New Oracle Price Target After Earnings Raise OpenAI Question

On Wednesday evening, tech giant/AI platform provider Oracle ($ORCL) released the firm’s fiscal fourth quarter financial results. For the three-month period ending May 31, Oracle posted an adjusted EPS of $2.11 (GAAP EPS: $1.45) on revenue of $19.184 billion. The top- and adjusted bottom-line results both beat the consensus view as that sales number was …

You've reached your free article limit

You've read 0 of 1 free Pro articles.

On Wednesday evening, tech giant/AI platform provider Oracle (ORCL) released the firm’s fiscal fourth quarter financial results. For the three-month period ending May 31, Oracle posted an adjusted EPS of $2.11 (GAAP EPS: $1.45) on revenue of $19.184 billion. The top- and adjusted bottom-line results both beat the consensus view as that sales number was good for year-over-year 20.6% growth.

The GAAP bottom-line number, however, fell just short of what Wall Street had in mind. Adjustments were made for restructuring costs, which is legitimate and for the purpose of stock-based compensation. Oracle went public in 1986. The fact that the firm is still not recording an expense they make every quarter 40 years later as an ordinary operating expense is just absurd. Just be straight with us, dudes.

Before we begin, readers should be fully aware that I have been critical of Oracle’s balance sheet in the past and have also been critical of the fact that the firm’s huge remaining performance obligation (RPO) never seems to turn into deferred revenues, which would make no sense if those orders were reliable.

I have had a negative take on ORCL since mid- to late 2025 and that opinion has proven itself worthy over that timeframe. The shares are down 47.7% from their $345.72 September 2025 high and have struggled even when other AI-focused names have performed well.

The Quarter Reported…

- Record Remaining Performance Obligations grew $85 billion from $553 billion to $638 billion

- Record Total Cloud Revenues of $9.9 billion, up 47% year over year

- Cloud Infra (IaaS) Revenue of $5.8 billion, up 93% year over year

- Cloud Apps (SaaS) Revenue of $4.1 billion, up 10% USD year over year

Guidance

For the current quarter, Oracle is looking for revenue growth of 27% to 29%. Total cloud revenue is seen at growth of 58% to 64%. Finally, adjusted EPS for the quarter is projected at $1.72 to $1.76, taking the low end of the range above the $1.69 that Wall Street was looking for.

For the full fiscal year just started, the firm sees total revenue of $90 billion, which was well above the $88.5 billion consensus view. This would produce an adjusted EPS projected at $8.05, which landed precisely upon consensus.

Fundamentals

For the quarter reported, Oracle generated operating cash flow of $31.977 billion. Out of that number came capex spending of $55.663 billion, leaving “free” cash flow of $23.686 billion. This was, for Oracle, the firm’s fifth consecutive quarter of cash burn.

Turning to the balance sheet, Oracle ended the period with a cash position of $31.894 billion, leaving the firm with current assets of $46.567 billion. Current liabilities add up to $41.764 billion. This includes short-term debt of $7.199 billion and deferred revenues of $9.916 billion. At the headline, the firm’s current ratio runs at 1.12. Adjusted for those deferred revenues, this ratio rises to 1.31 which, while not robust, does pass muster.

Total assets amount to $261.759 billion. Of that number, goodwill or other intangibles account for less than 24% which is not outlandish in 2026. Total liabilities less equity comes to $218.703 billion. Of that total, long-term debt comes to a whopping $122.342 billion. While I would not necessarily consider this an especially weak balance sheet, I don’t think anyone would marvel at its strength. Cash is burning and the debt load just keeps growing. Oracle cannot do what it has been doing indefinitely.

Opinion

The firm is profitable. That’s not in question. Should ORCL trade at 25-times forward looking earnings? That is a good question. The debt load is out of control. Cash flows seem to be, thanks to the AI up-spend, perpetually negative. The balance sheet is not super strong. Oh, and I have a question: If the firm has a remaining performance obligation of $638 billion, then how in the world are there only deferred revenues of $9.9 billion on the liability side of the balance sheet?

It is said that OpenAI accounts for more than 50% of that order backlog. If OpenAI is not putting any cash down on those orders, are they reliable?

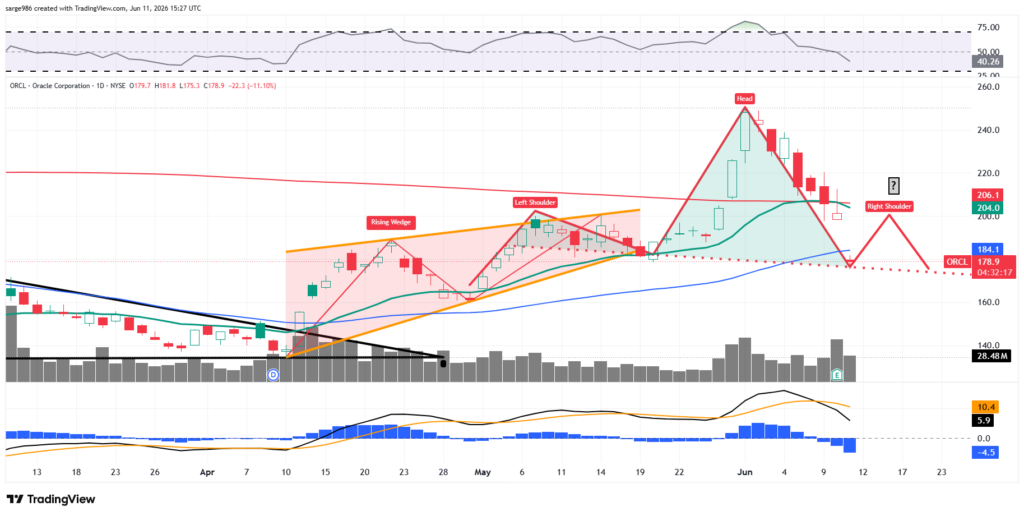

Readers will see that what had been a rising-wedge pattern morphed into a head-and-shoulders pattern of bearish reversal. Relative strength is below neutral while the stock’s daily MACD is postured quite negatively. If I were involved in ORCL, I would see the downside pivot at $176 and the target price at $160.

At the time of publication, Guilfoyle had no positions in any securities mentioned.