Put Your Chips on Taiwan Semiconductor? Here's How to Trade It

Taiwan Semiconductor is a cash flow beast, and the balance sheet is rock solid.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

I wouldn't call it good news. Last Tuesday, Intel INTC came clean about declining sales, huge operating losses in that firm's foundry business and just how long the path to profitability probably is. That certainly was not good news for Intel. The stock gave up more than 12% last week.

The American depository receipts of Taiwan Semiconductor TSM, the largest foundry by far in the world were up 3.9% for the week in comparison.

It was not just bad news at Intel that could be taken as good news for Taiwan Semiconductor. A day later, on Wednesday, a 7.4 magnitude earthquake shook Taiwan, largely leaving the area where Taiwan Semiconductor operates, undamaged.

By later that day, Nvidia NVDA had announced that it did not expect disruptions in the supply and production of its processors. Nvidia designs high-end GPUs and other chips for generative AI, data center, and gaming applications. Taiwan Semi is Nvidia's contract manufacturer. Taiwan Semi does similar work for Apple AAPL, and Nvidia competitor Advanced Micro Devices AMD, among others.

New News

This (Monday) morning, the federal government has signed a tentative agreement with Taiwan Semiconductor to provide TSM with up to $6.6B in grants and as much as another $5B in loans in order to boost the manufacture of advanced semiconductor chips on US soil.

The US Department of Commerce, headed by Commerce Secretary Gina Raimondo (whom I believe to be the sharpest member of the current administration) officially signed what is still a "non-binding" preliminary memorandum of terms under the CHIPS and Science Act with TSMC Arizona, which is what Taiwan Semi's US operation is known as. TSMC Arizona, as a domestic US foundry, will have three semiconductor fabrication facilities in that area.

Several firms are receiving funding under that Chips act. The above-mentioned Intel has signed an agreement for roughly $20B in grants and loans, while Samsung Electronics SSNLF is expected to receive awards of about $6B.

As the firm sees it, their first facility in Arizona is on track to begin production using 4nm (nanometer) technology at some point in the first half of 2025. 4nm chips are still considered to be cutting edge. A second fab center will produce what is becoming the world's most advanced 2nm processors in addition to 3nm technology. That facility should be operating by 2028. The third fab center will also manufacture 2nm or more advanced processors if more advanced processors exist by the time the plant starts producing by the end of this decade.

The construction of these facilities is expected to create more than 25,000 jobs directly with more created in support of those jobs. The facilities themselves are projected to create a rough 6K high-tech, high-wage, permanent positions.

Earnings

Taiwan Semiconductor will report the firm's first quarter financial results on April 18. In US dollars, the firm is seen earning about $1.32 per share on revenue of $18B. These numbers would be in line with the year ago earnings print, while being good for year over year revenue growth of 7.8%. Remember, that in Taiwan Semiconductor's home market, these earnings are reported in New Taiwan Dollars and then converted for our purposes into US dollars. One US dollar is currently equal to about 32 New Taiwan Dollars.

Three months ago, when reporting the firm's Q4 results that beat expectations for both the top and bottom lines, the firm guided towards full year 2024 revenue growth in the low to mid 20% 's range. For the quarter about to be reported, the firm guided towards revenue of $18B to $18.8B.

With the consensus for exactly $18B and growth of less than 8%, is there a chance that Taiwan Semi disappoints, or has the bar been lowered enough for an upside surprise that really falls within the original outlook?

Of course, we will be waiting not just to hear some refinement concerning that guidance, but also perhaps some more detail on the implementation and timing of the firm's plans in Arizona.

Fundamentals

Taiwan Semiconductor is a cash flow beast, producing $40.457B in operating cash flows over the trailing twelve months as of that last (Q4) report, as well as $9.517B in free cash flow after accounting for capital expenditures.

As of December, the firm did have $31.6B in long-term debt, of which nearly $1.2B will mature this year. Is that a lot? The firm had a cash position of just under $55B at the time, so not really. At that time, the firm's current ratio stood at a quite robust 2.40, and its quick ratio stood at 2.13. That's extremely strong in an inventory-focused business such as semiconductors. This balance sheet is rock solid.

My Thoughts

Taiwan is getting help to expand, and despite the efforts being made to compete in the space, Intel appears to be having trouble doing so. GlobalFoundries GFS remains well behind. As a fundamental analyst, I love the cash flows and the balance sheet. Now, time to take a look at the technicals.

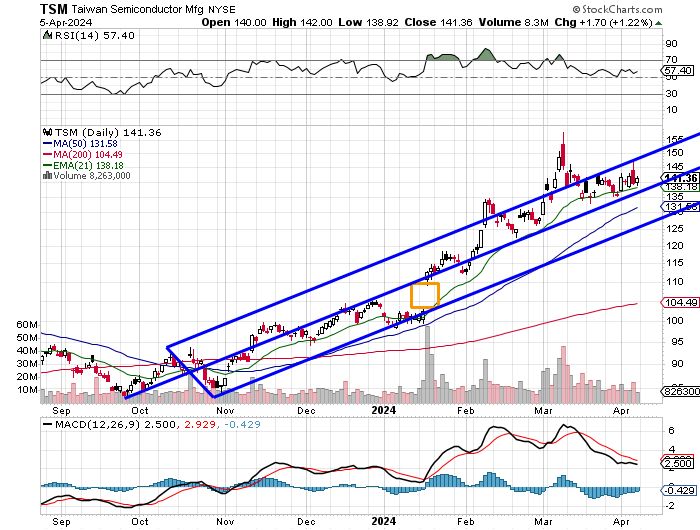

Readers will see that the stock is trying to break out of a Andres' Pitchfork model in place since last September. Despite an unfilled gap created back in January. Despite a mediocre reading for relative strength and a rather bearish looking daily MACD (moving average convergence divergence).

Still, the ADRs ride their 21-day EMA (exponential moving average), which is well above their 50-day SMA (simple moving average) and way, way above their 200-day SMA. So, what's with the mixed messages? I have an answer.

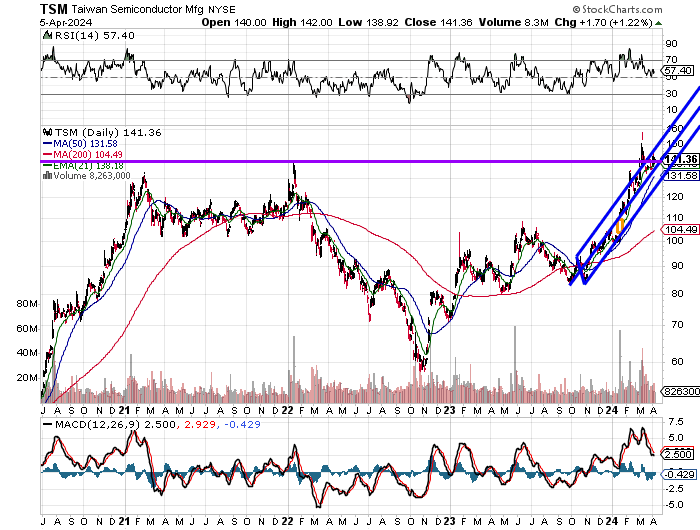

If we go way back to 2021/2022, we see that TSM developed a "double-top" reversal that worked like a charm, apexing twice in the neighborhood it now finds itself trading in. Sure, the level has been pierced a couple of times from below but has failed to take and hold that level in a sustained way.

That said, TSM closed above that $140 pivot on Friday. I am not in this stock, I mean ADR right now, but it has my attention. If the pivot holds through the inflation data this week, I can see TSM trading as high as $161 or even $169 if the whole semiconductor group gets on a roll and tries to make up for last week. Fail here? Then TSM is probably looking for a date with its 50-day line.

The ADRs were trading with a $144 handle in early trading. I don't want to chase on a gap-up opening. I would not be opposed to going out two months and selling $135 and/or $130 puts expiring on June 21st, should they still pay $4 to $6 worth of premium.

At the time of publication, Stephen Guilfoyle was long NVDA, AMD equity.