Cava Could Stick a Fork in Your Portfolio

This stock's valuation is burnt to a crisp, so if own it, here's what to do. If you don't, you've been warned.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

When an already expensive stock leaps almost 75% in 18-days you need to be careful not to fall in love with those shares.

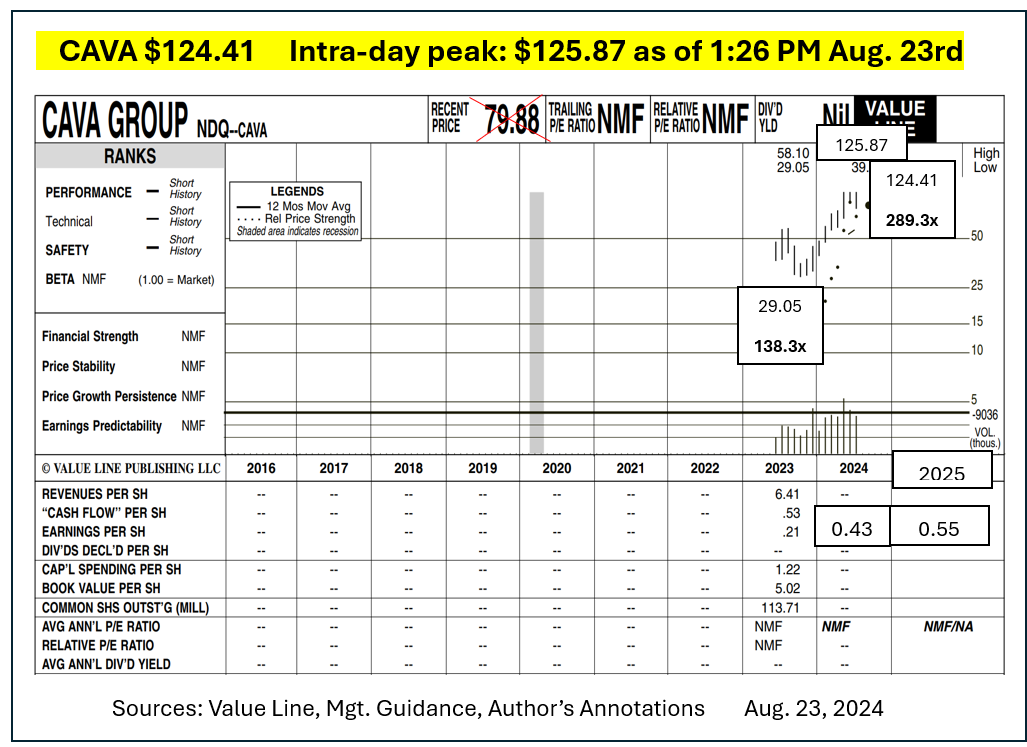

Sure, Cava Group's CAVA latest quarterly report showed better-than-expected sales and earnings. The absolute earnings per share, though, were just 17 cents and the first half total was 29 cents. Last year's second half was noticeably weaker than the first half due to seasonality.

Knowing that analyst views for the full year 2024 now are focused on 43 cents, up from 34 cents following last week’s earnings beat, 2025 earnings per share are currently penciled in at about 55 cents.

If those prove accurate, CAVA’s mid-afternoon quote of $124.41 last Friday equaled 289.3-times this year’s, and 226.2-times its 2025, EPS estimate.

Smart holders of Cava shares should be selling, rather than buying shares while the glow of almost unthinkable momentum is still shining brightly.

Why do I say that?

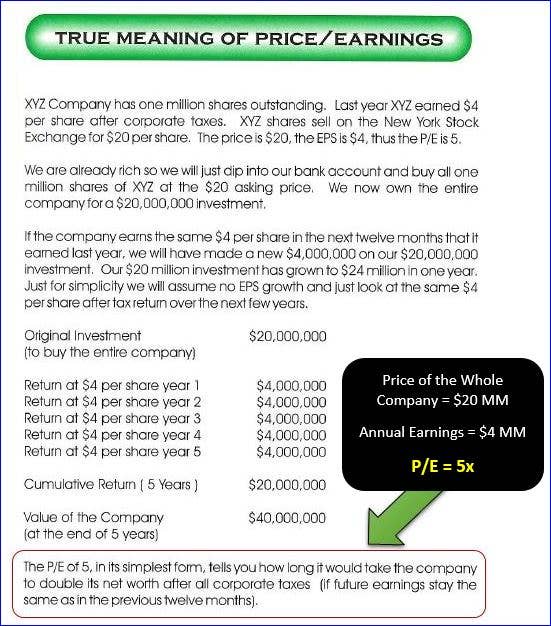

I’ve written before about the true meaning of price-to-earnings (P/E) ratios. My graphic illustrating that is shown below.

CAVA is showing solid growth, though, and deserves a higher than market P/E. The question becomes, "How high is too high to stomach?"

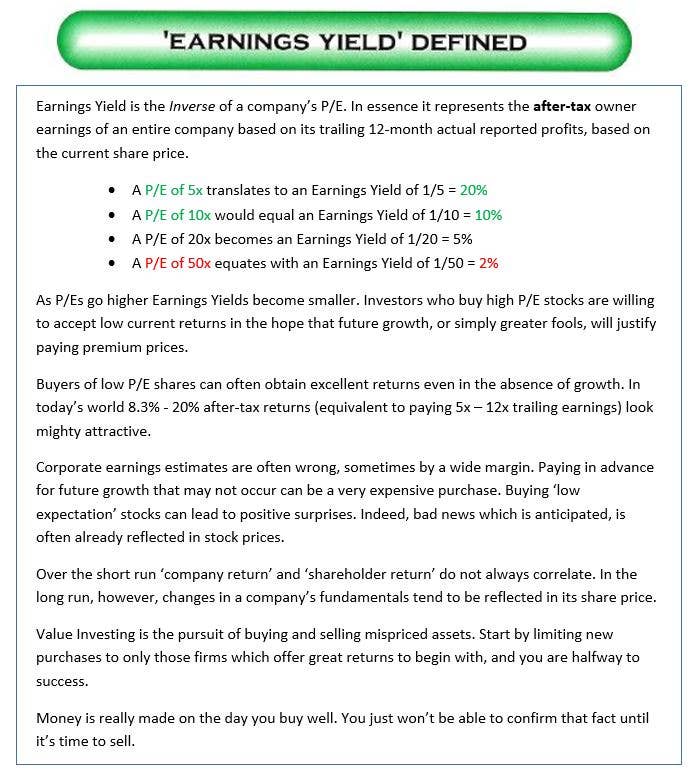

I noted that CAVA was selling for 289-times and 226-times forward 2024 and 2025 earnings. That means today’s shareholders are getting extremely puny real returns on “owner earnings.” That term comes from the reciprocal of the P/E and is also called earnings yield.

Based on the 27.9% year-over-year improvement in EPS expected next year (to 55-cents) shareholders should only expect to pocket 0.044% on shareholder equity in 2025.

It appears valuation is now way too rich to be sustainable.

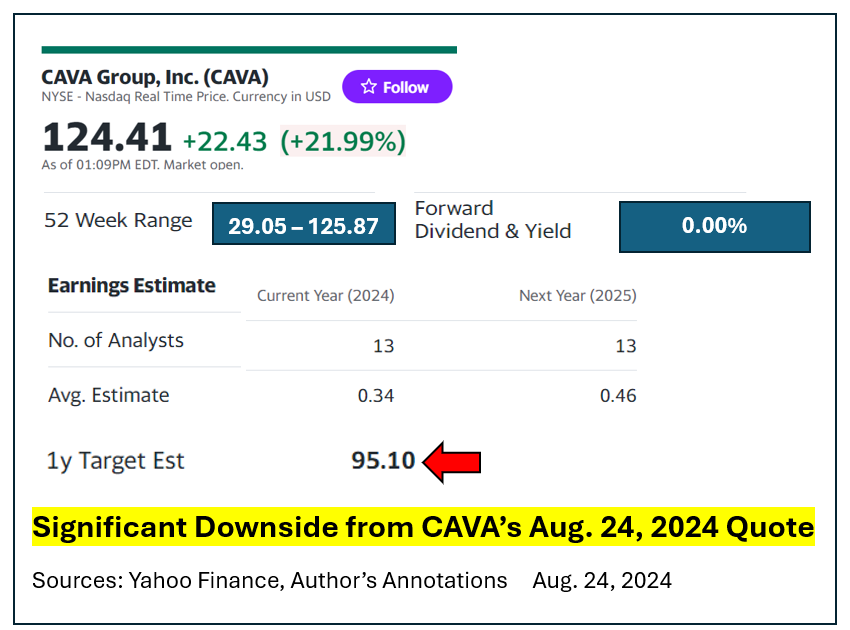

I am not the only one seeing this. Yahoo Finance carried a 12-month target price for CAVA at $95.10. That implied almost 24% of year-ahead downside from last Friday’s price. It also aggressively assumed that Cava would still command about 173-times the newly raised 2025 EPS estimate.

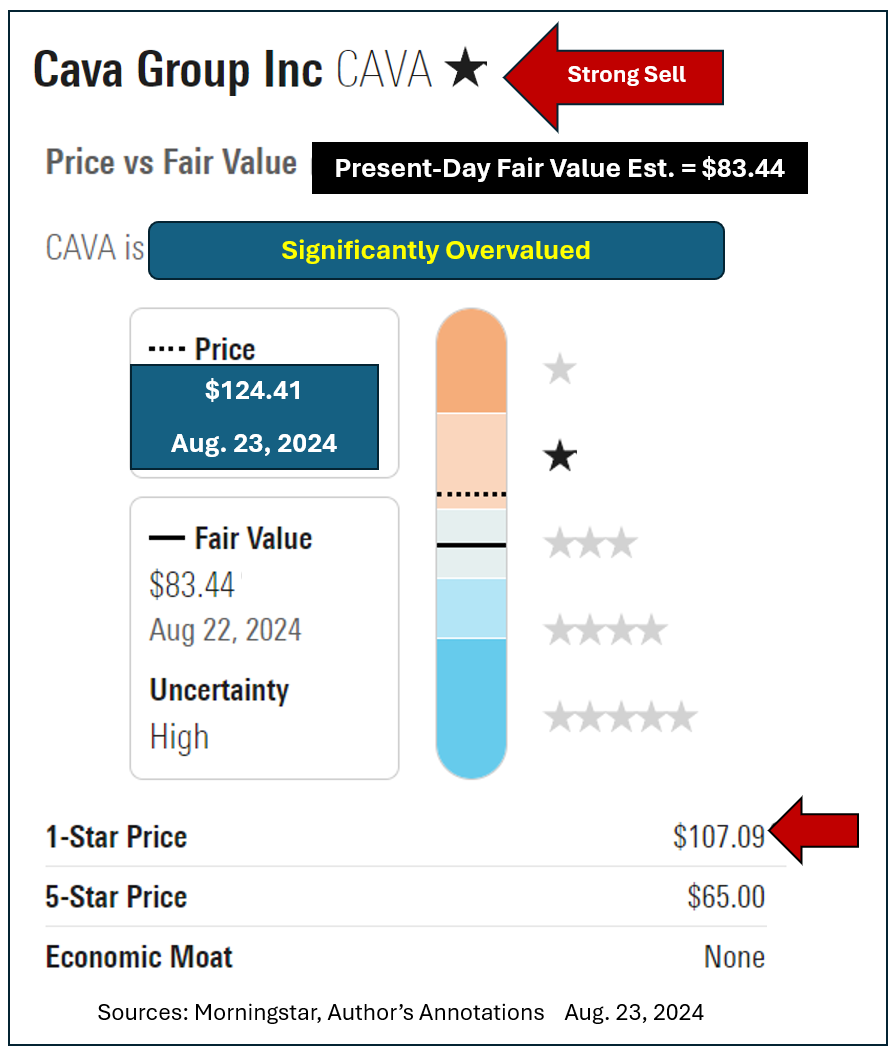

Independent research from Morningstar labels CAVA as a one-star out of five strong sell. Any price above $107.09 would have earned that inglorious rating. CAVA is now far above the super-rich valuation needed to qualify.

Downside risk to Morningstar’s $83.44 present-day fair value estimate equaled about 33% from its $124.41 quote. As with Yahoo Finance even that fair value assessment implies CAVA is worth 151.7-times next year’s already upwardly adjusted 55-cent estimate for 2025.

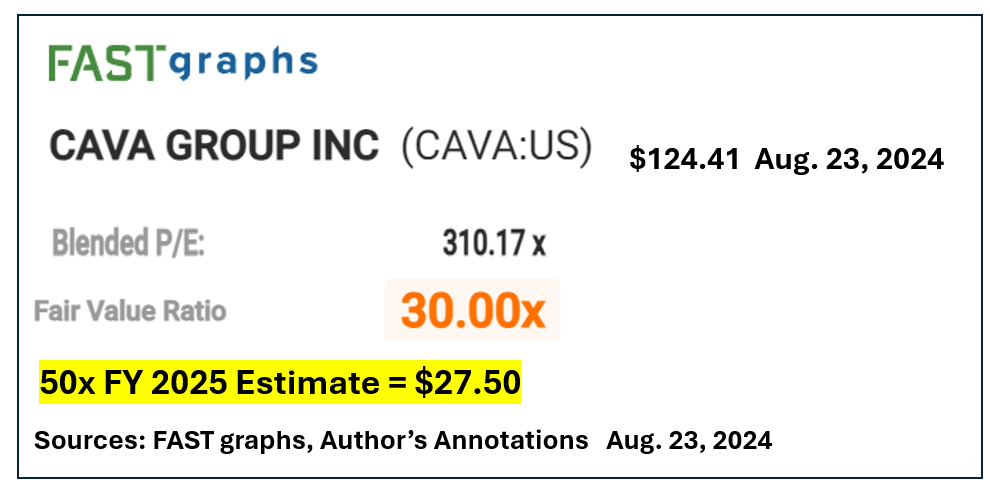

Quantitatively based Fast graphs is only willing to call Cava's fair multiple as 30-times.

Generously applying a 50-times multiple to next year’s estimate generates an 18-month target price that seems laughably low at present. Buying at the current price, though, appears to offer significant risk with only a hint, if any, of potential upside.

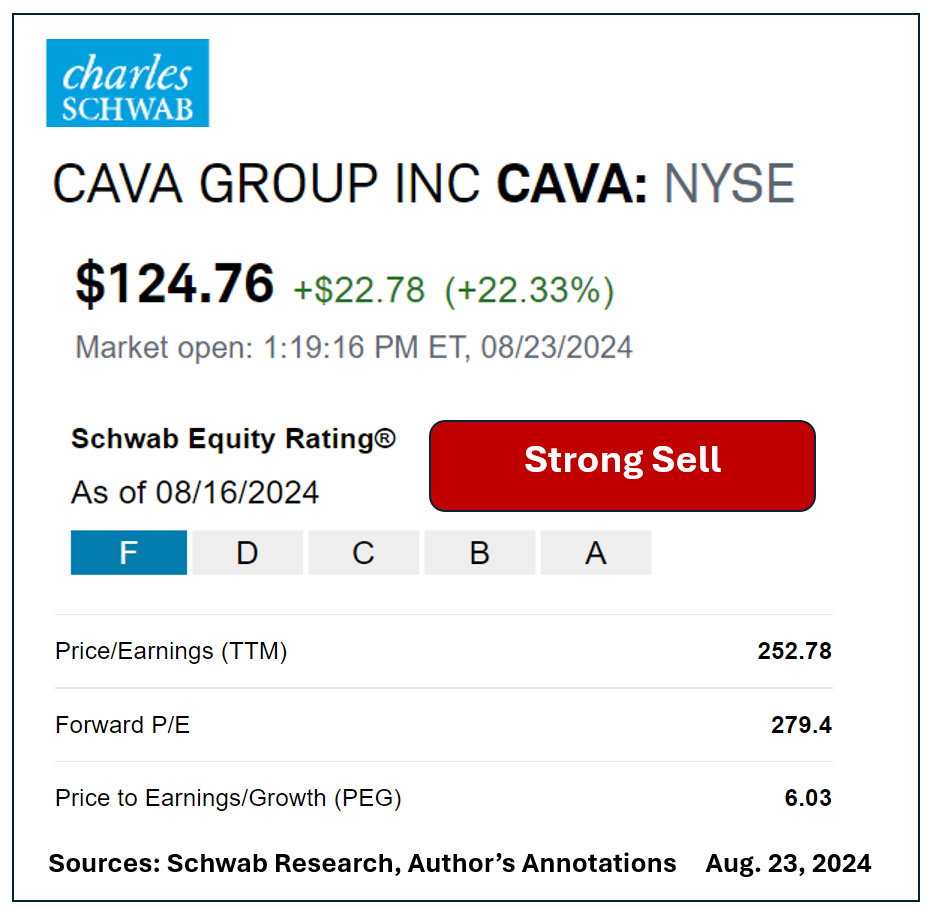

Charles Schwab’s research panel called CAVA’s equity rating as an “F” (strongest sell).

P/Es based on 2024 and 2025 look ridiculously high. So does the company’s PEG ratio of greater than 6-times.

Other than extremely strong momentum based on hyper-enthusiastic media coverage there is no reason to want to own Cava near today’s price.

If you own it, lock in gains. If you don’t own it, fight the urge to get onboard after the stock’s extraordinary run-up.

If you choose to hold or buy … do not say you were not warned.

More Paul Price:

- Short-Term Variations Make Us Crazy. They Also Create Opportunities.

- Investing Is a Marathon. Trading Is a Sprint.

- Fun Facts That Help Investors Make Money

At the time of publication, Price had no position in any security mentioned.