Market Reversal, Capped Rally? Fed Talk, Big Bank Earnings, Trading Lockheed, Amazon

There does seem to be a more cautionary tale being told by the Fed at this point, which I believe is necessary.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

What is it that Doug Kass so often tries to teach us? Maybe that financial markets have no day-to-day memory. That's especially true since algorithms replaced human traders and since market structure was fractured to the point where individual stocks may be listed or domiciled at either the New York Stock Exchange or the Nasdaq Market Site, but outside of the official open and close of any given regular session, may trade anywhere.

Such a change in fortune was evident on Thursday. One day after a broad equity market beatdown that may have been overdone, but truly did occur for a good reason, equities, at least at the major index level ran to the upside.

What changed? On Wednesday, March consumer prices printed warmer than expected both month over month and year over year as well as at both the headline and the core. This backed up expectations for short-term rate cuts any time soon and left a major upside mark on both the US Treasury yield curve and US dollar versus the greenback's reserve currency peers.

The Why?

On Thursday, the difference was that producer prices for March printed on the cool side, but not across the board and not cooler than in February on a year over year basis. The March PPI crossed the tape at month over month growth of 0.2% at both the headline and the core. This was below expectations for 0.3% at the headline and in-line with core expectations.

On a year over year basis, March PPI printed at growth of 2.1%, up from 2.0% in February, but below consensus view for a 2.3% result. Core PPI was not cold. At the core, PPI hit the tape at growth of 2.4%, up from February's 2.1% print and above consensus view for a 2.3% print.

The fact that for markets CPI is far more important than PPI and that CPI was warmer than PPI was cool was lost on equity markets. Not all markets. Just equity markets. Treasuries were weak to mixed as a mediocre at best 30 Year Bond auction followed seriously weak auctions for both 10 Year and 3 Year Notes. By day's end on Thursday, the US Ten Year Note paid 4.58%, up four basis points, while the US Two Year Note paid 4.95%, down two basis points.

Treasuries have strengthened slightly overnight. The US Dollar Index held Wednesday's gains into Thursday and has added further gains overnight into Friday morning as there is now belief that the European Central Bank will beat the Federal Reserve to the starting line of any coming era of easier monetary policy.

As I scan Fed Fund futures markets trading in Chicago very early this morning, there is now a 51% probability for a 25-basis point rate cut as early as September 18th, which would be right in front of the national election in the US if that were to happen then. These markets currently show a 58% likelihood for as much as 50 basis points worth of short-term rate cuts during calendar 2024.

Rally Caps?

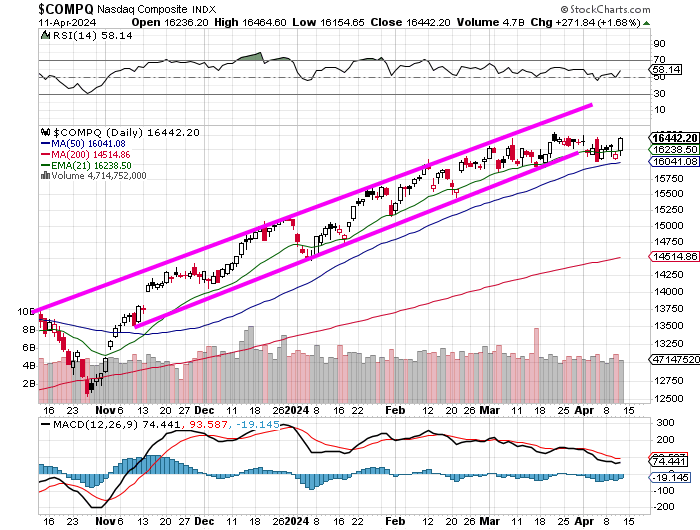

Or capped rally? The Nasdaq Composite closed at a record high level on Thursday, up 1.68% for the day as the S&P 500 gained 0.74%. I had told readers on Thursday morning that for Wednesday's markets to represent a change in trend to the downside, we would need to see a "follow-through" day and I preferred to see some space between the two selloffs.

Well, now we await a follow-through day, and it can be in either direction as the Nasdaq Composite broke through the lower trend line of its ascending price channel in early April...

... but has now regained its 21-day EMA (exponential moving average) and has traded in a narrow basing period of consolidation for almost a month. Relative strength has picked up, but the daily MACD (moving average convergence divergence) for this index remains bearishly postured with the 12-day EMA still below the 26-day EMA and the histogram of the 9-day EMA has below zero for literally all of March and April as well as most of February.

Small to midcap stocks failed to keep up with large-caps on Thursday, growth outperformed the pack for the day. Breadth was not nearly as strong on Thursday as it was weak on Wednesday. Only five of the eleven S&P sector SPDR ETFs showed gains on Thursday as Technology XLK led the way at +2%. No other fund among the eleven moved even a full percentage point. A day ahead of the kick-off of earnings season for the large banks, the Financials XLF backed up 0.71%, while the KBW Bank Index lost 0.76%.

Winners beat losers at the NYSE by the slimmest of margins and at the Nasdaq by about 5 to 4. Even more interesting, on an "up" day, advancing volume took a minority share (46.1%) of composite NYSE-listed trade, but a more optimistic 57.5% share of composite Nasdaq-listed trade.

Just as interesting and perhaps nullifying the significance of Thursday's rally, aggregate trade fell sharply on a day over day basis across the listings of both the NYSE and the Nasdaq and across the memberships of both the S&P 500 and the Nasdaq Composite.

The Fed Said...

There were several Fed speakers out and about on Thursday as there will be later today. There does seem to be a more cautionary tale being told at this point, which I believe is necessary.

"When we gain greater confidence that inflation is headed toward our target, then it'll be appropriate to ask whether it's not time to recalibrate the setting of monetary policy."

"What's happened over the last three months is we've seen elevated inflation, not nearly at the levels that it was at a year or two ago, but higher than our target."

- Richmond Fed Pres. Tom Barkin (Richmond has 2024 FOMC voting rights)

"There's no clear need to adjust policy in the very near term. As we collect more data, we'll be able to assess have we got (if we have) that confidence that inflation is moving back to 2%."

- New York Fed Pres. John Williams (NY has permanent FOMC voting rights)

"Incoming data have eased my concerns about an imminent need to reassess the stance of monetary policy. It may just take more time than previously thought for activity to moderate, and to see further progress in inflation returning durably to our target."

- Boston Fed Pres. Susan Collins (Boston does not vote for itself on policy until 2025 but may be called upon to vote in Cleveland's place once Cleveland Fed Pres. Loretta Meester retires in June.)

Here Come the Banks

Earnings season is upon us and here come the large banks. As readers can see below, JP Morgan JPM, Citigroup C and Wells Fargo WFC will bat at the top of the order. Roughly 50% of all S&P 500 companies reporting between this morning and next Friday will come from the financial sector. According to FactSet, for the first quarter, the Financials as a sector are expected to post year over year earnings growth of 0.7% on revenue growth of 3.3%.

However, there is a great disparity across industries within the sector. Earnings growth across insurance companies is seen at a whopping 37%. I am sure you've all seen your premiums for this year. On the other end of the spectrum (sticking with data provided by FactSet), the banks are seen posting earnings "growth" of -18%. When isolated, regional banks are seen posting earnings "growth" of -28%.

Very interestingly, the financial sector ex-insurance would be expected to post earnings "growth" of -6%, while the financial sector ex-financial banks would be looking at earnings growth of 14.2%.

Such a Deal

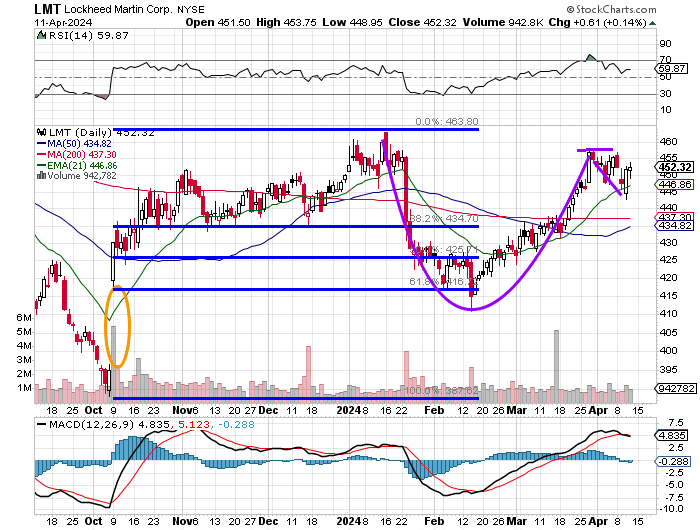

News broke on Thursday that the Department of Defense had awarded a contract worth as much as $4.1B to Lockheed Martin LMT. The firm will be paid to develop, test, deliver, and help operate updates and new capabilities for the "Command and Control, Battle Management and Communications System" or as it is affectionately known... the C2BMC for the Missile Control Agency. Yes, my friends, we have come a long way from caking ourselves in disgusting, smelly mud to both protect ourselves from insects and cover our scent, or from patrolling in streams and brooks to prevent ourselves from being tracked.

Readers will see that LMT caught itself almost perfectly in February at nearly a 61.8% Fibonacci retracement of the October through January rally. Moving to the present, LMT has formed a cup pattern from January into late March and has now developed a handle. This creates a $457 pivot and if that pivot can be taken after the stock found support at its 21-day EMA, my target price will become $525.

'Cuz The Weasel Goes Pop!!

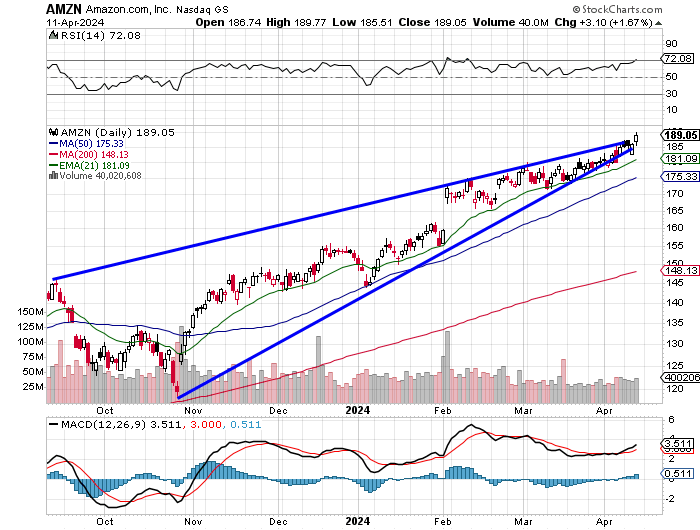

Amazon AMZN closed at a record high level of $189.05 on Thursday afternoon. We have repeatedly shown an ascending narrowing wedge where the higher lows have been gaining on the higher highs for this stock for quite some time now. The whole way, we have expressed our view that a coming period of volatility, perhaps an upside break, would follow the closing of that six month "pennant."

This appears to potentially be occurring in the present with the share price lurching forward as both relative strength and the daily MACD appear to be postured bullishly. This puts my pivot for AMZN at $187 and the target, conservatively at $215.

Economics (All Times Eastern)

08:30 - Export Prices (Mar): Expecting 0.5% m/m, Last 0.8% m/m.

08:30 - Import Prices (Mar): Expecting 0.4% m/m, Last 0.3% m/m.

10:00 - U of M Consumer Sentiment (Apr-adv): Expecting 79.0, Last 79.4.

10:00 - U of M One Year Inflation Expectations (Apr-adv): Expecting 2.8%, Last 2.9%.

10:00 - U of M Five Year Inflation Expectations (Apr-adv): Expecting 2.8%, Last 2.8%.

13:00 - Baker Hughes Total Rig Count (Weekly): Last 620.

13:00 - Baker Hughes Oil Rig Count (Weekly): Last 508.

The Fed (All Times Eastern)

14:30 - Speaker: Atlanta Fed Pres. Raphael Bostic.

15:30 - Speaker: San Francisco Fed Pres. Mary Daly.

Today's Earnings Highlights (Consensus EPS Expectations)

Before the Open: BLK (9.38), C (1.30), JPM (4.13), STT (1.52), WFC (1.09)

At the time of publication, Stephen Guilfoyle was long WFC, LMT, AMZN equity.