Sizing Up a Micro-Cap Biotech for a Speculative Play

We won't have to wait too long for some idea on whether or not this stock has a chance.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Here's one you've probably never heard of.

On Monday morning, AC Immune SA ACIU released its first-quarter financial results. Just who is ACIU? The Lausanne, Switzerland-headquartered clinical-stage biotech focuses on precision medicine for neurodegenerative diseases. It designs, discovers, and develops therapeutic, and diagnostic products for the prevention, diagnosis, and treatment for diseases caused by misfolded proteins.

AC Immune's two technology platforms, SuperAntigen and Morphomer, are designed to create antibodies, small molecules and vaccines meant to address a wide variety of neurodegenerative indications. The company's pipeline includes nine therapeutic products with five currently in clinical trials and three diagnostic candidates. Its lead product has been Crenezumab, which is a humanized and monoclonal anti-Abeta antibody meant to treat Alzheimer's disease.

Earnings

AC Immune posted a Q1 GAAP loss of $0.18 per share on no revenue. The loss per share missed expectations by three cents. The lack of revenue for the quarter was flat from the year-ago comparison. The company did generate $17.6M in revenue for the December quarter thanks almost entirely to a contract related to clinical trials being run for/with the Janssen subsidiary of Johnson & Johnson JNJ.

For the first quarter, operating expenses, including both administrative costs and R&D expenses, amounted to $20.068M (+14.2%), leaving (due to having generated no revenue an operating loss of $20.068M. After accounting for interest and other income and expenses, the GAAP net loss came to $17.862M (-0.2%), or a loss per share of $0.18 versus a loss of $0.21 for the year-ago period.

What Might Be...

Obviously, this micro-cap biotech is not about what is, but about what might be instead. Very importantly, AC Immune has already announced a deal with Takeda TAK for ACI-24.060 with $100M upfront and total potential payments for options exercised and milestones net of up to $2.1B.

ACI-24.060 is currently in Phase 2 trials that should report Abeta-PET imaging results in Q2 2024, evaluating amyloid plaque reduction after six months of active immunotherapy. This is meant ultimately, if all goes well, to end up treating Alzheimer's patients.

Another candidate in the news is ACI-7104 VacSyn, which is in Phase 2 trials for potentially treating Parkinson's disease. This trial should produce results by H2 2024.

Balance Sheet (in Swiss Francs)

AC Immune has on its books, CHF 74.821M with current assets at CHF 109.873M and current liabilities of CHF 14.124. That's good enough for a current ratio of 7.78, which is exceptional.

Total assets amount to CHF 167.281M, including intangible assets of CHF 50.416M. At roughly 30% of total assets, this is enough to keep an eye on, but should not yet be enough to be an issue. Total liabilities less equity comes to CHF 22.6M. There is no debt on this balance sheet.

With the above-mentioned infusions of cash, and potential milestones met going forward, the company sees a three-year cash runway, even without contribution from the commercialization of any of its product candidates.

My Thoughts

Obviously, AC Immune is a prospect for pure speculation. However, I do not think we'll have to wait too long for some idea on whether or not this stock has a chance.

I like the balance sheet. By Q2, we should see either good news or bad news regarding the company's top candidate. They do have a nice cash runway that will have a chance to grow exponentially if a few things break their way.

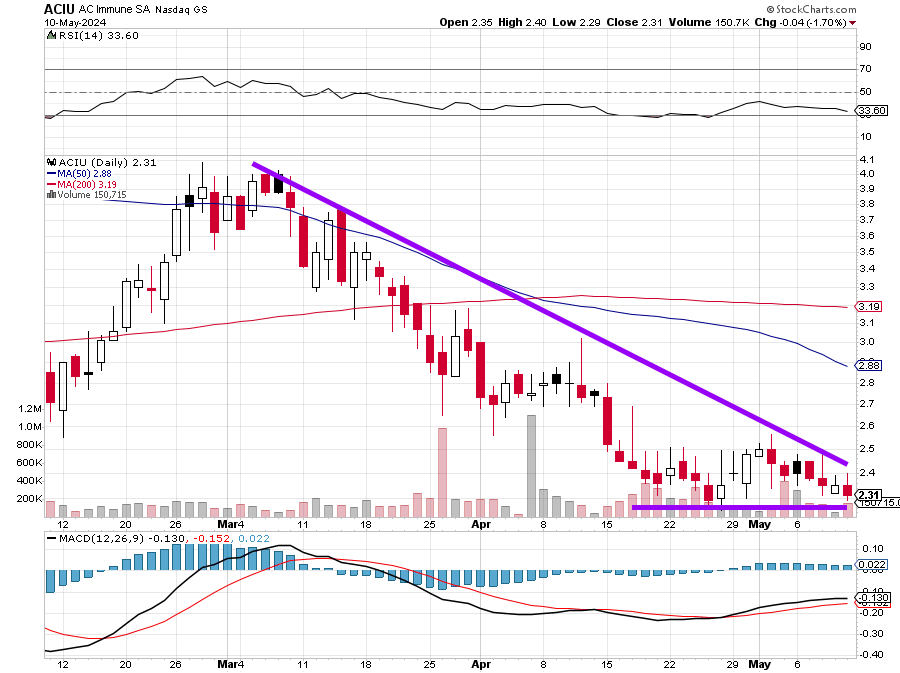

Looking at the chart, above, we have a mini-descending triangle, which can be a bearish technical chart pattern. Am I tempted to initiate a small long position down here? Very much so. We'll see where the stock is trading after this article goes public.

I would take an inability to hold the $2.25 level post-earnings as decisively negative. However, the stock has been trading higher ahead of the opening bell while I have been writing. I now see a last sale of about $3.50. No, I will not be paying up 50% for this issue.

That said, I might see where $5 calls and $2.50 puts expiring in June and August are trading after the open. If it makes sense, I would, perhaps use sales of both, to discount an equity purchase. If the discount is there, I think it may be worth capping profitability and increasing equity risk at a lower price point over time.

(Please note that due to factors including low market capitalization and/or insufficient public float, we consider ACIU to be a small-cap stock. You should be aware that such stocks are subject to more risk than stocks of larger companies, including greater volatility, lower liquidity and less publicly available information, and that postings such as this one can have an effect on their stock prices.)

At the time of publication, Guilfoyle had no positions in any securities mentioned.