What the Market Has Wrong on This Latest Jobs Report

There is more going on than the modest uptick in the unemployment rate.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The big November Employment Report we’ve all been waiting for this week is out and there were some positives for consumers. But those same findings also add to the growing likelihood that the Fed delivers a monetary policy pause on December 18.

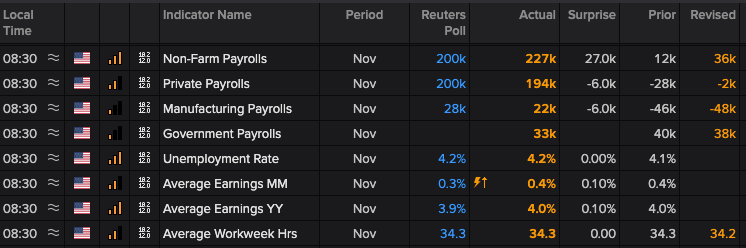

November job creation rebounded stronger than the market expected, coming in at 227,000 jobs versus the 200,000 consensus. To that, we can add the positive revisions for job creation in September (plus 255,000 versus the prior figure of 223,000) and October (36,000, up from the initial 12,000). Tallying those figures points to more folks working than previously expected which we see as a positive for the economy and consumer spending, a plus for our shares of Mastercard MA. It also confirms that the jobs market need not be a concern for the Fed at this time.

The November report also showed that wage growth accelerated compared to October, rising 4.0% year over year, up from 3.9%, but also sequentially up 0.4% versus October’s 0.3% figure. While some will quickly jump on the implied annualized sequential wage figure of 4.8%, what should stick out as much is year-over-year inflation data being stuck at 4.0% for the last three months after rising from 3.6% in July and 3.8% in August.

Here again, this is good for the consumer and spending as well as the economy, but from the perspective of inflation moving back toward the Fed’s 2% target, this is not a good look. Our take is that the jobs figures and the wage data of the last few months lean more toward the Fed pausing delivering 75-basis points in rate cuts at its two most recent policy meetings. As Fed Chair Powell said Wednesday, the Fed can take a more cautious approach to finding the neutral level of monetary policy.

So, the question we have to answer then is why did December rate cut expectations tracked by the CME FedWatch Tool jump to more than 85% this morning? The likely explanation was the tick higher in the Unemployment Rate to 4.2% in November from 4.1% in October, matching the market forecast.

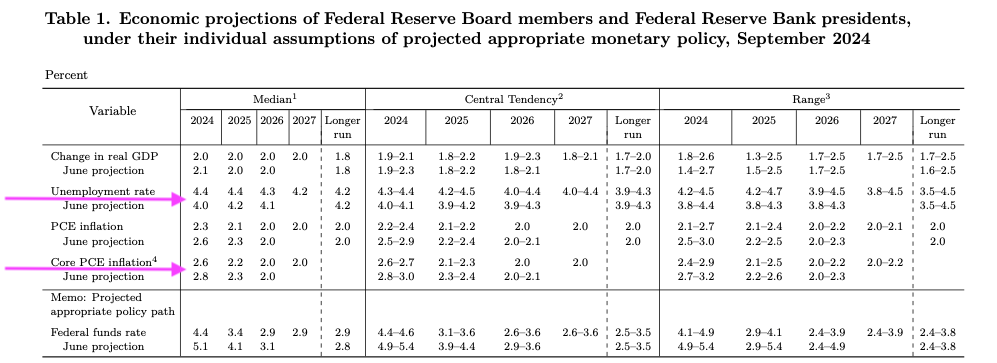

But when we take a harder look at the data, that 4.2% figure for November is only back to August levels and is below the 4.3% level we saw in July. More importantly, it’s below the 4.4% figure the Fed shared for 2024 in its updated September economic projections. As we’re looking at that table below, we also see the recent pick up in the October core PCE price index to 2.8% puts it above the Fed’s 2.6% target for 2024.

In our view, the market is eyeing the uptick in the November Unemployment Rate as fostering a December rate cut. For the reasons we outlined below, we’re less inclined to agree with that logic.

Next week brings the November CPI and PPI data, and as we’ve discussed with you, the recent headline and core figures for both reports have been trending in the wrong direction. November wage data this week as well as the lift we saw in the November ISM Service PMI price data suggest we could see core CPI and PPI figures remain sticky next week. If that is what the data shows, the market will need to revisit Powell’s “more cautious” comment from earlier this week.

Near term, the market’s reaction could push the S&P 500 and Nasdaq Composite back into overbought territory after Thursday's move lower. We’ll enjoy the impact on the Portfolio, but we’ll be more disciplined when it comes to putting cash to work in this environment.

More Pro Portfolio

- We're Locking In a Triple-Digit Gain for This Deeply-Overbought Name

- Weekly Roundup: After a November to Remember, What's in Store for December?

- Headlines for the Holidays: News That Speaks to the Pro Portfolio

At the time of publication, TheStreet Pro Portfolio was long MA.