Micron Suddenly Expects a Big Increase in Chip Demand: Here's How to Play It

Generative AI applications are placing increased and accelerated demand on memory chip capacities.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Micron Technology MU reported its fiscal second quarter earnings that ended on February 29th back in mid-March. At that time, we wrote to you to inform readers that the firm had returned to profitability a quarter ahead of its own expectations.

For that three-month period, Micron posted an adjusted EPS of $0.42 (GAAP EPS: $0.71) on revenue of $5.824B. The adjusted EPS print just blew away expectations that were for a loss, while the sales number easily beat Wall Street, while reflecting robust year over year growth of 57.7%.

Why? Well, its generative AI, though that is not really what Micron does. Micron does memory, in fact... Micron is the dominant player in the memory ship space that had been oversupplied until just recently. What generative AI applications have done is place greatly increased and accelerated demand on memory chip capacities.

Micron is suddenly expecting to experience greatly increased demand for what are known as "high bandwidth memory" or HBM that combines with traditional DRAM chips to aid in the increase of processing speeds for the elite level GPU designer such as Nvidia NVDA and Advanced Micro Devices AMD.

This new pressure has resulted in aggressive pricing increases for both NAND and DRAM memory chips that have suddenly benefited as data center demand has created a scarcity that probably would have been difficult to comprehend only months ago. In fact, during that mid-March earnings call, Micron CEO Sanjay Mehrotra said that the firm's HBM supply has already sold out for this calendar year (2024) and that most of the firm's supply slated for calendar 2025 had already been allocated.

Readers may recall that Micron at that time had suffered through a period of negative free cash flow, but still ran with a strong balance sheet. A bit more long-term debt than I would like, but a balance sheet chock full of tangible strength, nonetheless.

Guidance

For the current quarter, Micron projected revenue generation of between $6.4B and $6.8B, which was well above the $6B or so that Wall Street had in mind at that time. Consensus is now up to $6.6B.

The firm also guided towards an adjusted gross margin of 25% to 28% and an adjusted EPS print of $0.38 to $0.52. This too was far better than the consensus view, which had been for about $0.20. Wall Street is now up to $0.47.

News

Overnight, in response to the news that Taiwan Semiconductor TSM would receive more than $11B in grants and loans from the CHIPS Act, and knowing that Intel INTC had already received cash, Citigroup five-star rated (at TipRanks) analyst wrote "Intel has already been granted $8.5B in cash so there is roughly $22B left in cash to be distributed in the CHIPs Act and we expect buy-rated Micron to receive a significant grant (>$5B) as well." Danely, as just mentioned, has a "buy" rating on MU with a $150 target price.

Elsewhere, Mizuho Securities five-star rated analyst Vijay Rakesh reiterated his buy ratings for direct Micron competitor Western Digital WDC and Seagate Technology STX. The analyst sees better demand for hard-disk drives out of China, which is good for Seagate, and flash memory prices rising.

Rakesh mentions that his team sees spot pricing for NAND memory up nearly 21% after hearing reports that Micron and Samsung SSNLF after the earthquake in Taiwan as the supply chain for these chips was already tight. By the way, Rakesh rates MU at a "buy" with a $130 target price.

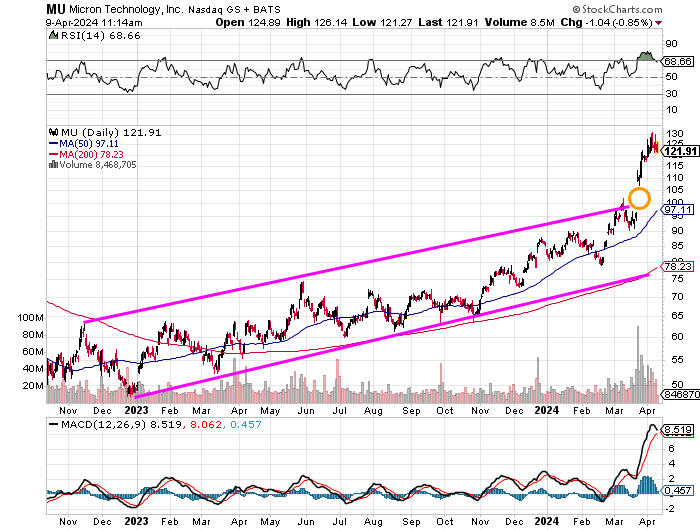

The Chart

Readers will see that Micron has clearly broken out from the ascending price channel that it had been in as a response to those earnings. Relative Strength is now technically overbought, as the daily MACD (moving average convergence divergence) appears to be set up for a bearish cross-under of the 26-day EMA (exponential moving average) by the 12-day EMA.

It would appear that much of this good news has already been priced in. That said, algorithms do have a mind of their own and do not walk away from making stupid trades the way humans used to. There will likely be upside even if briefly in response to a CHIPS Act announcement. Unless of course... the number disappoints.

I suggested patience in March, and I still do. Should markets get hit hard in response to the inflation data this week, or as earnings season gets under way, there remains that unfilled gap in the $90's beckoning. The stock needs to trade at $96 to fill that hole. I suggested selling some puts in March if one was hoping to get long and get paid to wait.

My thoughts at that time were to sell an April 19th $102 put for $1.15 and an April 19th put for about $0.30. The $102 put is now worth less than $0.10, and the $96 put is now worth less than $0.05.

Being that we are close to 100% profitability on those options shorts, these positions, if a trader indeed opened them, might as well be closed and the cash pocketed.

Micron will report on June 21st. A trader might consider reestablishing sales of a similar number of puts with those similar strike prices but with a May 24th expiration. Right now, the May 24th $105's are paying about $1.25, while the May 24th $95's are paying about $0.40. If it works, wash, rinse, repeat.

At the time of publication, Stephen Guilfoyle was long NVDA, AMD equity.