Why We’re Staying on the Sidelines as This Housing Play Comes Under Pressure

There's a risk we see on top of D.R. Horton’s soft 2025 delivery guidance.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

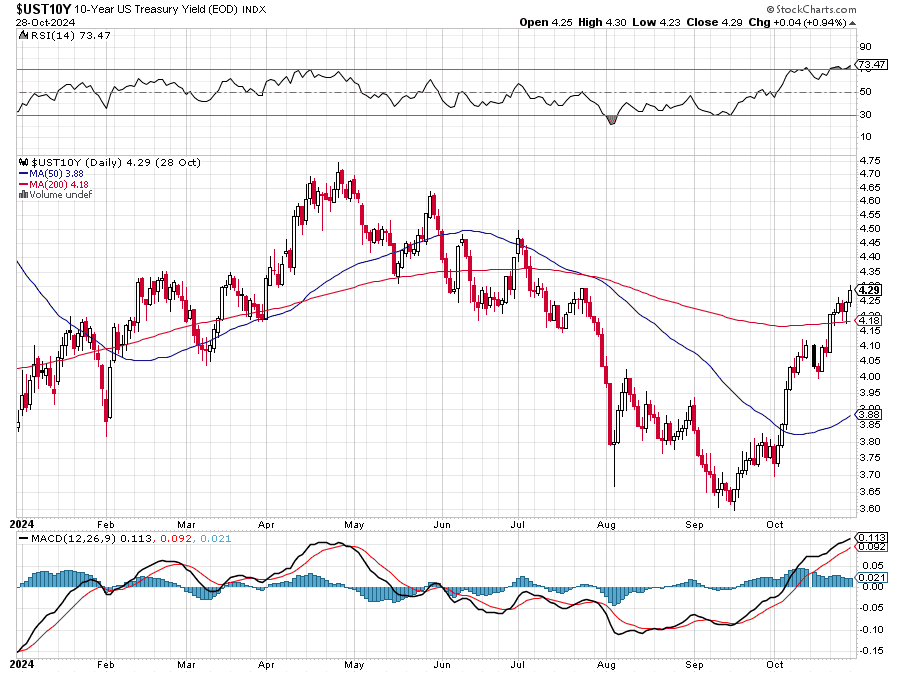

Shares of Builders FirstSource BLDR are trading off today as the 10-year Treasury yield chugs higher yet again and D.R. Horton DHI, one of the largest homebuilders, issues preliminary home delivery guidance for the coming year that implies modest growth compared to the last 12 months of deliveries.

We suspect these two events go hand in hand as the 10-year Treasury yield has retraced its way all the way back to late July levels, meaning they are considerably higher than the September low near 3.65%.

The rebound in Treasury vields has also pulled mortgage rates higher, which explains Horton’s more cautious outlook. For the coming year, Horton expects to close 90,000-92,000 homes, up from 89,690 over the last 12 months. That implies a modest level of growth, but when we annualize the last two-quarters of Horton's home closings, which tally 95,604, it becomes clear the market was likely expecting Horton’s initial 2025 forecast to be higher. This disappointment explains why DHI shares are down double digits, as are our BLDR shares.

Besides Horton’s initial estimate at 2025 home closings, what stood out to us was its comment about its 2025 outlook hinging on the 2025 spring selling season. This coincides with the risk we’ve called out over the last few days that the Fed may not deliver as many rate cuts between its November and June policy meetings.

While others are raising questions over the number of rate cuts coming for the balance of the year, to the extent the Fed’s November policy statement and comments from Fed Chair Powell next Thursday point to a slower rate of cuts, market assumptions about interest rate-sensitive stocks will be reset.

Recognizing this likelihood, we’ve purposely shared the portfolio and members should stay on the sidelines with BLDR shares at least until we get past next week’s Fed policy meeting. Better to let both shoes drop so to speak than move too soon on the shares. As we digest this week’s economic data and its implications for Fed rate cuts, we’ll continue to keep a close eye on BLDR shares and the support they have near $168.

Let’s remember the Fed’s intent is to return monetary policy over time to a more neutral footing, which means there will be more rate cuts coming over the next several quarters. That will lead to lower mortgage rates and a pick-up in housing activity, which what we want to capture by owning BLDR shares over the long-term. As we see it, this resetting of housing expectations will lead to an opportunity to pick up BLDR shares at better prices.

More Pro Portfolio:

- We're Adding Shares and Upping Our Price Target on This Holding Amid Record Backlog

- Weekly Roundup: Multiple Points of Confirmation for Our Portfolio Positioning

- AI Generates News: A Look at the Headlines That Speak to Our Stocks

At the time of publication, TheStreet Pro Portfolio was long BLDR.