Updating Our Table With the Latest EPS Expectations

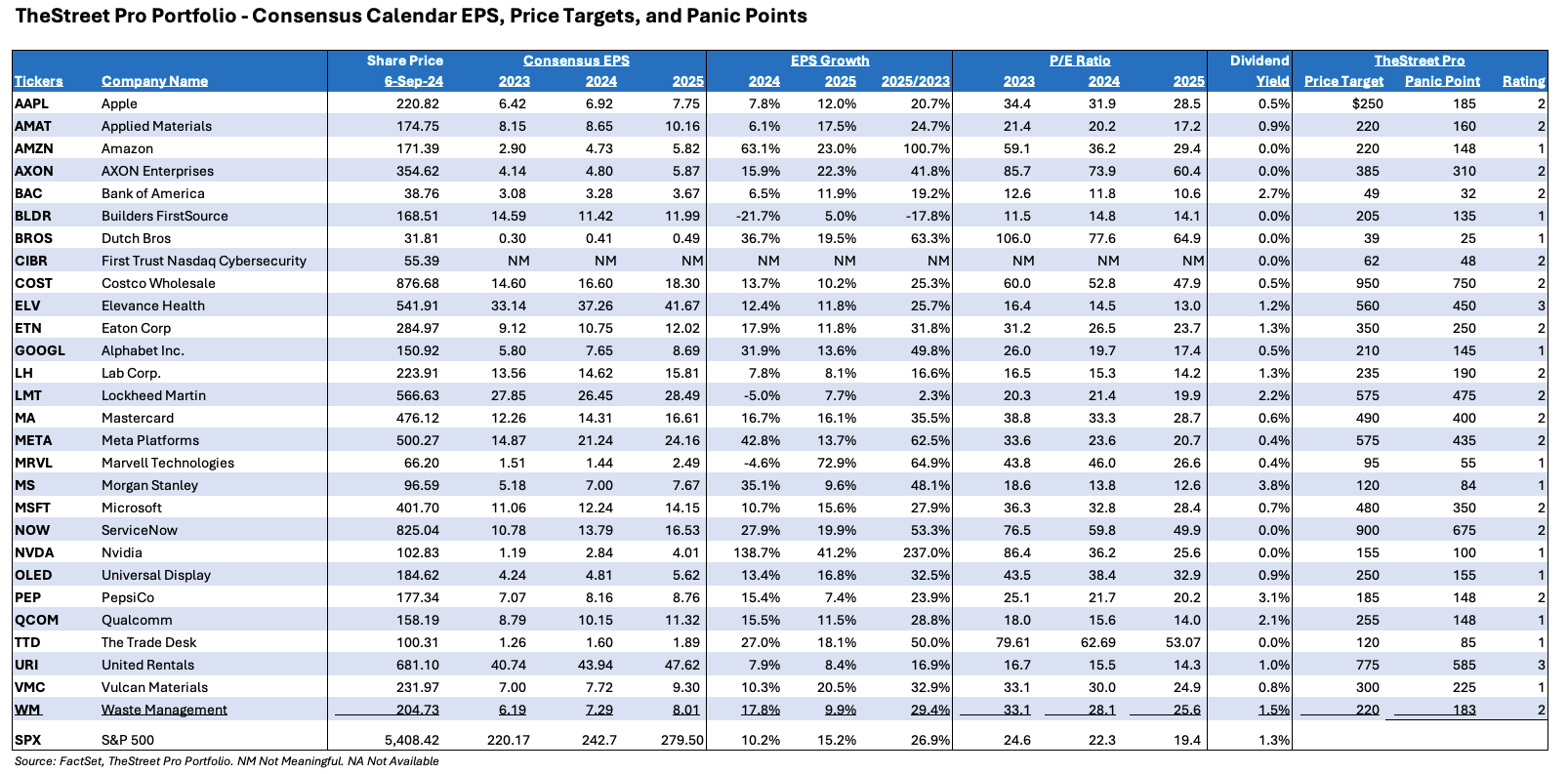

We’ve captured consensus calendar EPS expectations for our holdings and the S&P 500.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Last week, one of our messages was that “summer vacation” was over and with that in mind we wanted to take a beat to let consensus calendar EPS expectations for our holdings catch up with any recent analyst changes. We also wanted to take a fresh look at consensus EPS expectations for the S&P 500 for 2H 2024 and 2025, and what those revisions say about expected EPS growth for that market barometer and its current valuation.

For the S&P 500, what we see is 2H 2024 EPS expectations softened further and are now only expected to rise 7.4% compared to 1H 2024. Yet, the market’s consensus view for 2025 that called for an earnings re-acceleration has only heated up further.

As of last Friday, the figures tabulated by FactSet point to the basket of S&P 500 companies growing the collective EPS by 15.2% next year compared to 2024. That does not jive with an economy on the brink of hard landing, which is the scenario depicted in the latest CME FedWatch Tool with 100 to 125 basis points of rate cuts by the end of this year. Following Monday's updated rolling GDP forecast for the current quarter to 2.5% from 2.1% via the Atlanta Fed’s GDPNow model, we’ll revisit the CME FedWatch Tool to see if that softened the market’s arguably aggressive outlook. Our thinking is that the 2025 EPS growth figure is more likely to come down between now and January than not.

Before the market focuses on that 2025 figure, the S&P 500 closed last week at 22.3 times expected 2024 earnings. When compared against the multi-year peak P/E of 23.4 times expected current year EPS reached several weeks ago, it suggests that unless we see a sharp re-acceleration in 2H 2024 EPS prospects or the Fed telegraph far more rate cuts than expected (unlikely), the S&P 500 has less than 5% upside. As we think about that, let’s remember that we don’t “buy the market” but individual stocks with better EPS prospects that are benefiting from structural changes and other tailwinds.

For our purposes, we’ll use the revised S&P 500 EPS forecasts as our benchmark for assessing new candidates for the Portfolio and the Bullpen, so we continue to focus on companies with superior EPS growth prospects. Those prospects can shift, and we’ve seen that with lifted expectations for Amazon AMZN, Bank of America BAC, Mastercard MA, Meta Platforms META, Nvidia NVDA and PepsiCo PEP over the last several weeks.

We’ve seen similar movement with expectations for Apple AAPL, which reflects the market’s enthusiasm for the iPhone upgrade cycle and Apple Intelligence. Earlier on Monday, we shared what we might hear spinning out of that event and our game plan from AAPL and Qualcomm QCOM shares.

What we did not see across our holdings was any downward or negative EPS revisions. As we navigate the next few weeks, which are filled with investor conference presentations, we’ll continue to update this table for the Portfolio and share it with you. When we do that, barring any actions taken with the Portfolio, we’ll make any changes to existing panic points as needed.

More Pro Portfolio

- Buying More Stock of This Semi-Cap Equipment Position

- Weekly Roundup: Is the Market Setting Up for an April Repeat?

- The AI Conundrum, Cyber Threats, and Our Digital World: More News on Our Strategies

At the time of publication, TheStreet Pro Portfolio was long AMZN, BAC, MA, META, NVDA, PEP, AAPL and QCOM.