Own One of America’s Premier Growth Companies at a Bargain Price

You can now buy this top-quality, proven left-to-right grower, at much less than the market multiple of far inferior companies.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

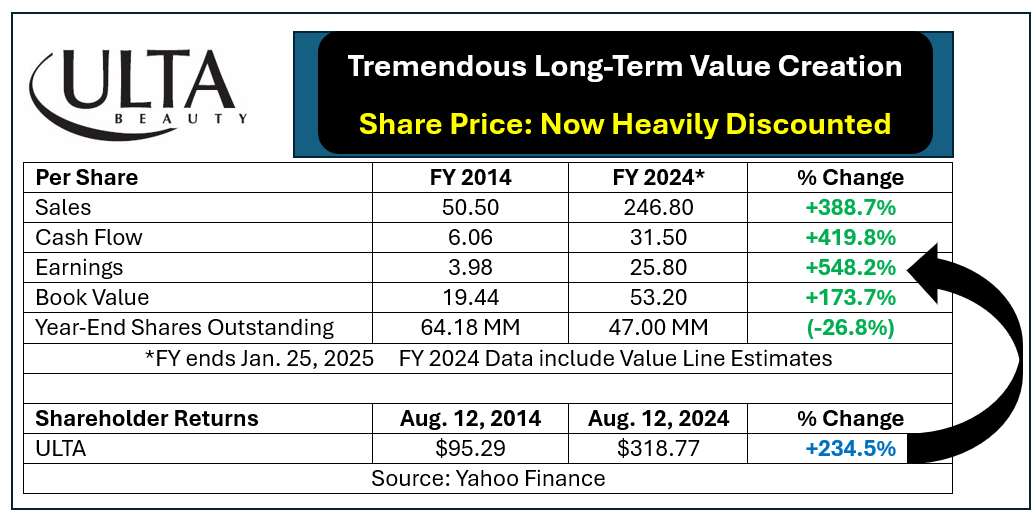

Ulta Beauty ULTA has a decade-long growth record that few firms can match. Details are provided below.

What is most notable is that the +234.5% shareholder return represents a greater-than-57% discount to its cumulative EPS growth.

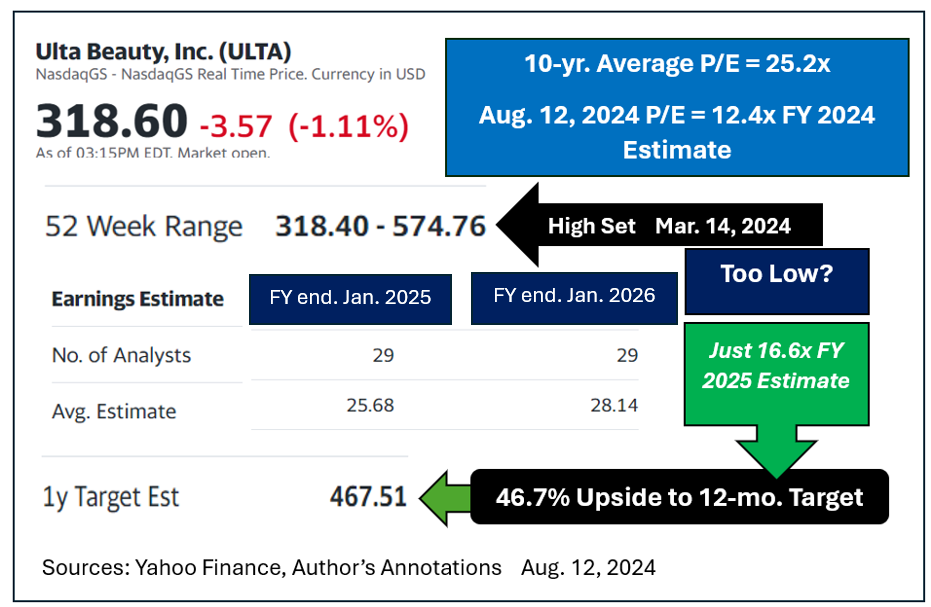

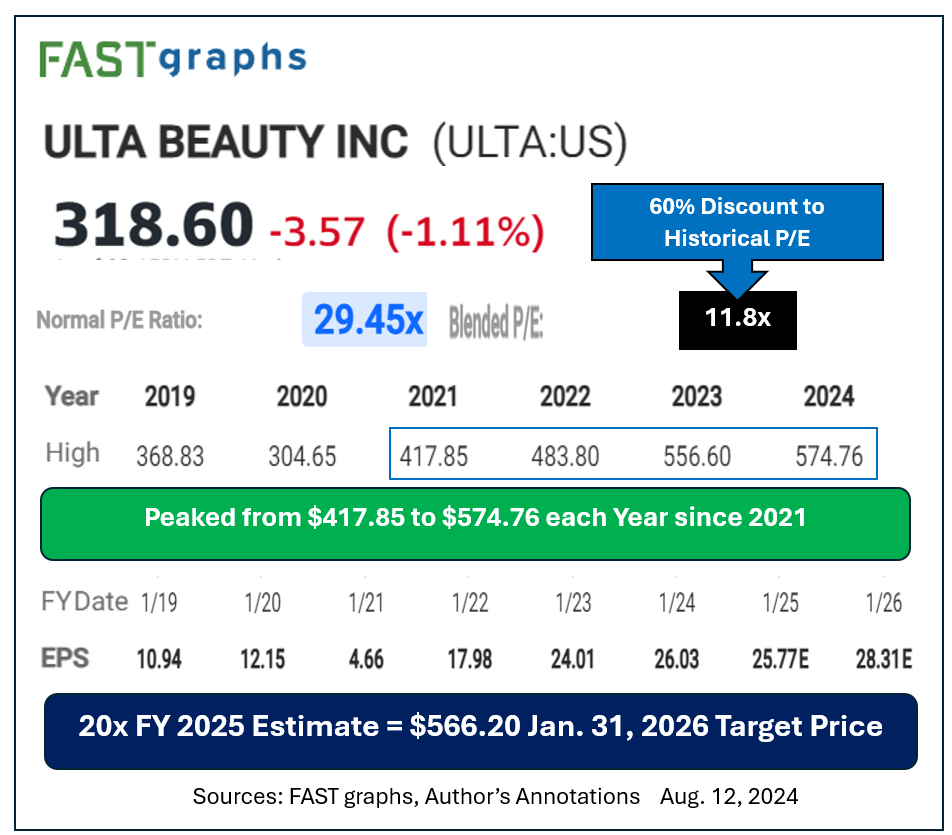

The only way that can happen is through P/E compression. ULTA’s current multiple sits at just 12.4x its FY 2024 estimate (FY ends Jan. 25, 2025) versus a 10-year average P/E of 25.2x.

That means you can now own this top-quality, proven left-to-right grower, at much less than the market multiple of far inferior companies.

ULTA has a higher-than-average Beta (volatility quotient). That is a positive thing when you are getting in near multi-year lows. The shares can rebound very quickly once the mood improves.

What Is ULTA Worth?

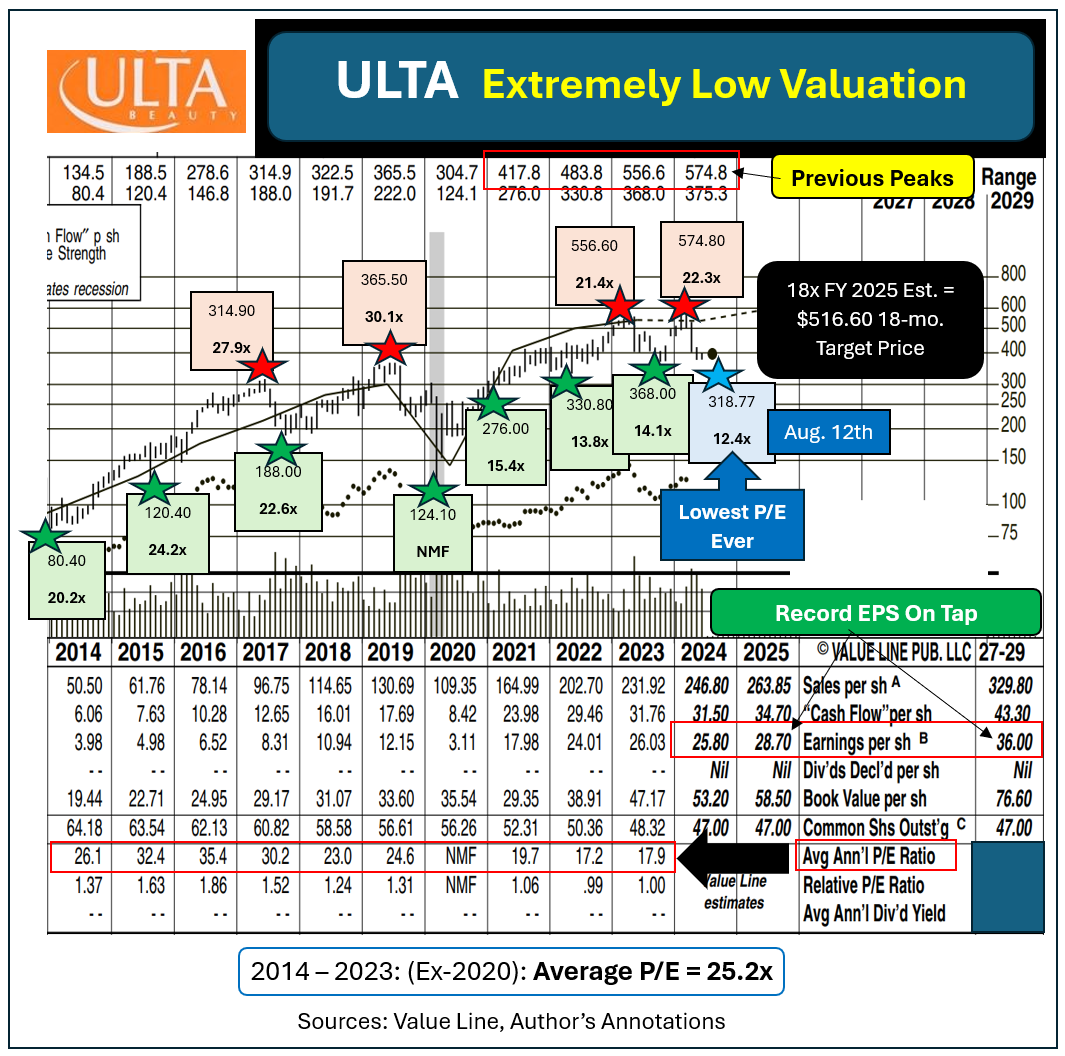

Assume that the shares do not regain their old 25.2x average P/E but only command about 18x forward earnings. Based on that very conservative view ULTA could easily bounce back to about $517 per share by January 2026. That implies greater-than-62% upside from its Aug. 12, 2024 quote.

That price target is far from an upper limit, however. ULTA topped out at $556.80 during May 2023 and at north of $574 in March of this year.

Previous “best buying opportunities” (green-starred below) came with ULTA at P/Es ranging from 13.8x to as high as 24.2x current year’s EPS. Each of those seven entry points led to large tradable rallies.

The stock’s four “should have sold” moments (red-starred) only kicked in with ULTA at from 21.4x to 30.1x earnings.

Do not simply accept my opinion on ULTA’s value.

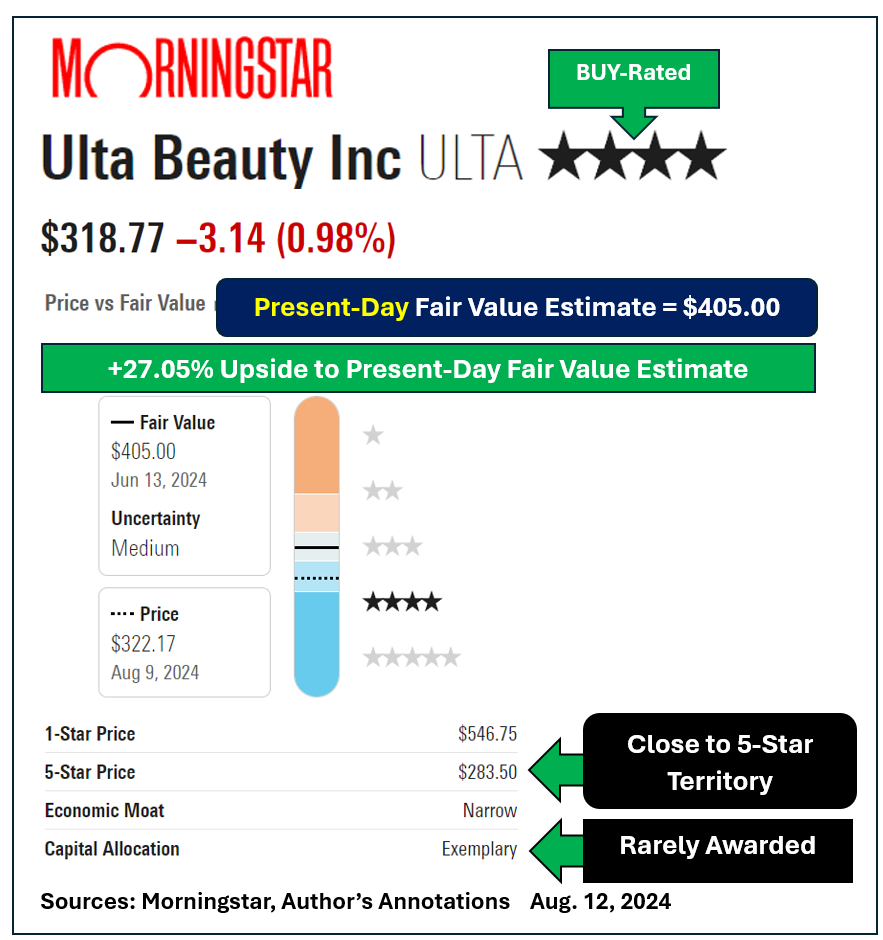

Research firm Morningstar rates the shares as a 4-star, out of five, BUY. It calls present-day, as opposed to year-ahead, fair value as $405 per share. That implies greater-than-27% upside is possible in short order.

A dip below $283.50 would put ULTA into Morningstar’s highest 5-star territory. Note, too, that Ulta earned the coveted “exemplary” rating for capital allocation decisions.

Yahoo Finance says ULTA now sells for less than half its normalized P/E. Its 12-month goal price of $467.51 is quite conservative at just 16.6x the company’s FY 2025 estimate. Even so, reaching that target would deliver almost +47% by this time next summer.

Quantitatively based FAST graphs notes ULTA peaked between $417.85 and $574.66 during each of the four years 2021-2024 YTD.

A regression-towards-the-mean 20x multiple on FY 2025’s EPS estimate suggests a Jan. 31, 2026 goal price of $566.20.

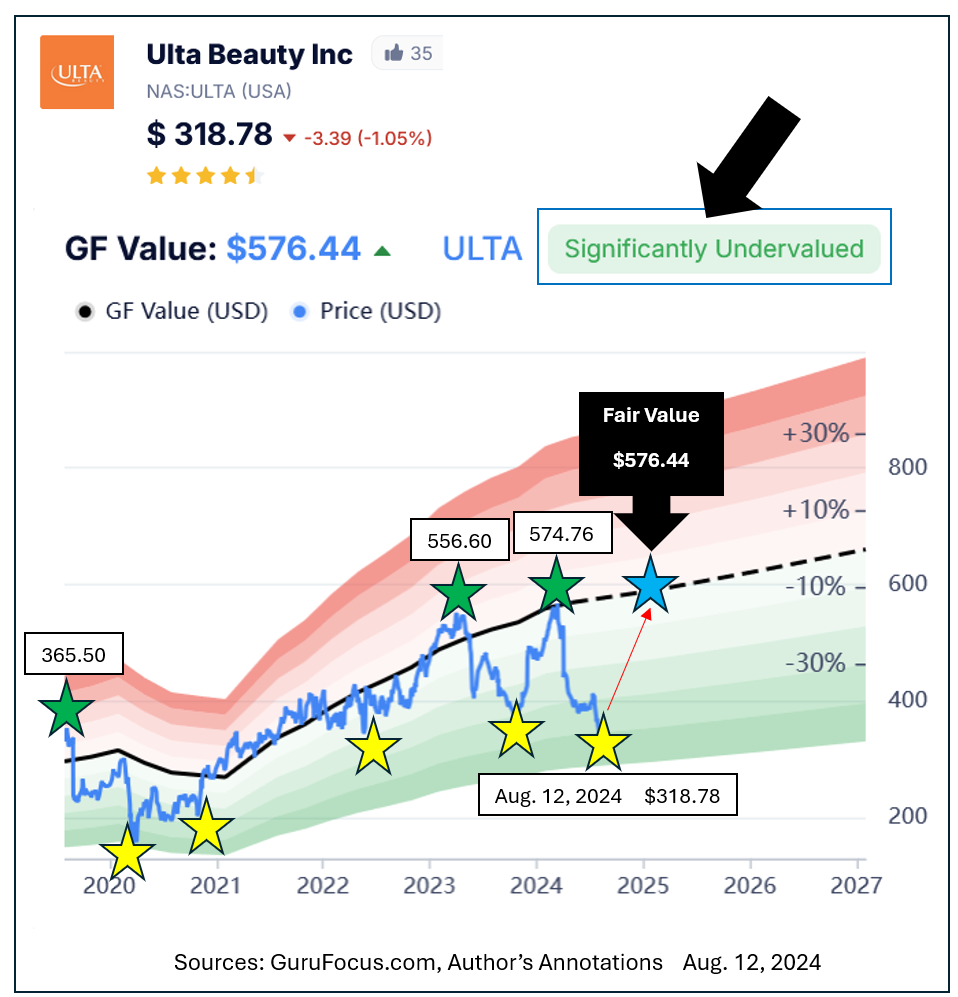

GuruFocus.com calls ULTA “significantly undervalued.”

Its targeted fair value price equals $576.44, just a tad above ULTA’s 2024 peak price. That implies upside of +80.8% from here.

Buying shares outright offers unlimited upside but requires about $31,900 of investment capital per each one hundred shares.

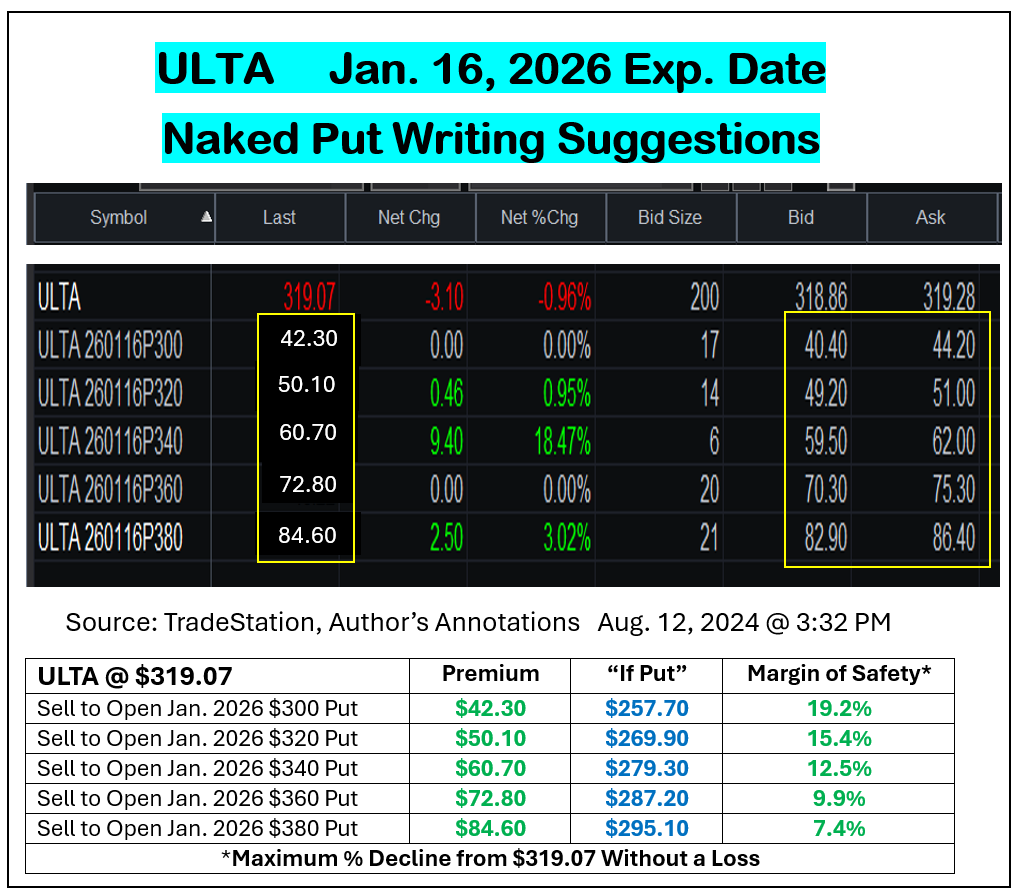

Option-savvy traders with the ability to short naked puts might also wish to sell naked puts on ULTA out to Jan. 16, 2026 expirations. Actual pricing on some of those, with ULTA at $319.07, is shown below.

I picked out the $300 to $380 strike prices as worst-case, forced purchase prices, running form $257.70 to $295.10, are all discounted to today’s already low price.

Maximum gains on these, or any other option sales always equals 100% of all premium dollars received upfront.

That runs from $4,230 (on the most conservative) $300 strike price to as high as $8,460 on the $380 strike if the option ultimately expires worthlessly.

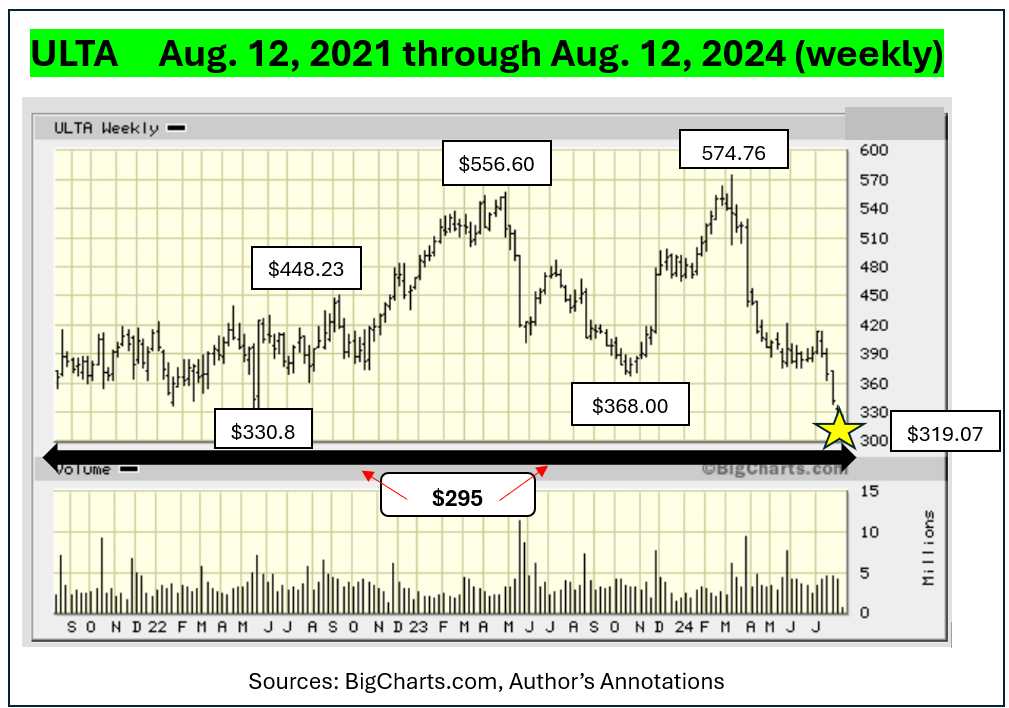

The three-year chart below shows that ULTA has not changed hands as low as even the most aggressive “if put” price shown above since well before August 2021.

The last time ULTA could be bought for as low as $295 was in February 2021, 3.5-years ago. It has not been available for under $276 since the Covid-panic year of 2020.

We all look back on times when great companies were “on sale” at terrific valuations, yet we failed to buy.

Bad momentum makes cowards of us all. Fight that very human emotion, though, and start building positions in ULTA. Your account statements will validate your decision later.

Buy some ULTA shares, short some LEAP puts, or consider doing both.

More Paul Price:

- Short-Term Variations Make Us Crazy. They Also Create Opportunities.

- Investing Is a Marathon. Trading Is a Sprint.

- Fun Facts That Help Investors Make Money

At the time of publication, Price was short ULTA Jan. 2026 puts.