Powell on Deck: Why He Could Disappoint Some Folks

Plus, the September investor conferences could bring new opportunities for investment.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

*Fed Chair Powell is on deck at 10 a.m. ET, and here’s what we expect

*The market may be disappointed by Powell’s lack of rate-cut clarity

*Upcoming data will determine the size of an increasingly-likely September rate cut

*The wave of September investor conferences could bring opportunities to the portfolio

Friday is the day the market has been waiting for: Fed Chair Jerome Powell and the comments he makes at 10 a.m. ET from Jackson Hole. We’ve shared what we expect Powell will say, and for the ones that missed those comments, we expect that he will acknowledge continued progress on inflation and the slower-than-previously-thought jobs market, but stop short of showing the Fed’s plans for rate cuts.

We could hear words like “more good data,” ”growing confidence” and the like, but by no means should we expect Powell to reveal the Fed’s updated playbook. Remember, we are not only in between Fed policy meetings, but the next 26 days could bring data that tips the scales in favor of a 25-basis point rut, a 50-basis point one or no rate cut at all.

Our growing sense is that the Fed will deliver a cut in September, but the data between now and September 18, 2024, will determine not only how big of a cut but the Fed’s policy statement language and its updated set of economic projections. For that reason, we continue to think that there is room for some in the market to be disappointed by Powell’s comments later this morning.

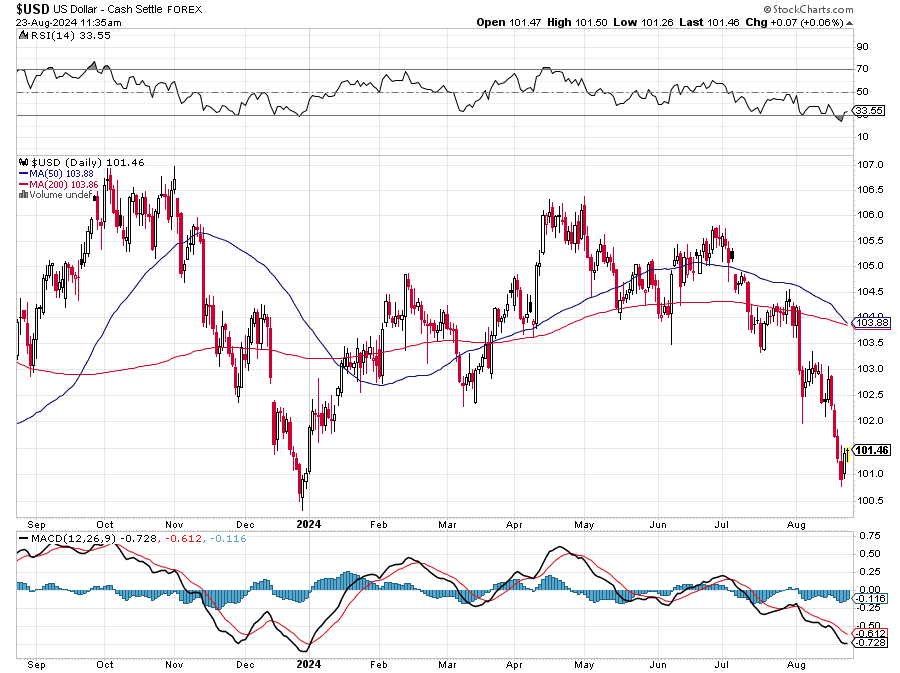

While that could bring some opportunities, let’s remember that September tends to be a challenging month for the market. Not only are we back to having trading desks fully staffed after the Labor Day weekend, but companies will also be making the investment conference rounds. Yesterday, we shared why the Flash August PMI data from S&P Global signals that we should focus on margin comments in those presentations. We will also be interested in what those with non-U.S. operations have to say about the recent slide in the dollar, which should be a bit of a tailwind for those operations.

Those and other comments will follow the July and August data for Manufacturing & Service PMIs from ISM, job creation, wages and, eventually, CPI, PPI and retail sales. What this means is that we could see companies tweak their outlook for the second half of the year before they enter their September quarter quiet periods. If the coming data reinforces that the economy is slowing and the margin pressure is building, it could bring far more interesting opportunities for us.

Between now and then, we’ll continue to ferret out new Bullpen candidates, so if things play out as we suspect, we’ll be ready. We’ll also continue to monitor positions that are encroaching on their price targets. As we refresh our fundamentals and technical analysis for them, we’ll determine if there is more upside to be had or if more prudent action is warranted.