Lockheed Lives on the Cutting Edge of Defense: Here's How to Trade It

The balance sheet is solid, and cash flows are able to handle any changes in the environment. The guidance is close to spectacular.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The news had been warming up ahead of Q1 earnings. Of course, we speak of perhaps the greatest defense contractor of all-time, the firm living on the cutting edge of defending American interests and the interests of American allies globally.

We speak of Lockheed Martin LMT, a Sarge favorite, and arguably the longest tenured Sarge favorite at that. Two weeks ago, the US Department of Defense announced an up to $4.1B contract to Lockheed to develop, test, deliver and operate updates and new capabilities for the Command-and-Control Management and Communications system for the Missile Defense Agency.

Less than a week later, last week...the firm won another award, this one worth potentially $17B to develop the "Next Generation Interceptor" to modernize the ground-based network of radars, interceptors, and equipment designed to protect the US from intercontinental ballistic missiles.

That same day, JP Morgan five star rated (by TipRanks) analyst Seth Seifman upgraded LMT to "overweight" (buy-equivalent) from "neutral" (hold-equivalent), while increasing his target price to $518 from $475, despite acknowledging an uncertain production rate for the F-35 Lightning fighter aircraft going forward.

The Quarter

On Tuesday morning, Lockheed Martin released the firm's first quarter financial results.

For the three months ended March 31st, Lockheed posted an adjusted EPS of $6.33 (GAAP EPS: $6.39) on revenue of $17.195B. The adjusted earnings printed easily beat Wall Street, while the revenue number simply crushed the consensus view coming in by more than $1B, while reflecting year over year growth of 13.8%. The only adjustment made to these results was for $14M in mark to market investment gains, resulting in a GAAP EPS that was actually higher than the adjusted print.

Impressive

CEO Jim Taiclet commented in the press release: "First quarter sales increased significantly year-over-year and we generated robust free cash flow of nearly $1.3 billion, while taking assertive actions to further strengthen production capacity."

Taiclet added "Our $159 billion backlog includes several large National Security Space awards in the quarter and attests to the breadth of our portfolio, depth of our technical expertise, and understanding of our customers' needs. These capabilities uniquely position us to lead the realization of joint all domain operations, including reliable battle management and command and control systems integrated across multiple domains, military services, and allied forces."

Operations

As sales were growing 13.8% to $17.195B, the cost of those sales increased 16.2% to $15.202B. This left a gross profit of $1.993B (-2.6%) as gross margin dropped from 13.5% to 11.6%. After tacking on a small amount for "other" income and expenses, operating profit landed at $2.029B (-0.4%).

Finally, after accounting for interest, taxes and non-operating expenses, net income printed at $1.545B (-8.5%). Once share count is diluted, this works out to $6.39 per share versus the year ago comparison of $6.61.

Segment Performance

- Aeronautics generated revenue of $6.845B (+9.2%), while producing an operating profit of $679M (+0.6%) as operating margin dropped from 10.8% to 9.9%.

- Missiles and Fire Control generated revenue of $2.993B (+25.3%), while producing an operating profit of $311M (-17.5%) as operating margin dropped from 15.8% to 10.4%.

Rotary and Mission Systems generated revenue of $4.088B (+16.5%), while producing an operating profit of $430M (+22.9%) as operating margin improved from 10% to 10.5%.

Space generated revenue of $3.269B (+10.5%), while producing an operating profit of $325M (+16.1%) as operating margin improved from 9.5% to 9.9%.

Guidance

The firm reaffirmed the previously provided outlook for full year 2024. For the current year, Lockheed sees revenue generation of $68.5B to $70B. This is well above the $65B to $65.5B that Wall Street was looking for. Operating income is seen at $7.175B to $7.375B. After accounting for pension-related adjustments, diluted EPS is expected by the firm to land at $25.65 to $26.35. Wall Street was almost unanimously below $25 on this number. This has a lot to do with this morning's pre-opening pop in the price of the shares.

As far as cash flows are concerned, the firm is projecting full year operating cash flow of $7.75B to $8.05B, CapEx spending of roughly $1.75B, and free cash flow of $6B to $6.3B. As it always has been, this firm remains an absolute free cash flow producing beast.

Fundamentals

For the quarter reported, Lockheed produced operating cash flow of $1.635B, out of which came CapEx spending of $378M. This left free cash flow of $1.257B. Out of that number, Lockheed repurchased $1B worth of common stock for the firm's treasury, while returning $780M in cash dividends to shareholders. Yes, despite the strong cash flows, that's a lot to return to shareholders. I would prefer at least for now to see the repurchases slow down to the $500M or so that the firm was buying back a year ago.

Glancing at the balanced sheet, Lockheed ended the quarter with a cash position of $2.79B, inventories of $3.278B and current assets of $22.958B. Current liabilities add up to $17.699B that included almost no debt. That leaves the firm with a current ratio of 1.3 and a quick ratio of 1.11. These ratios do not knock the cover off of the ball, but they are more than adequate, especially for a huge industrial firm reliant upon carrying large inventories at all times.

Total assets amount to $54.963B including $12.94B in goodwill and intangibles. At 23.5% of total assets, this number is a long way from raising any alarms. Total liabilities less equity comes to $48.313B, including $19.25B in long-term debt. Speaking as a fan of the company, and an investor, I would prefer to see returns to shareholders reduced to something less than free cash flow. In fact, I would not mind if there was little in the way of repurchases, while the dividend is sustained, and the long-term debt-load was reduced. That's just me. I'm old school that way.

My Thoughts

There's a lot to like here. Earnings are strong, as are revenues. Margins came in a bit, but Lockheed did not deliver a single (lucrative) F-35 aircraft this past quarter. We do know that those deliveries will kick back up this year, even if the Biden administration plans to buy fewer of these fighters for US forces. Deliveries of F-16 fighters, C-130s (cargo/gunship) and helicopters all increase for the quarter on a year over year basis.

Best of all, the balance sheet is solid, at least in the present and cash flows are there to the point of being able to handle any changes in the environment. The guidance is close to spectacular. Though a reaffirmation, those numbers are well above what Wall Street had in mind.

Remember, back in March, the US Air Force disclosed that it had conducted the final test of an air-launched hypersonic weapon developed by Lockheed. Obviously, no information had been released about the results of that test. Though as far as we know a procurement order for such a weapon has not been placed, we do know that Lockheed had been working on defensive hypersonic weapons, which is what is desperately needed.

Easier to create an indefensible weapon than it is to create something that can actually intercept it. Our enemies are ahead of us on hypersonic offense. It would be nice to know that we are ahead of them on hypersonic defense. This stuff, I am sure, is classified and we won't know anything until there is actual news.

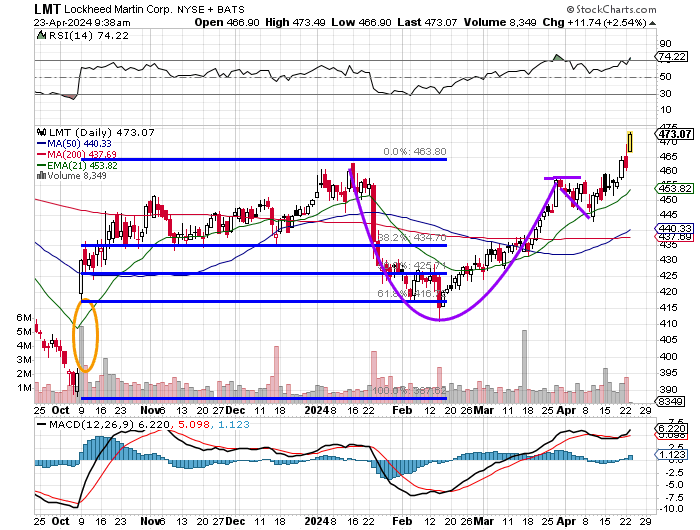

Readers will see that the stock found support at almost a perfect 61.8% Fibonacci retracement (in February) of the October through January rally. This morning, LMT continues the breakout that we had talked about a couple of weeks ago in Market Recon as well as in Doug's Diary. LMT had formed a cup pattern stretching from January into late March and then developed a handle. This created a $457 pivot. Off of that pivot, my target price stands at $525.

Relative strength is very strong. The daily MACD (moving average convergence divergence) is in excellent shape, bordering on becoming technically overbought. Readers will now see the "golden cross" that this stock experienced a few days ago. That's the 40-day SMA (simple moving average) rising above the 200-day SMA. I would expect significant support in that area at this time.

What that means is I believe that the stock can be brought down to the 50-day line, but the 200-day line, not far below... would serve as my panic point.

At the time of publication, Stephen Guilfoyle was long LMT equity.