SoFi's Down, the CEO's Buying and So Am I

I always take note when CEOs put their own money on the line when a stock trades lower. But my conviction for this name is based on more than that.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

I'll be adding to one of my higher conviction long-term long positions later today.

SoFi Technologies SOFI has run in fits and starts. Up and down. The trend since March has been mostly down. On Tuesday morning, SoFi reported that it had placed a $350M personal loan securitization exclusively with funds and accounts managed by Prudential Financial PRU and PGIM Fixed Income.

SoFi CEO Anthony Noto commented: "We've continued to see healthy demand for our personal loan sales, providing us access to new forms of capital as SoFi helps more members get their money right, PGIM's experience as an asset-based finance lender, coupled with its established securitized product platform, makes the company a great partner for SoFi as we continue to strengthen our lending capabilities."

According to BusinessWire, SoFi has now sold more than $15B and securitized more than $14.5B worth of personal loan collateral, which underscores the quality of SoFi's personal loan portfolio.

Looking Back

We see that CEO Anthony Noto purchased another 28,775 shares of common SOFI stock on May 3 for a little less than $200K, bringing his personal stake up to more than 8.03M shares. I always watch for CEOs who put their own money on the line when a stock trades lower.

About 10 days later, analyst Dan Dolev of Mizuho Securities, who has been a supporter, reiterated his "buy" rating and $12 target price after meeting with some of SoFi's executives, including CFO Chris Lapointe. Records show that Lapointe is long more than 1M shares in his personal account as well.

That day, Dolev wrote: "Given the increase in capital levels from recent transactions, many investors were wondering why SOFI had not changed its stance on ramping loan growth. We were encouraged to hear that internal indicators are healthy, and that management is simply being prudent with personal loan growth amid less-upbeat external indicator reads (e.g. PCE, unemployment, consumer confidence, etc.)"

Earnings

About a month ago, SoFi reported Q1 GAAP EPS of $0.02 on revenue of $580.65M. These top and bottom-line results both beat consensus, while the revenue print reflected year-over-year growth of 26.2%.

New member additions amounted to 622K during that quarter, bringing total membership up to more than 8.1M individuals. This showed growth of almost 2.5M new members over 12 months.

Product additions for the quarter came to more than 989K, which took total products sold up to more than 11.8M, good for 38% year-over-year growth.

At that time, SoFi took full-year revenue guidance up to $2.39B to $2.43B, better than the $2.38B that Wall Street had expected at the time, and full-year GAAP EPS up to $0.08 to $0.09, above the $0.07 that Wall Street expected.

The second-quarter guidance was mildly problematic, which could be adding to recent weakness in the share price. For the current quarter, SoFi only saw revenue of $555M to $565M, with the Street at $590M. Even though the full-year forecast was made at the same time, this could be spooking a few investors, especially if they think that print might land on the light side.

Currently, when SoFi reports in late July, consensus is for GAAP EPS of $0.00 (not a surprise) on revenue of $565M, which would be at the top of the company's one range provided. That growth would be up 15% from the same period last year.

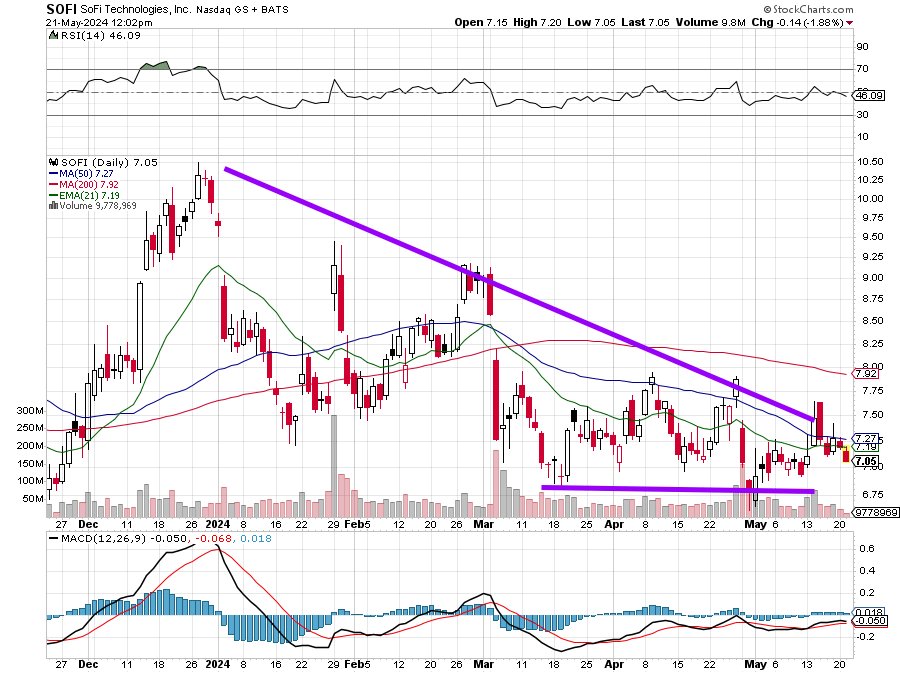

The Chart

Readers will see that SOFI has been trying to break out of a bearish descending triangle to the upside since late April. The stock has retaken and lost its own 50-day simple moving average (SMA) and 21-day exponential moving average (EMA), while relative strength remains on the low side of neutral. The daily Moving Average Convergence Divergence (MACD) has largely flatlined with the 12-day and 26-day EMA sort of wrestling for dominance. However, the histogram of the 9-day EMA has remained positive for more than a week now.

I am willing to add from here down to the $6.61 low of late April (I did add very close to that spot on that day). Should that spot crack, I would pause, but not panic.

For now, my pivot will remain the 200-day SMA at $7.92, which would put a temporary price target at $9.60. I would be down roughly 8% in the $6.40s, which is where I would consider lightening up if need be. That's if my average point of entry is not impacted too much as I add.

More Stocks Under $10:

- Sizing Up a Micro-Cap Biotech for a Speculative Play

- Time to Get Fired Up About Rocket Lab

- How Far Can This Low-Priced Silver Stock Rally?

At the time of publication, Guilfoyle was long SOFI equity.