We’re Adding a Trucking Play to the Portfolio Bullpen

2026 North American industry orders are picking up, as is U.S. truck tonnage data.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Today we are adding heavy-duty and medium-duty truck company Paccar (PCAR) to the Pro Portfolio Bullpen.

While not a household name, Paccar is the second-largest U.S. heavy-duty truck manufacturer with around 30% of the market. With its Kenworth and Peterbilt brands, the company also participates in the medium-duty truck market.

We may not ultimately call Paccar up to the Portfolio, but the decision will hinge on what continues to unfold in the domestic economy and how that impacts demand for new trucks, which per data from the American Trucking Association, moved roughly 73% of the nation’s freight by weight in 2024.

The economic data we discussed earlier today, the better-than-expected headline and new-order data for ISM’s May Manufacturing and Services PMI reports, point to the domestic economy continuing to hum. Based on QTD data so far, economic models from the Atlanta Fed and the New York Fed have GDP for Q2 2026 running at 2.5%-3.0% compared to the revised Q1 2026 figure of 1.6% and 0.5% for Q4 2025.

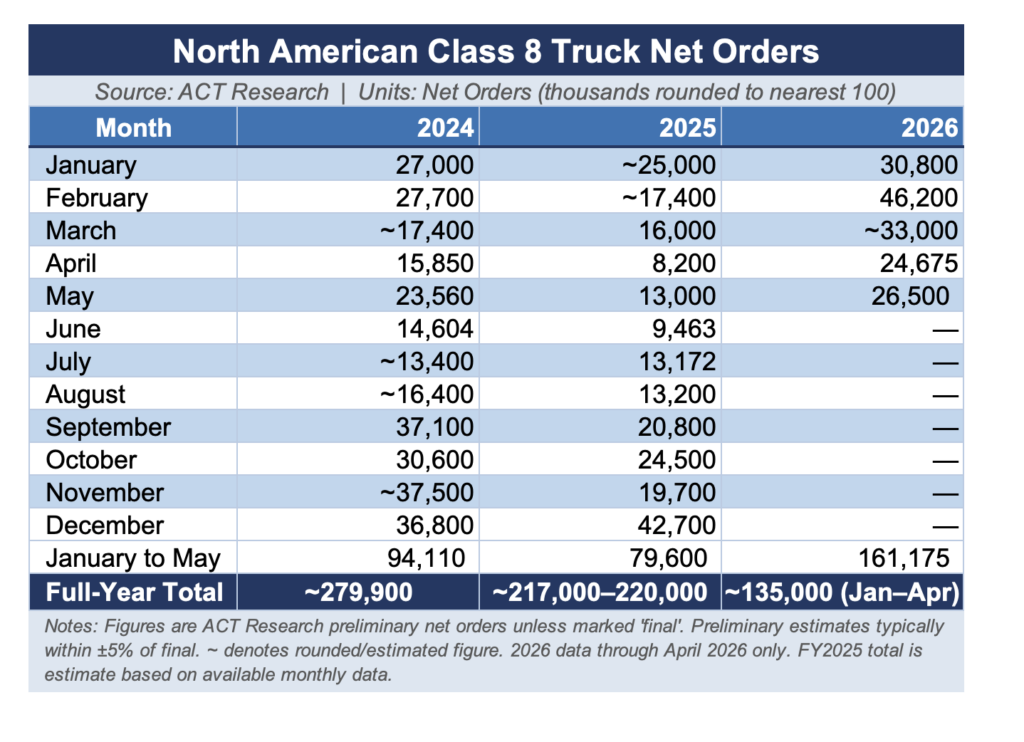

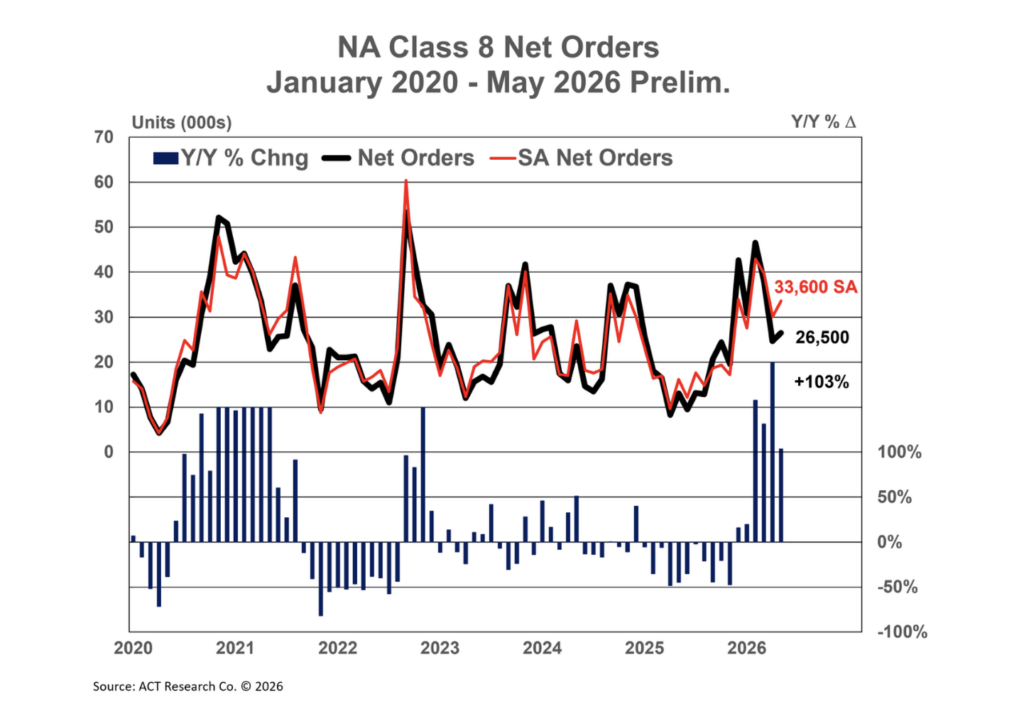

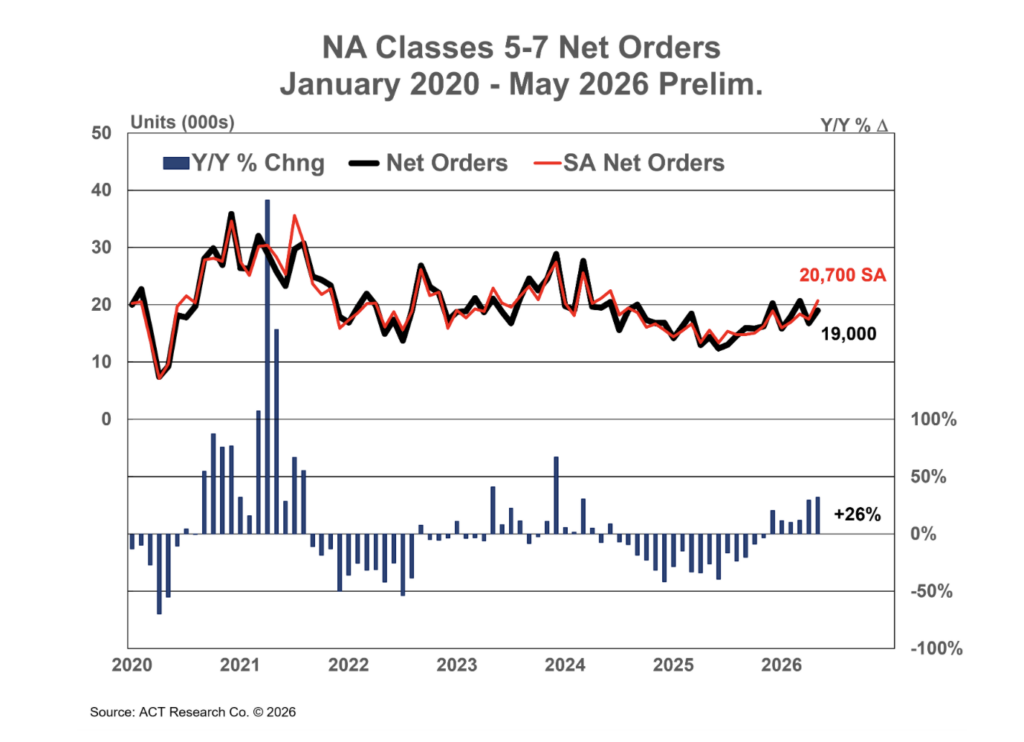

To that, we can add the uptick in heavy-duty (referred to in the industry as Class 8) and medium-duty (Class 5, 6 and 7) truck orders in April and now May. May heavy-duty truck orders climbed just over 100% year over year, but let’s remember that 2025 activity was likely depressed following Liberation Day developments and subsequent tariffs. Total Class 5-7 truck orders tallied 19,000 in May, up 32% year over year, but here too off depressed levels.

Also, this year, business owners and owner-operators can utilize 100% bonus depreciation (restored by the One Big Beautiful Bill Act) or Section 179 expensing to write off the entire purchase price of a qualifying heavy commercial vehicle, including new Class 8 and Class 5-7 trucks. With data from ACT Research finding the average age of a U.S. Class 8 tractor is 6.3 years, the highest in more than a decade, the ability to fully depreciate a new truck in its first year is likely a factor helping to drive replacement demand. As we can see in the table above, year-to-date heavy-duty truck orders are up considerably compared to the same period last year and in 2026.

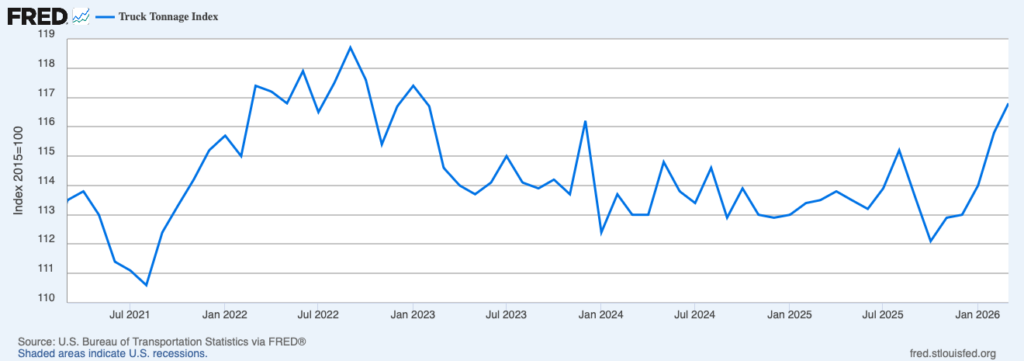

On its face this looks promising, as does the year-to-date trend in truck tonnage.

As we refine our thinking on PCAR shares, we’ll want to track order and production data from ACT as well as monthly truck tonnage indicators, fuel costs and other factors that may influence truck orders. That said, when Paccar reported its Q1 2026 results in late April, it forecasted the 2026 U.S. and Canadian heavy-duty truck market to be 230,000-270,000 units compared to 233,000 in 2025. Around that time, truck competitor Volvo (VLVLY) shared its view for ~265,000 in heavy-duty truck retail sales this year.

More recent data suggest that industry sales figures for this year could be at the upper end of Paccar’s 2026 range and closer to Volvo’s. With that looking to be a low-double-digit year-over-year increase, we are starting to examine H2 2026 revenue and EPS prospects vs. current consensus expectations.

And as we do that work, we will also be mindful that while Paccar derives the bulk of its revenue from the U.S. truck market, especially during a period of rising demand, we’ll want to monitor the ones for Europe (25% of Paccar’s 2024 deliveries) as well as Mexico, South America and other markets (18% of 2024 deliveries). With that in mind, we will also want to keep in mind the dollar and the impact of currency on Paccar and potential new tariffs from the Trump administration.

More Pro Portfolio:

- Taking Advantage of Jensen Huang’s ‘Gift’

- We’re Tracking 29 Signals Across 9 Portfolio’s Investment Themes

- May Monthly Roundup: Sell in May? No Way!

At the time of publication, TheStreet Pro Portfolio had no positions in any securities mentioned.