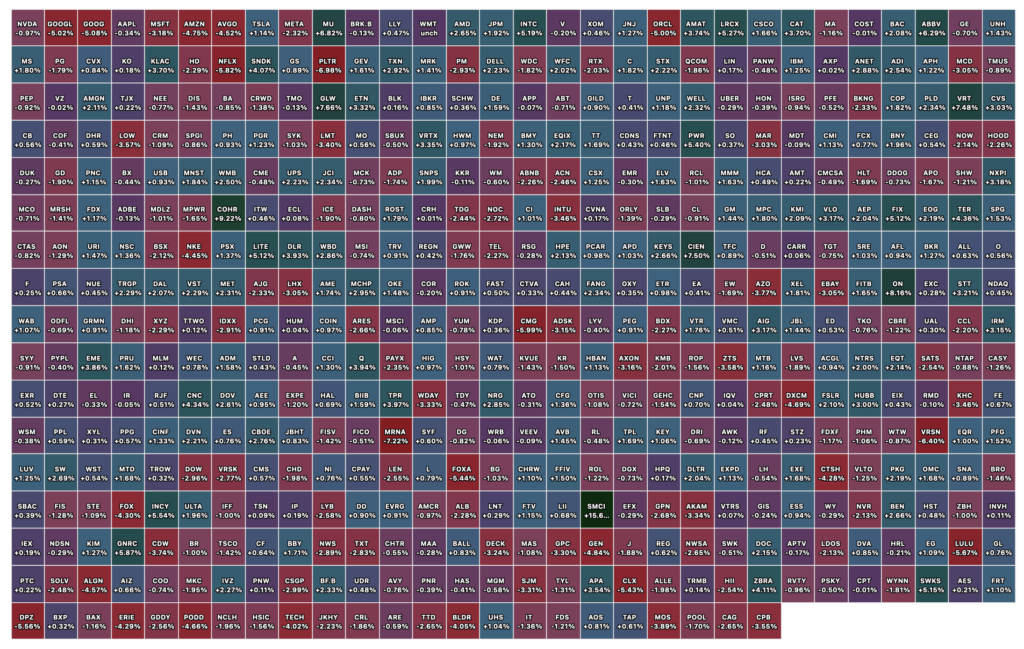

Closing S&P 500 Heat Map

Position: None

BY Doug Kass · Jun 22, 2026, 4:37 PM EDT

Position: None

BY Doug Kass · Jun 22, 2026, 3:58 PM EDT

Position: None

BY Doug Kass · Jun 22, 2026, 3:37 PM EDT

I have taken a small trading short rental in DRAM at $80.27.

Position: Short DRAM (S)

BY Doug Kass · Jun 22, 2026, 3:18 PM EDT

Here are today’s things:

* Shorted SPY at $749.07 and QQQ at $743.67 — covered SPY at $744.80 and QQQ at $737.99.

* Added to JOET short at $45.64 and GRNY short at $27.63.

* Shorted a package of high-beta tech.

* Shorted more MS at $227.32.

* Shorted more IWM at $297.07.

* Added to longs MSOS at $4.76, MSOX at $3.00, GTBIF at $7.55, VRNOD at $5.55, CURLD at $9.73 and TRLV at $9.40.

Position: Long MSOS (L), MSOX (VS), GTBIF (S), VRNOD (S), CURLD (VS), TRLV (S); Short high-beta tech package, JOET (S), GRNY (M), MS (M), IWM (S)

BY Doug Kass · Jun 22, 2026, 3:02 PM EDT

I have two research calls this afternoon — at 2:45 PM and 3:30 PM.

Radio silence.

Position: None

BY Doug Kass · Jun 22, 2026, 2:39 PM EDT

BY Doug Kass · Jun 22, 2026, 1:49 PM EDT

Position: None

BY Doug Kass · Jun 22, 2026, 12:50 PM EDT

and my related comments:

Position: None

BY Doug Kass · Jun 22, 2026, 12:41 PM EDT

– NYSE volume 7% below its one-month average;

– Nasdaq volume 52% above its one-month average;

– VIX index: up 6.59% or 17.48

Positions: None.

BY Doug Kass · Jun 22, 2026, 11:55 AM EDT

The sort of abysmal price action in MSFT, AMZN, GOOGL and META are EXACTLY the concerns I expressed in my market structure post.

I worry that today’s weakness in the precursor of a market structure event not similar to past disruptions:

The proliferation, popularity and acceptance of leverage products and portfolio concentration in quantitative strategies, margin debt, the options market and leveraged ETFs argue in favor of rising odds of another October 1987 (“Black Monday”) or a 2018 “Volmageddon” (or Vix Bloodbath) event.

Position: None

BY Doug Kass · Jun 22, 2026, 11:42 AM EDT

Positions: None.

BY Doug Kass · Jun 22, 2026, 11:16 AM EDT

Added to JOET (JOET) $45.64 short at and GRNY (GRNY) short at $27.63 .

Positions: Short JOET S GRNY M

BY Doug Kass · Jun 22, 2026, 11:07 AM EDT

I added to MS (MS) short at $227.31.

Position: Short MS S

BY Doug Kass · Jun 22, 2026, 11:02 AM EDT

With S&P cash – 26 handles I have covered my Index shorts:

* SPY (SPY) $744.80

* QQQ (QQQ) $737.99

From only 40 minutes ago:

With S&P cash + 24 handles, I am back shorting the indexes:

* SPY (SPY) $749.07

* QQQ (QQQ) $743.60

Positions: Short SPY VS QQQ VS

BY Doug Kass · Jun 22, 2026, 10:09 AM EDT

BY Doug Kass · Jun 22, 2026, 11:01 AM EDT

BY Doug Kass · Jun 22, 2026, 10:57 AM EDT

From Peter Boockvar:

I’ve argued many times that even when the conflict officially ends, the Strait reopens, and oil prices pull back in response, we are not going back to $65 on any sustainable basis, if at all. A key factor on the demand side to this belief is the global desire to build excess stockpiles, in addition to refilling the reserves already released. Reuters ran an opinion piece today from Ron Bousso titled “Iran war triggers global race to build oil reserves.” The piece said, “Vulnerable countries that paid a high economic price during the Iran war are seeking to build domestic oil and gas storage buffers against future shocks, a drive that could bring roughly half a billion barrels of additional demand down the pike.”

Further, “India is in clear need of larger strategic reserves. It is the world’s most populous nation, the 3rd largest oil importer and the 2nd largest importer of liquefied petroleum gas used for cooking, and is set to become the single biggest source of global oil demand growth through 2030, according to the IEA…Its reserve covers just eight days of imports; meeting the IEA’s 90 day standard would require more than 400 million additional barrels, costing roughly $28 billion at $70 per barrel.”

“Pakistan is in a similar position…Building reserves equivalent to 90 days of imports would require around 35 million additional barrels. Australia, the only full IEA member that consistently failed to meet the agency’s SPR requirement, has announced plans to spend $7 billion to hold at least 50 days of fuel. Other countries, including Asia’s top oil refining hub Singapore, are also considering building or expanding strategic oil and gas storage. Europe already has an extensive gas storage system to manage seasonal demand, particularly in winter. But…the region may opt to build additional government controlled storage.”

“Even energy producers are moving in this direction. Gulf national oil companies are seeking more storage outside the region to preserve export flexibility in a crisis.”

Bottom line, “Taken together, these new storage plans could require around 500 million barrels of crude and refined products,” based on their calculations. “Depleted inventories will also need refilling. Roughly 400 million barrels have already been drawn from global stocks since the start of the war, according to the IEA, with draws likely to continue through the summer even after Hormuz reopens. Combined, that amounts to roughly 1 billion barrels of additional demand. Even if spread over several years, it would provide significant price support.”

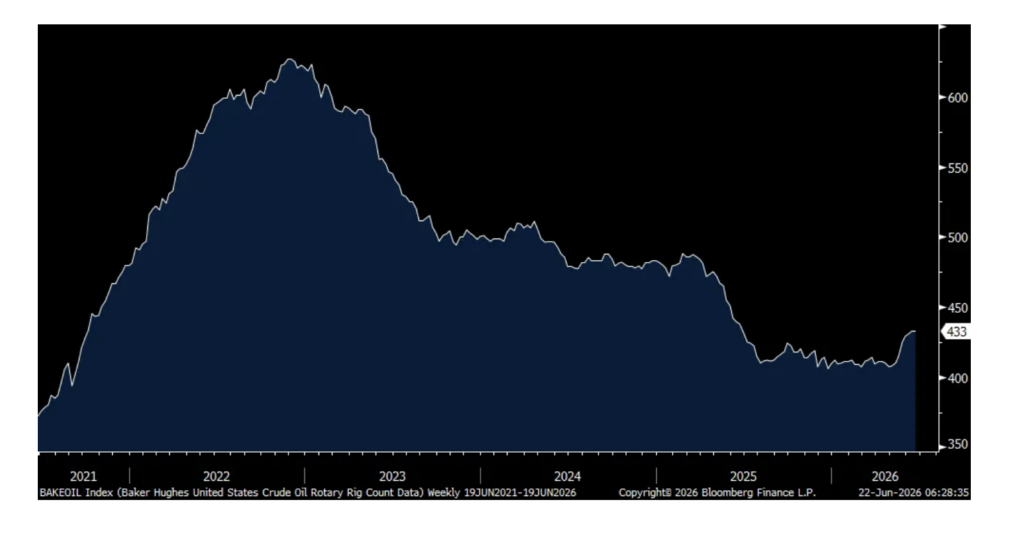

A check on the US oil rig count, after rising for 8 straight weeks and by 26 rigs during this time frame to 433, there was no change w/o/w as of 6/19.

Baker Hughes Crude Oil Rig Count

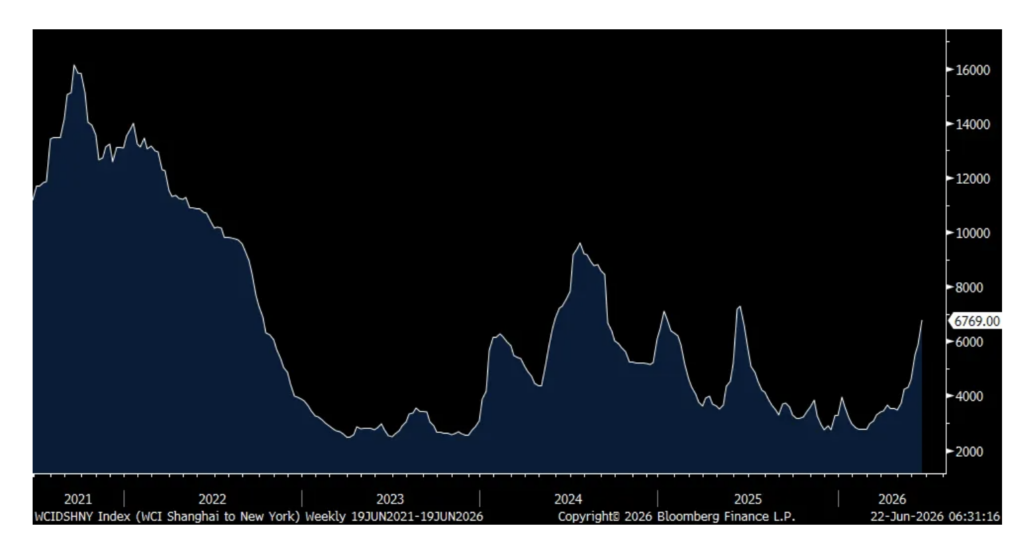

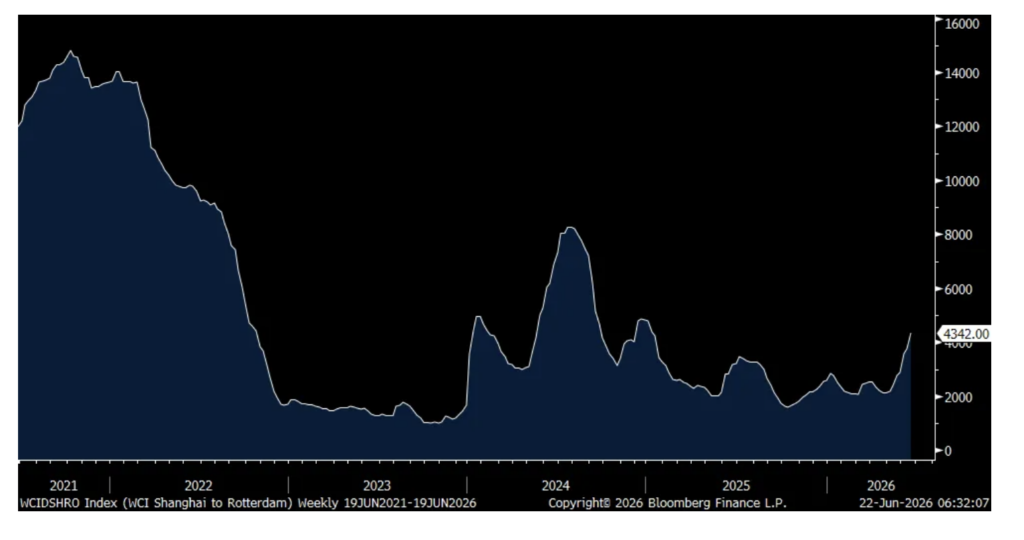

Another check on container shipping prices and we’ll see in coming weeks to see if we get any collateral relief with hopefully the Strait fully reopening. As of 6/18, the price of a 40 foot container from Shanghai to NY jumped again to $6,769, up by 17% w/o/w to the highest in a year. Shanghai to Rotterdam saw prices rise to the most since January 2025 at $4,342, up 15% w/o/w.

Shanghai to NY

Shanghai to Rotterdam

When analyzing under the hood of the US economy, in the context of the two lane highway I keep mentioning, the case is the same when it comes to CapEx. There is CapEx on building on the GenAI infrastructure and CapEx on everything else. The former is growing tremendously as we know, but there is little growth with the latter. This was from Accenture on Friday, a stock that fell by 18%:

With regards to corporate IT budgets, “Even with AI, they’re spending it differently, but they haven’t been increasing.”

Also of note from their call, “we were impacted by the conflict in the Middle East. We saw a revenue impact of approximately $100 million compared to our expectations, which was all consulting type of work, split evenly between the direct impact on our Middle East business and indirect effects outside of the region. In the last few weeks of the quarter, we saw this indirect impact globally in products and to a lesser degree in resources, mostly in discretionary spend.” As an example of the ‘indirect impact’, “some of the industries are dealing with kind of longer-term issues, so think about automotive, where we have a large presence. They were already challenged. And now with the higher gas prices, that’s added to it.”

Overall, they are optimistic about the AI opportunity “We believe that AI will be a tailwind for us and our industry as it scales because it is a catalyst for reinvention and is creating new opportunities for growth and efficiency for our clients and for us.”

Shifting to the US consumer, this was from Kroger and whose stock fell 8% Friday:

“The customer is under pressure. Higher gas prices and reduced SNAP benefits are squeezing budgets. Customers are managing spend carefully and shopping with real intent. That pressure is showing up in the market. Food-at-home growth decelerated 100 bps compared to the last quarter. Encouraging news is that our work on affordability is starting to resonate and you can see it in the data.”

“Traffic is up. Customers are coming through our doors more often, which tells me our value messaging is starting to land.”

“Food inflation came in at the low end of our expectations, down sequentially from the fourth quarter. Egg deflation was a meaningful headwind to identical sales without fuel, representing 64 bps of pressure.”

“Looking ahead, we expect inflationary pressure to increase as the year progresses, reflecting the broader macro environment.”

With respect to the not surprising resignation of Keir Starmer as the PM of the UK, there isn’t much of a market impact with the pound little changed, the FTSE 100 slightly higher and gilt yields lower, along with its European peers. Wes Streeting is the business friendly Labor party candidate but the betting markets have a 90%+ chance that Andy Burnham, left of Starmer, will be the next PM. I continue to believe the the UK stock market is a treasure trove of cheap stuff.

Positions: None.

BY Doug Kass · Jun 22, 2026, 10:50 AM EDT

With S&P cash + 24 handles, I am back shorting the indexes:

* SPY (SPY) $749.07

* QQQ (QQQ) $743.60

Positions: Short SPY VS QQQ VS

BY Doug Kass · Jun 22, 2026, 10:09 AM EDT

*Anyone who has observed the market’s spectacular intraday volatility and outsized daily swings over the last several weeks should realize that something is amiss — the market is not behaving normally, it seems destabilized.

* The proliferation, popularity and acceptance of leverage products and portfolio concentration in quantitative strategies, margin debt, the options market and leveraged ETFs argue in favor of rising odds of another October 1987 (“Black Monday”) or a 2018 “Volmageddon” (or Vix Bloodbath) event.

* As noted in my Diary over the last few months, the market has grown casino-like in which gambling has been encouraged and traders have adopted the mindset of race-track bettors.

* Price discovery has become distorted and compromised as an increased number of market participants worship at the price of momentum (and not value) — in this backdrop YOLO (“you only live once”) investing and FOMO (“fear of missing out”) are conspicuous (and potentially toxic) conditions.

* But as night follows day and at a date uncertain, the market will discover that momentum is a two-way street that travels faster and more persistently on the downside than it does on the upside.

* In summary, changes in market structure that are implicitly celebrated in rising markets pose an unfathomable risk on the downside.

“Whenever you find yourself on the side of the majority, it is time to pause and reflect.“

– Mark Twain

The current speculative and levered conditions in the market remind me of the investment backdrop that immediately preceded the dramatic market declines of Black Monday (October 1987) and Volmageddon.

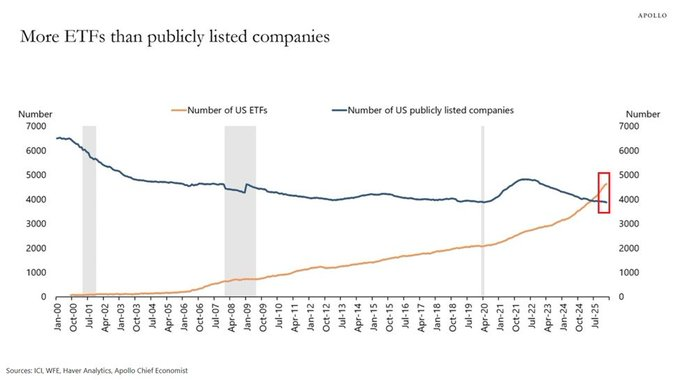

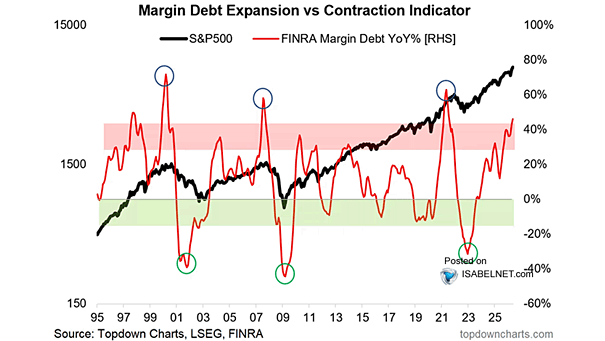

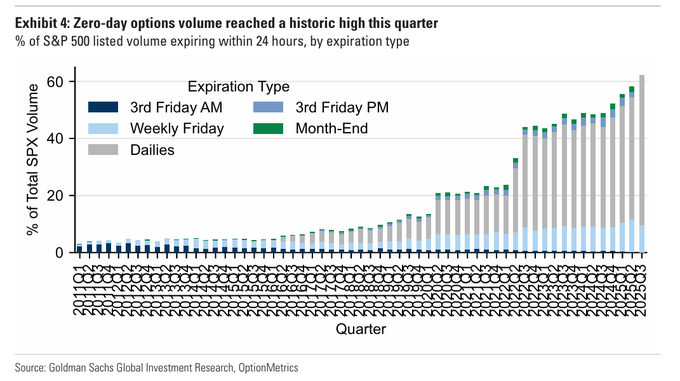

Never have passive funds and levered quantitative strategies been so dominant, leveraged ETFs so popular (total listed ETFs now surpass the number of listed individual equities), margin debt so high and options markets been so time compressed (with 0DTE options representing 2/3 of total options trading):

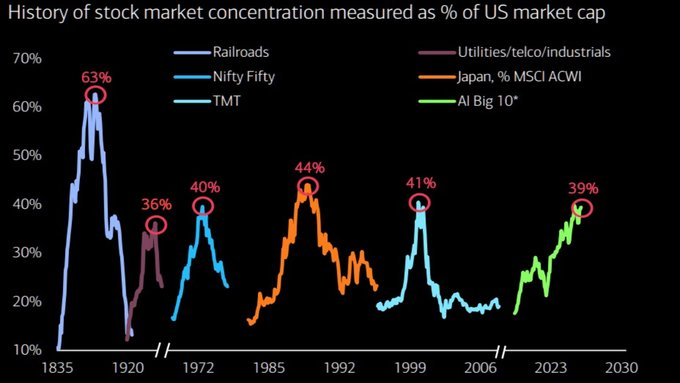

Market concentration is at an extreme:

I can see several catalysts that could hasten an abrupt market dive or flash crash, including (but not restricted to) a marked acceleration in the rate of inflation, an unexpected geopolitical event, an abrupt rise in interest rates, evidence that the massive AI capital spending boom will not deliver adequate returns on investment, a negative fundamental development in semis/memory, a swift drop in the price of bitcoin, an accounting scandal (which often occur at the end of a benign market cycle), a failed Treasury auction, or a Gammageddon, among other factors.

However, in all likelihood it will be an event that no one is predicting and no one is prepared for.

Back in late 2024 I cautioned about and delved into the unexpected and leveraged corners of speculation (reposted here in its entirety):

——–

* The entirety of the recent four-week market advance has been based on an expansion in price earnings multiples.

* As narratives multiply and fear/doubt disappear, guards and disciplines are dropped with many asset classes at all-time highs.

* But as asset prices rise, diligence and the assessment of reward vs. risk should take on greater irrelevance – unfortunately just the opposite is occurring.

* And so should the concept of “a margin of safety” be evermore embraced – as it is an essential and integral ingredient to investing over a “market cycle.”

* Expect the unexpected…in the corners of leverage and those that are endorsing the narrative of a “new paradigm” (of higher valuations).

“What the wise man does in the beginning, the fool does in the end.”

– Warren Buffett

“A bull market is like sex, it feels best just before it ends.”

– Barton Biggs

Over history, market inflection points and economic dislocations often come from places not anticipated. Indeed, the most important turning points in markets (and in life) often come at the most unexpected times and in the most unexpected ways. In particular, leverage, as proven by history, is often uncovered in unexpected places. Think about the collapse of a generally unknown currency, the Thai Bhat that gripped Asia in 1997 and then spread to other countries (with a ripple effect), raising fears of a financial contagion and a worldwide economic meltdown. Or the failure of the highly leveraged (and formerly successful) Long Term Capital hedge fund (managed by several Nobel Prize winners in economics) in the following year — which was, in part precipitated by the Russian Debt crisis in 1998 and required a multi billion dollar bailout by 14 banks (orchestrated by The New York Federal Reserve). But the best example of hidden leverage (where no one was looking) was seen in The Great Financial Crisis of 2007-09 when one overleveraged segment, real estate, proved to be the Achilles Heel for the global economy.

Indeed, what started out as what many believed to be only a few California mortgages under water, multiplied geometrically and almost bankrupted our worldwide financial system — as the layers of leverage were swiftly uncovered and spread rapidly. This morning’s market commentary will highlight several significant market (and economic) risks that are not regularly discussed.

The “failure” or combustion of any of these factors could have a most adverse impact on equities and on the domestic economy.

* The U.S. economy has never been more levered to the U.S. stock market. Indeed, one can argue that — with household ownership of equities at an all-time high, with a chorus of “its different this time” and with dreams of a new investing paradigm (of higher valuations) dominating the narrative. As discussed below, it is almost as if the domestic economy is being collateralized by a foundation asset, equities.

From Tom Dyson:

The US stock market is such a foundational asset. You could say, the US stock market has become the collateral that backs the world economy, and all its debt. As long as the stock market keeps rising, everything’ll be okay. But as soon as it turns down, things will start breaking. Employment, real estate values, consumption, trade… and even the government’s finances. It’s the wealth effect, when the stock market is such an important store of wealth. They all rely on a strong stock market to function. The fact that the world’s prosperity has one single point of failure – even as it rises day after day – should terrify you. The market’s function should be to allocate scarce capital efficiently… not collateralise the entire system. In effect, it’s become too big to fail, which is an acute fragility for our capitalist system. As allocators of capital ourselves, how should we approach our investment discipline in a market where expectations (and stock market values) are literally “off the charts”? The bears say “every other time this has happened, there’s been a big wreck.” The bulls say “this time is different, and besides, the trend is your friend and getting the timing wrong is the same as being wrong. “What do you do? Neither position is falsifiable. Which means there is no way to figure out the correct answer with logic… or research… or data. So it comes down to philosophy. Are you a contrarian? Or are you a trend-follower?… The global debt stock surged by over $12 trillion in the first three quarters of 2024 to a record high of nearly $323 trillion. It’s a huge wealth bubble and when it pops, $400 trillion or $500 trillion of (mostly) paper claims ($323 trillion in debt plus whatever owners’ equity the system has) will rush for the exits and seek safety. And policy makers won’t be able to stop it.

* Elon Musk’s health and business/innovative successes are critical to a continuation of economic growth and stock market gains. Musk’s broad reach — on the road, under ground, in space, over the internet, in defense, in artificial intelligence — has now advanced into Washington, and in the formulation and implementation of policy. To have one person so immersed and involved in all these critical areas could pose broad risks — in many ways.

* An extremely leveraged cryptocurrency market represents potential systemic risks. It is my view that cryptocurrency is “the mother of all bubbles” perpetuated by a number of factors (including the rejection of fiat money) and developing digital narratives — many of which have a weak foundation of logic. The absurd notion that the limiting of supply of bitcoin is as stupid as it is damning — as there is no limit to the supply of other cryptocurrencies. To this observer, the sheet market size of bitcoin and other cryptocurrencies is a manifestation of the risks.

See: Crypto Market Cap Charts | CoinGecko

And, as I have written, MicroStrategy (MSTR) (with its “math” in expressing the case of buying $1 bills for $3 and MSTR’s multiple derivative plays), is the standard bearer of the digital speculation today. See: TheStreet Pro

When the cryptocurrency markets implodes, which is my baseline expectation, the contagion effect will likely be pronounced on all of the capital markets.

* Both fiscal and monetary policy – which is needed to secure the foundation of growth — are travesties. Neither political party has been fiscally responsible — the profligate spending over the last few decades continues apace. (I do not, in any way, buy Elon Musk’s objective of cutting $2 trillion from the U.S. budget, as when you go over the numbers only about $1.5 trillion can be cut (and that is if one cut all that was “available” to be cut in total). As well, the Federal Reserve has been guilty of reckless, feckless and fatuous policy in its delayed response to inflation and, then, in effecting a rapid rise in interest rates. I have little confidence in Powell’s Fed steering clear of debris in his remaining time at that institution. Nor am I confident in any Fed chairman that might replace him.

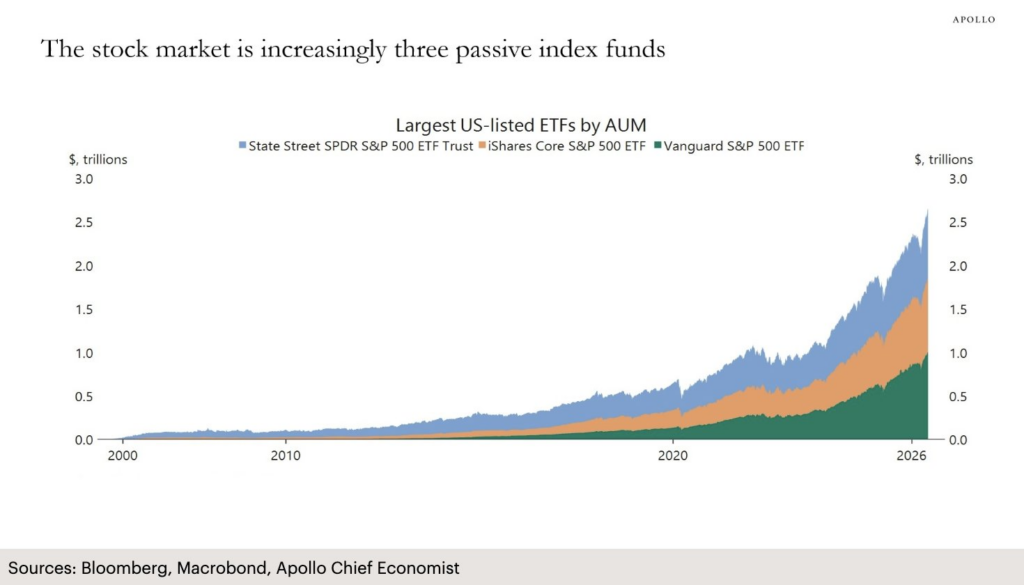

* Changing market structure poses a significant market risk. Passive investing has engulfed the stock market landscape. We are all traders now, on the same side of the boat and worshipping at the altar of price momentum. (See the first bullet point!) Massive inflows into passive strategies and products have been the straw that has stirred the market’s drink:

In part, those inflows, have contributed to a near unprecedented narrowing in the equity risk premium (to 20-year lows) while the risk to earnings growth are at 20-year highs:

I can guarantee you (and history has proven) that these inflows — as well as FOMO and the animal spirits — will not be permanent conditions.

“We must stop regarding unpleasant or unexpected things as interruptions of real life. The truth is that interruptions are real life.”

– C.S. Lewis

The history of speculation is that it resides in areas that are rationalized (with broadening acceptance of a new paradigm).

It is also the condition of history that it is fueled by leverage and lasts longer than most expect. But excesses are never permanent. They become ever more dangerous when markets are consumed with optimism, are no longer fearful and are levered up.

Position: None

BY Doug Kass · Jun 22, 2026, 9:50 AM EDT

Into this morning’s market ramp I have put back on my speculative short basket.

This is my third foray into this.

As mentioned in my GRNY (GRNY) and JOET (JOET) post (previous) this typically is a very very short term and opportunistic trade.

A true rental.

Positions: Short High Beta Tech Package

BY Doug Kass · Jun 22, 2026, 9:48 AM EDT

* Among other reasons, I now want to be short momentum.

I plan to aggressively expand my (GRNY) short now and to continue to modestly expand my (JOET) short (despite my fondness for its portfolio manager Joe Terranova).

Let me give you two straightforward reasons for my tactics:

* Both ETFS are grounded in momentum-based investing. Here are the holdings of GRNY (GRNY Holdings – GRNY GRNJ GRNI | Fundstrat Granny Shots ETFs) and JOET (JOET – Portfolio – Virtus Terranova US Quality Momentum ETF | Morningstar). Given my increasingly negative near term market view I want to now be short momentum (i.e., the leading edge of market leadership). Shorting these ETFs satisfies my objective of shorting momentum and conforms to my conservative risk profile and appetite, as, for me, it is too dangerous (save very very short term forays on the short side) to position short in SNDK (SNDK), MU (MU), AMD (AMD), INTC (INTC), AMAT (AMAT) et al.

* Both ETFs rebalance with strict multi month disciplines. This disadvantages both ETFs in the event of a violent change in sector leadership. In other words, why be long a momentum based ETF if one hand is tied behind its back?

Any questions about this, please comment in The Comments Section.

Short GRNY M JOET S

BY Doug Kass · Jun 22, 2026, 9:35 AM EDT

-GETY +121% (announces display partnership with OpenAI)

-DFTX +65% (reports positive Phase 3 Emerge topline results for DT120 ODT in MDD; met primary and all key secondary endpoints)

-APGE +47% (confirms to be acquired by AbbVie for $135.11/shr in $10.9B cash deal)

-RGNX +11% (reportedly FDA drops requirement for Regenxbio’s placebo-controlled trial; FDA agrees to reverse rejection of Navsunli gene therapy)

-BWIN +10% (JPMorgan Chase and Co Raised BWIN to Overweight from Neutral, price target: $28)

-FRVO +10% (announces agreement to develop EGS-Twin digital twin platform for Enhanced Geothermal Systems; reports earnings)

-ACA +7.5% (to be acquired by CRH at $150/shr in all-cash deal valued at $8.5B)

-PLBY +7.2% (repurchases 16.6M shares from Fortress at $1.05/share for ~$17.4M)

-MLTX +6.7% (announces Week 52 Results of Sonelokimab from its Phase 3 VELA Program in Hidradenitis Suppurativa)

-VC +5.5% (multiple broker upgrades)

-SMCI +5.3% (hearing upgraded at boutique firm)

-INTC +3.0% (hearing Mizuho raises price target; momentum)

-ACHV +2.9% (receives FDA CRL for cytisinicline NDA; No efficacy or clinical safety deficiencies identified)

-BTQ -10% (files to sell at the market C$150M equity offering)

-MPLT -4.9% (ML-004 IRIS Phase 2 misses primary social communication endpoint in ASD)

-SPCX -3.8% (confirms to launch inaugural senior unsecured notes offering)

-AMBQ -2.9% (files to sell 1.8M shares)

Positions: None.

BY Doug Kass · Jun 22, 2026, 9:26 AM EDT

Positions: None.

BY Doug Kass · Jun 22, 2026, 8:50 AM EDT

8:00 a.m.: Fed Treasury Repo Reference Rate; 11:30 a.m.: Treasury hosts an $89 3 and a $77B 6-Month Bill Auction

9:00 a.m.: Fed Board Governor Christopher (Voter) gives welcome remarks before the Fifth Conference on the International Roles of the U.S. Dollar hosted by the Federal Reserve Board, Washington, DC

(Text available. No Q&A. Livestream at https://www.federalreserve.gov/ and https://www.youtube.com/federalreserve )

Positions: None.

BY Doug Kass · Jun 22, 2026, 8:38 AM EDT

Positions: None.

BY Doug Kass · Jun 22, 2026, 8:23 AM EDT

Position: None

BY Doug Kass · Jun 22, 2026, 6:20 AM EDT

New short position put on late Thursday.

From the Comments Section:

Dougie Kass

I shorted IWM at $295.67 near the close and after hours.

First time long time.

Position: Short IWM (S)

BY Doug Kass · Jun 22, 2026, 6:05 AM EDT

The S&P Short Range Osclllator remains overbought at 1.77% vs. 1.99%.

Postion: None

BY Doug Kass · Jun 22, 2026, 5:55 AM EDT

Dougie Kass

800PM

With futures -59 handles I covered my Index shorts from Thursday (Friday was a holiday!):

From Thursday:

Here are today’s things:

* Re-shorted SPY at $746.68 and QQQ at $736.53.

* Re-shorted GRNY at $27.49 and JOET at $45.57.

* Added to cannabis longs: MSOS ($4.69), MSOX (new position) and GTBIF ($7.49).

* Shorted more MS at $228.47.

Position: Long GTBIF (S), MSOS (VL), MSOX (VS); Short SPY (S), QQQ (S), GRNY (VS), JOET (VS), MS.

BY Doug Kass · Jun 18, 2026, 11:55 AM EDT

BY Doug Kass · Jun 22, 2026, 5:49 AM EDT

The 30-year mortgage rate is back at 6.5% — nearly 2.5 times its 2021 low of 2.6%. The Fed's bond holdings have quietly helped hold mortgage rates down. New chair Warsh wants to shrink the "bloat" — a move that could push mortgage rates even higher.

The embedded tweet could not be found…

The embedded tweet could not be found…

In less than ten trading sessions, SpaceX priced its IPO at $135, surged to almost $220, and has now retraced to $166. In other words, investors who were lucky enough to acquire their exposure at the IPO are currently up 23%, while those who were very unlucky and bought at the Show more

The Emperor Has No Clothes: Why the AI Infrastructure Buildout Math Doesn't Work I have to give IBM CEO Arvind Krishna credit. He's saying what many of us in this industry have been thinking but haven't been willing to say out loud. The math just doesn't add up. Here's what I'm Show more

🚨Hedge funds are ALL-IN on US semiconductor stocks: Semiconductors now reflect a RECORD 14% of hedge fund long US equity portfolios. This percentage has more than QUADRUPLED over the last year. TAP IMAGE TO SEE FULL INSIGHT👇 globalmarketsinvestor.beehiiv.com/p/the-s-p-500-…

Last wk, the Wednesday FOMC mtg led to a sell-off in both bonds and stocks but Thursday saw a rebound leading to a solid wk w/ S&P +0.9% led by Semi Index +7% & oil down 9% to $78. The yld curve though did flatten last wk with 2y +10 bps while 30y -7 bps. As I previewed last Show more

Charlie Munger on meme stocks and short squeezes: "It's really stupid to have a culture which encourages as much gambling in stocks by people who have the mindset of race-track bettors." "I have a very simple idea on this subject. I think you should try to make your money in Show more

I am old enough to remember when every Fin TV panelist was overweighted $MSFT $AMZN $META $GOOGL Now, crickets. Ignored were, among other things, our concerns that the MAG7 was moving from capital light to capital intensive. Sorry to be blunt, but I call BS to the non Show more

Leveraged excess, unwaving optimism, and concentration. Read: "An Adverse Market (Structure) Event Is Growing More Likely" Now on the blog tab of seabreezepartnerslp.com

U.S. Equities saw an inflow of $141 Billion over the last month, the largest monthly inflow in history 🚨