Why We're Lifting Multiple Panic Points

These factors have us keeping our panic points wider than usual.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

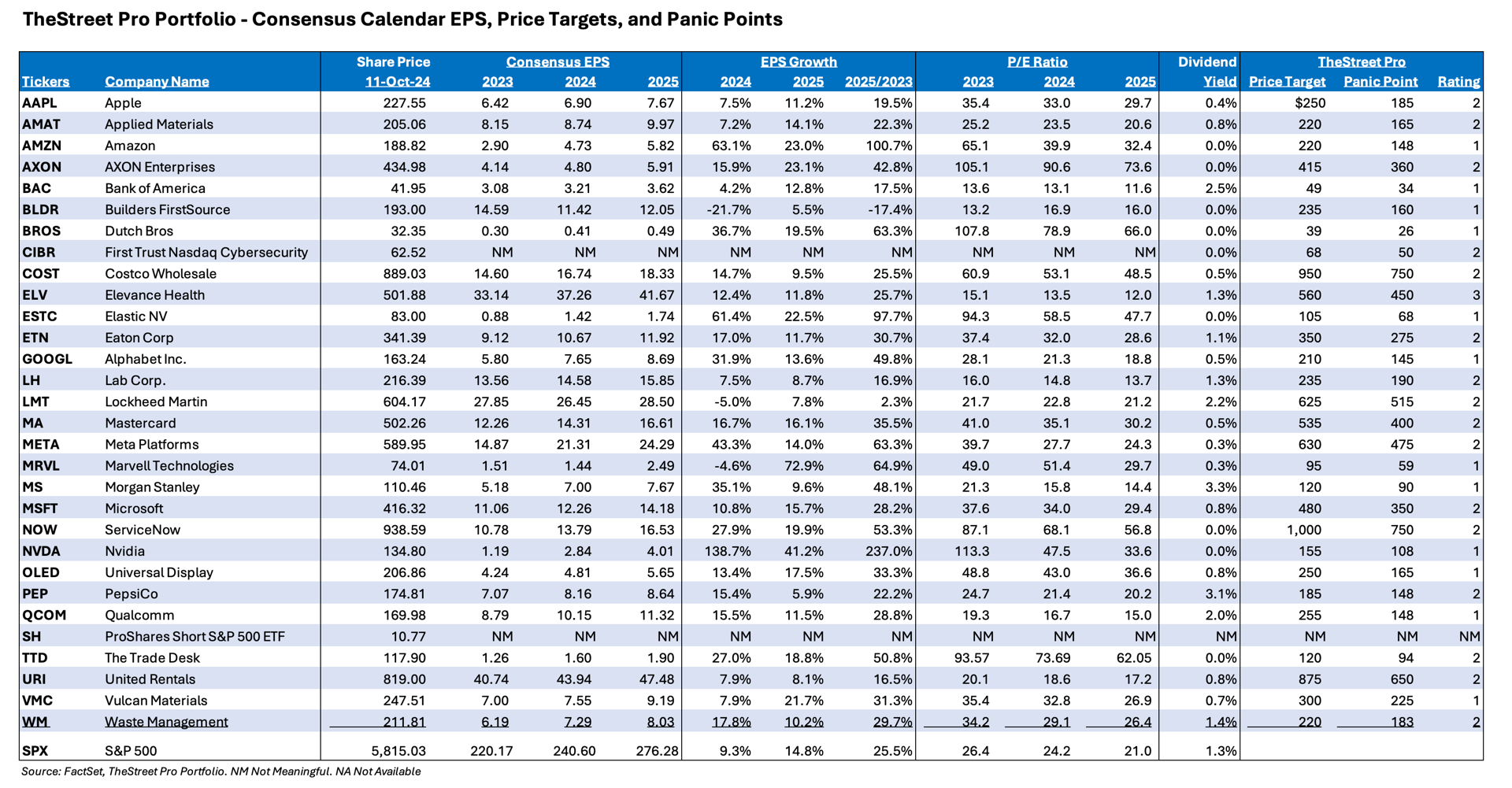

In Monday's Daily Rundown video, we discussed the accelerating pace of September quarter earnings reports just ahead of us. With that in mind, we are sharing an updated table containing the latest calendar consensus EPS figures for our holdings and the S&P 500. We’re also doing some catch up following the market’s continued melt-up and resetting many of our panic points higher.

EPS Expectations

Over the last few weeks, there have been a variety of data points, some economic, some monthly revenue reports and others that have cropped up. Let’s also not forget the impact of hurricanes Helene and Milton, which will slow construction and other activity in the Southeastern U.S.

In some cases, they have reaffirmed our thought process, while in some they have led us to boost a few price targets. Those same updates have led to some shuffling of calendar 2024 and 2025 EPS expectations for multiple Portfolio positions, but also for the S&P 500 as well.

The Bank of America BAC consensus 2024 EPS now sits at $3.21, down from $3.28, while EPS for 2025 has been lowered to $3.62 from $3.67

The consensus for Eaton Corp’s ETN 2024 EPS is currently set at $3.67, down from $10.76. For 2025, the market now expects EPS of $11.92 versus the prior consensus of $12.02

Labcorp LH is now forecasted to deliver EPS of $14.58 this year, down $0.04 per share, but its 2025 consensus EPS has been lifted to $15.85 from $15.81.

Meta META experienced positive increases for 2024 and 2025 to $21.31 and $24.29 from $21.24 and $24.16, respectively.

Following its recent earnings report, PepsiCo’s PEP 2025 EPS was revised to $8.64 from $8.76. No changes came to its 2024 EPS of $8.16.

Next year’s consensus EPS for United Rentals URI was reset at $47.48 from $47.62.

Feeling the impact of the recent hurricanes, their weather and subsequent damage, calendar 2024 and 2025 EPS for Vulcan Materials VMC was revised lower to $7.55 and $9.19 from $7.72 and $9.30, respectively. What may not be apparent in those revisions is the market sees a slightly faster rate of EPS growth next year than it previously did.

In response to recent iPhone sales chatter, Apple’s AAPL calendar consensus 2024 and 2025 EPS were revised lower to $6.90 and $7.67 from $6.92 and $7.75, respectively. We continue to think we will see an extended iPhone upgrade cycle that hinges on Apple Intelligence features in forthcoming Apple OS updates.

The consensus 2024 EPS for Applied Materials AMAT was lifted to $8.74 from $8.65, but the expectation for 2025 was adjusted to $9.97 from $10.16. Quarterly results this week from ASML (AMSL) and Taiwan Semiconductor TSM will tell us if that 2025 revision was an overreaction to Intel’s INTC woes.

As we make those changes, we’ve also noticed another step down in consensus EPS expectations for the S&P 500 to $240.60 this year and $276.28 for 2025. The revision for 2024 comes entirely in 2H 2024 with the rate of EPS growth compared to 1H 2024 now at 6.0%, far lower than the 11.2% projected in July.

Portfolio Panic Point Adjustments

We’ve all witnessed the strides made by the Portfolio over the last several weeks, and that is leading us to lift multiple panic points across the Portfolio. Because we are wading deeper into the September quarter earnings with a stretched market valuation and investor sentiment knocking on the door of “extreme greed,” we are keeping our panic points a little wider than usual, given the potential for outsized reaction to customer, competitor or supplier earnings and the risk of a market pullback:

- Applied Materials to $165 from $160

- Axon AXON goes to $360 from $$325

- Bank of America to $34 from $32

- Dutch Bros BROS inches ahead to $26 from $25

- First Trust Nasdaq Cybersecurity ETF CIBR to $50 from $$48

- Eaton’s is boosted to $275 from $250

- Meta’s is upped to $475 from $435

- Marvell's MRVL panic point climbs to $59 from $55

- Morgan Stanley’s MS goes to $90 from $84

- The panic point for ServiceNow NOW jumps to $750 from $675 following our recent price increase to $1,000.

- We’re bumping up our Nvidia NVDA panic point to $108 from $100

- The one for Universal Display OLED rises to $165 from $155

- Following continued strength in Trade Desk TTD, we’re resetting our panic point at $94, up from $85

More Pro Portfolio

- Why We Opened a Position in a $8.4 Billion AI Name

- Weekly Roundup: Portfolio Begins October With Big Gains and Big Moves

- We Did the Homework for You: Here're the Top Stories on Our Investing Themes

At the time of publication, TheStreet Pro Portfolio was long BAC, ETN, LH, META, PEP, URI, VMC, AAPL, AMAT, AXON, BROS, CIBR, MRVL, MS, NOW, NVDA, OLED and TTD.