Weekly Roundup: Notching Another Gain on Strength in Financials and Tech

It was a busy week of moves for the poretfolio, and we’re at the ready for more opportunities as earnings season accelerates.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

While continued strength in quarterly earnings from the financial sector started this week off on an upbeat note, back-to-back 2025 guidance trimming from UnitedHealth Group (UNH) and ASML Holding (ASML) took some wind out of the market’s sales. Ultimately, though, quarterly earnings from Taiwan Semiconductor (TSM), Netflix (NFLX), and favorable iPhone 16 data points led the market to notch another gain this week. As we describe below, multiple levers led the portfolio to outpace this week’s climb in the S&P 500.

The market’s reaction to developments at UnitedHealth, ASML, and American Express (AXP) on Friday, served as reminders we could see some bumpy days ahead as this earnings season accelerates over the next few weeks. We think the market’s continued melt-up and investor sentiment once again knocking on “Extreme Greed” on Friday are a combination that could pressure the shares of companies that do not deliver pristine earnings and guidance. While not yet overbought, the relative strength indexes (RSI) for the S&P 500 and Nasdaq Composite have crept higher week over week as has the S&P’s valuation.

Those additional layers raise the stakes that much further and the combination could result in some market weakness in the heat of the earnings season. We saw that this week with shares of Applied Materials (AMAT), which we took advantage of. That is why even though we will remain disciplined and prudent investors, we also will remain at the ready to take advantage of opportunities as they present themselves to us. Such opportunities, if they come to pass, may allow us to pick up more shares of well-positioned companies, allowing us to reap the benefits down the road just like we are today.

Have an enjoyable weekend and be sure to catch our next batch of ripped-from-the-headlines confirmation points for the portfolio’s holdings and investment strategies on Saturday.

Catching Up on the Portfolio This Week

While the market continued to chug higher this week, we had another week of outperformance because of the strong gains registered by Morgan Stanley MS, Marvell Technology MRVL, Dutch Bros BROS, Vulcan Materials VMC, Apple AAPL, and Nvidia NVDA. The biggest drag on the portfolio this week coming off unexpected booking weakness and a trimmed 2205 outlook from ASML Holding was Applied Materials AMAT. However, following bullish capital spending comments from Taiwan Semiconductor (TSM), we used that weakness to scoop up more AMAT shares.

We made several moves with the portfolio during the week starting with lifting several panic points for existing positions on Monday. That same day we locked in another slice of profitable gains for Axon Enterprise AXON as the shares moved deeper into overbought territory. Strong September-quarter performance on Tuesday and Wednesday for Bank of America BAC and Morgan Stanley led us to boost our price targets for both.

On Thursday, we opted to exit our position in Three-rated Elevance Health ELV following September-quarter EPS weakness that is expected to continue in the current quarter. We used proceeds from that trade to fund the pick-up of additional AMAT shares as well as to buy more of Elastic N.V. ESTC. Later that day, we locked in big gains in shares of Morgan Stanley and Marvell as part of some prudent portfolio management following post-earnings gains for Morgan and bullish comments this week from Ericsson (ERIC) and Taiwan Semi for Marvell’s business segments.

On Friday, those same bullish comments from Taiwan Semi paired with recent ones from Hon Hai and others led us to boost our Nvidia price target. In the same Alert, we also lifted our price target for The Trade Desk TTD shares following the thesis-confirming comments from Netflix (NFLX), made during its quarterly results, for its advertising business model. Findings for digital advertising prospects and the Connected TV market in a new research report were also a factor in our decision to lift our TTD target.

The net effect of those moves is we now have 28 active positions and 11.3% of the portfolio’s assets in cash. That leaves us with ample firepower should opportunities to pick up additional shares of existing holdings present themselves as this earnings season continues. We would welcome the opportunity to add more shares of Meta META, ServiceNow NOW, Eaton ETN, and Dutch Bros to our holdings, but only at favorable risk-to-reward levels.

Now let’s see what Wall Street had to say about our holdings this week:

Alphabet GOOGL shares were added to the “Tactical Outperform” list at Evercore ISI.

Philips Securities upped shares of Bank of America to Accumulate from Neutral with a $44 target, while Evercore boosted its target to $45, keeping an Outperform rating on the shares. Other price target increases for BAC shares were delivered from Oppenheimer, Morgan Stanley, and Barclays.

Tigress Financial raised its price target for Costco COST to $1,065 from $975, reiterating its Buy rating. On Thursday, we explained how comparing Costco’s September sales report against the September Retail Sales data confirmed Costco continues to take consumer wallet share. We also shared what we’re watching that could lead us to revisit our COST price target.

Susquehanna did some catching up with its price target for Lockheed Martin LMT, boosting it to $705 from $565. We plan on revisiting our price target once Lockheed presents an updated look at its multi-year delivery schedule now that it's back delivering F-35s.

Citi reiterated its Buy rating on Marvell stock with a $91 target price, highlighting confidence in upside to the company's AI sales targets. Comments we shared from Ericsson and Taiwan Semi this week offer a more well-rounded view of Marvell’s business, keeping us long the stock in size despite this week’s register ringing.

Mizuho hiked its Meta price target to $650 from $600 ahead of earnings, which are set for release on October 30. TD Cowen also lifted its price target for the social media company to $675 from $600. If you missed our price target increase for META a few weeks back, you can find it here.

Piper Sandler lowered its price target on Microsoft MSFT to $470 a share from $480, while KeyBanc, citing strong IT spending, lifted its target to $505 from $490.

Above we noted we boosted our Morgan Stanley target, but we were hardly alone. Barclays lifted its target to $135, while Goldman upped its to $121.

On Friday, OTR Global raised its rating on ServiceNow to Positive from Mixed after missing out on the nice 40% move we captured in the shares. Earlier in the week Oppenheimer, citing positive channel checks, raised its NOW price target to $1,020 from $820. NOW shares also saw Deutsche Bank hoist its price target to $1,020 from $900 this week. Those moves come after we hiked our NOW price target to $1,000 from $900 the prior week.

Goldman Sachs raised its Universal Display OLED target to $244 from $236, still a few bucks below our $250 target. We continue to see multiple tailwinds for the adoption of organic light-emitting diode displays across multiple end markets.

This Week's Portfolio Videos

We cover a lot of ground during the week in our Daily Rundowns. If you happened to miss one or more of them, here are some helpful links:

Monday, October 14: Our Game Plan for the Week as the Pace of Earnings Accelerates

Tuesday, October 15: How Two Companies Spooked the Market Over 2025 Earnings

Wednesday, October 16: Strong Gains Have Us Watching These Two Positions

Friday, October 18: Recapping Our Gains and Shares Swapping

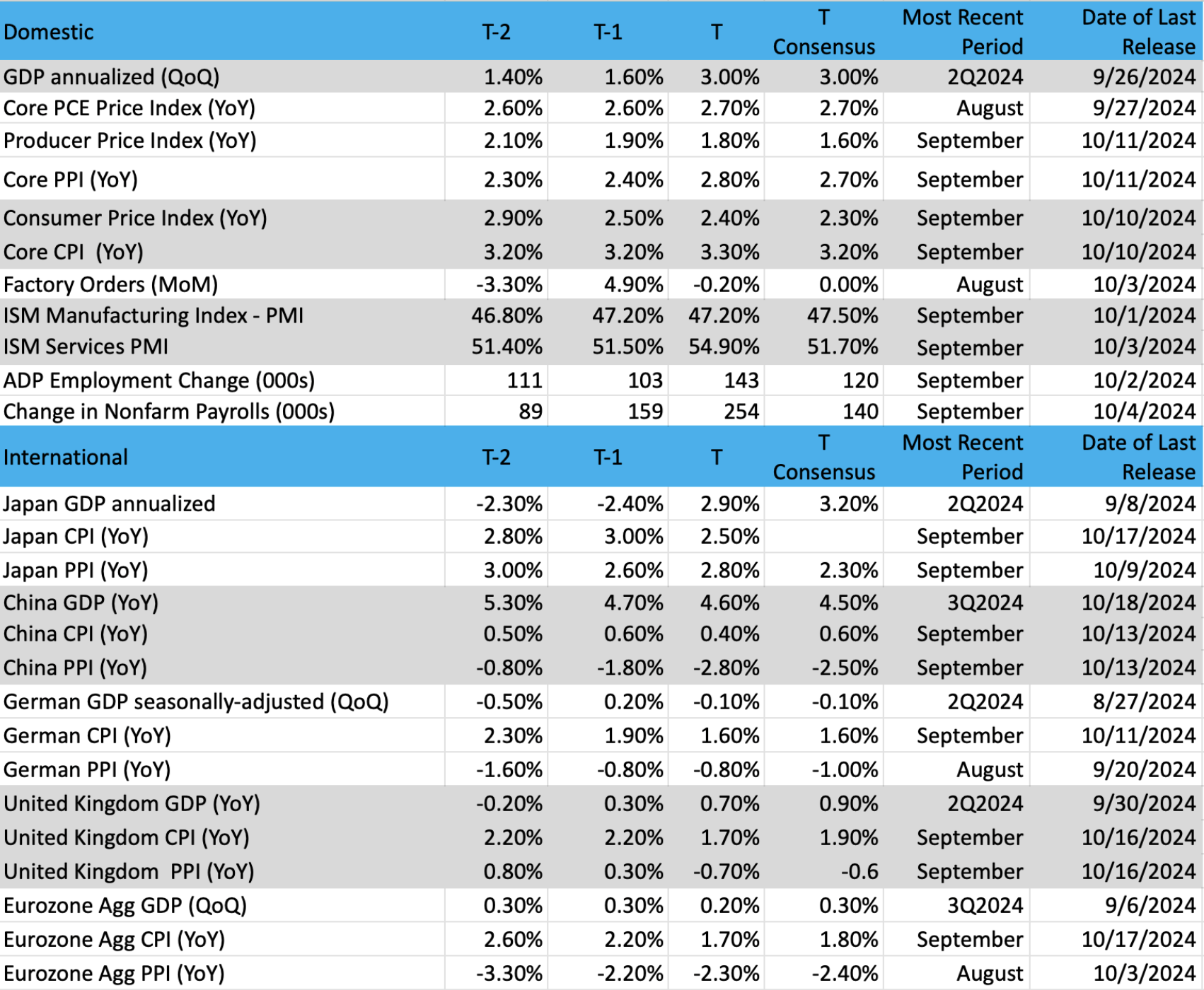

Key Global Economic Readings

(Note: T is the most recent period, T-1 is the prior period's reading and T-2 is two periods back, the intent being to illustrate any trends)

Chart of the Week: iShares Trust US Transportation (IYT)

Some say,"As the transports go, so goes the economy." It does make sense. Goods and services being moved around the world tell us the health of the economy. Shipping by air, freight, trucking, car, rails, and tanker are the basics of product delivery. The transports tend to give us a good view of business going forward.

The iShares Trust US Transportation (IYT) is an ETF that contains many important companies around transportation. Names such as FedEx, Uber, United Airlines, UPS, Union Pacific, and Delta Air Lines are concentrated in this ETF. Recent trends have been bullish in this group, and there is no clear reason why those trends cannot continue to play out as we approach the end of 2024.

The index hit a bottom in early Augus. Most stocks fell sharply at that time too, but the IYT bounced back and now shows several bullish characteristics. First off, the price chart is definitively bullish, with blue candles. This is the GoNoGo composite of indicators, and when flashing blue this is a strong buy signal. Parabolic SAR (stop and reverse) is also in bullish form, with good support for the price action (dots in the top pane).

Other indicators confirm the trend. MACD (moving average convergence divergence) is on a strong buy signal, stochastics (momentum) is overbought (does not mean sell), and the chop indicator is moving down, which means a trending move is happening.

The series of higher highs, and higher lows in the IYT is a textbook uptrend pattern. We look for that to continue. There's nothing negative in the chart! The economy remains robust, and the transports confirm it.

Other charts we shared with you this week were:

Monday, October 14: S&P 500 - Bulls Are in for a Pleasant Few Weeks

Monday, October 14: Elastic NV (ESTC) - Our Newest Name Shows an Opportunity Down the Road

Tuesday, October 15: Alphabet (GOOGL0 - This Magnificent Seven Chart Is Very Intriguing

Wednesday, October 16: Qualcomm (QCOM) - Qualcomm Is Unflappable

Thursday, October 17: Apple (AAPL) - Apple, What Are You Waiting For?

The Week Ahead

As we move further into the second half of October, the number of September economic data points will slow, ushering in the first hard look at how the economy performed in October. We’ll get that with Thursday’s Flash September PMI data from S&P Global. We will put that report through the usual gauntlet that includes moving past the headline figure and delving into what the data say about job creation, inflation, and new order activity.

Next week also brings a few more pieces of September Housing data, including Existing Home Sales and New Home Sales. Setting the stage for those reports, on Thursday (October 17), data published by the Mortgage Bankers Association showed mortgage applications for new home purchases increased 10.8% year over year in September.

Based on those findings, MBA estimates new single-family home sales were running at a seasonally adjusted annual rate of 680,000 units in September. While that’s a slower pace than the 716,000 single-family homes sold in August and the 739,000 sold in July, far more sold in the September quarter than were sold in the July quarter. As we dig into those two September housing reports, we’ll be mindful of recent double-digit delivery guidance from Lennar (LEN) and KB Home (KBH) as well as what Pulte (PHM) has to say next week. Based on what we see, we’ll revisit the price targets for our construction-related prices as needed.

Here's a closer look at the economic data coming at us next week:

U.S.

Monday, October 21

· Leading Indicators – September (10:00 AM ET)

Wednesday, October 23

· MBA Mortgage Applications Index – Weekly (7:00 AM ET)

· Existing Home Sales – September (10:00 AM ET)

· EIA Crude Oil Inventories – Weekly (10:30 AM ET)

Thursday, October 24

· Initial & Continuing Jobless Claims – Weekly (8:30 AM ET)

· S&P Global Flash Manufacturing & Services PMI – October (9:45 AM ET)

· New Home Sales – September (10:00 AM ET)

· EIA Natural Gas Inventories – Weekly (10:30 AM ET)

Friday, October 25

· Durable Orders – September (8:30 AM ET)

· The University of Michigan Consumer Sentiment Survey (Final) – October (10:00 AM ET)

International

Monday, October 21

· China: Financial Direct Investment – September

· Germany: Producer Price Index - September

Tuesday, October 22

· Eurozone: New Car Registrations - September

Wednesday, October 23

· Eurozone: Consumer Confidence (Flash) – October

· Canada: Bank of Canada Interest Rate Decision

Thursday, October 224

· Japan: Jibun Bank Flash Manufacturing & Services PMI - October

· Eurozone: HCOB Flash Manufacturing & Services PMI – October

· UK: S&P Global Flash Manufacturing & Services PMI - October

Friday, October 25

· Germany: Ifo Current Conditions & Expectations - October

In Friday’s video, we discussed that roughly 85% of the S&P 500’s basket will be reporting over the coming weeks. We’ll continue to mine reports from competitors, customers, and suppliers for holdings as we prepare for their quarterly earnings and guidance.

As we get ready for September-quarter results from ServiceNow (NOW), United Rentals (URI), and Labcorp (LH) later in the week, we’ll be assessing what’s said by SAP (SAP), IBM (IBM), Herc Holdings (HRI) and Quest Diagnostics (DGX). Results from General Dynamics (GD) and Northrop Grumman (NOC) will bring some added context to Lockheed Martin’s (LMT) results on Tuesday. In that report, we’ll also be looking for Lockheed’s multiyear delivery schedule.

Other reports we’ll be interested in reviewing are those from Pulte Group (PHM) and Lam Research (LRCX) given our holdings in Builders FirstSource (BLDR) and Applied Materials (AMAT). When we read through reports from United Parcel Service (UPS) and Digital Reality Trust (DLR), we’ll be matching their respective outlooks against 2024 digital shopping holiday expectations and expected data center capital spending.

Here's a closer look at the earnings reports coming at us next week:

Monday, October 21

· Open: SAP SE (SAP)

· Close: Nucor (NUE),

Tuesday, October 22

· Open: 3M (MMM), Comcast (CMCSA), Danaher (CHR), GE Aerospace (GE), General Motors (GM), Herc Holdings (HRI), Kimberly Clark (KMB), Lockheed Martin (LMT), Logitech (LOGI), PulteGroup (PHM), Quest Diagnostics (DGX)

· Close: Packaging Corp. (PKG), Texas Instruments (TXN)

Wednesday, October 23

· Open: Boeing (BA), Coca-Cola (KO), General Dynamics (GD), Hilton (HLT)

· Close: Celestica (CLS), IBM (IBM), Lam Research (LRCX), Lending Club (LC), ServiceNow (NOW), Tesla (TSLA), T-Mobile (TMUS), United Rentals (URI)

Thursday, October 24

· Open: American Airlines (AAL), Dow (DOW), Honeywell (HON), Labcorp (LH), MSC Industrial (MSCI), Northrop Grumman (NOC), UPS (UPS)

· Close: Boston Beer (SAM), Coursera (COUR), Deckers Outdoor (DECK), Digital Realty Trust (DLR), Universal Health (UHS)

Friday, October 25

· Open: AutoNation (AN), Booz Allen Hamilton (BAH), Colgate Palmolive (CL).

Portfolio Investor Resource Guide

· Economic Data: Here's a List of Links to the Key Economic Data We Closely Watch

· Investing Terminology: 16 Key Terms Club Members Should Know

· 10-Ks: Want to Know About a Stock? Read the Company's Reports

· 10-Qs: Unlock the Numbers and Key Information Behind Your Stock With the 10-Q

· Income Statement: Our Cheat Sheet to Understanding This Financial Document

· Balance sheet, Cash Flow Statements, and Dividends: How to Know If a Company Is Off-Kilter? Read Its Balance Sheet

· Valuation Metrics: Everyone Wants a Value. Here's How Investors Can Find

The Portfolio Ratings System

1 - Buy Now (BN): Stocks that look compelling to buy right now.

2 - Stockpile (SP): Positions we would add to on pullbacks or a successful test of technical support levels.

3 - Holding Pattern (HP): Stocks we are holding as we wait for a fresh catalyst to make our next move.

4 - Sell (S): Positions we intend to exit.