Weekly Roundup: Powell’s 'Adjustment' Drives the Market and the Portfolio Higher

While we enjoy the move and its impact on the Portfolio, we see some warning signs.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

The stock market notched another weekly gain, the vast majority of which came after Fed Chair Powell’s Friday Jackson Hole comments that confirmed a monetary policy “adjustment” was near. While wildly expected, the Fed chair stopped there, not calling out specific timing or rate cut size. Pretty much, that’s what we expected him to do and the market certainly liked what it heard.

We did too, but in Friday’s video, we shared our concern that market expectations for the number of rate cuts to be had this year are likely once again out over their skis. Data between now and the Fed’s September policy meeting will dictate the size of that increasingly likely rate cut. It will be the Fed’s policy statement language, Powell’s September presser and the Fed’s updated set of economic projections that will set or potentially re-set market expectations for the total number and size of rate cuts for this year.

Should the market need to recalibrate its expectations, something we think is likely given recent data, that re-think could bring volatility back into the market. That could bring opportunity for us, but let’s also remember that as longer-term investors, our thinking should be on where Fed rate cuts could land the Fed funds rate over the next 12 to 18 months. It’s that prospect for far lower rates that keeps us longer-term bullish on several names in the portfolio, including Builders FirstSource BLDR.

Getting back to the near-term, during the week, the S&P 500 became short-term overbought, and the end of the week surge made that even more so. The week’s move for the S&P 500 also placed its P/E above 23-times expected 2024 EPS, only just below the recent peak P/E multiple of 23.4-times set earlier this year. This tells us that to move sustainably higher, that market basket will need to deliver stronger-than-expected EPS growth for that market basket in 2H 2024. But, in the last few weeks, we’ve seen those 2H 2024 EPS growth prospects soften to +7.8% compared to 1H 2024, down from more than 11% at the end of July.

To aggressive Fed rate cut expectations, an overbought market and a stretched market P/E valuation, we can add the flare shot across the bow contained in the Flash August PMI data from S&P Global. That report highlighted the growing likelihood that companies could be facing greater margin pressure as input costs continue to rise faster than their output prices. While slowing output price growth is helpful for inflation and Fed rate cuts, it’s a potential headwind for expected margin improvement and EPS generation for the next few quarters.

That is quite a combination of factors, and it’s one that means we will be walking a cautious path as we transition from August to September. In getting ready for what company management will say during the September wave of investor conferences, which could trigger a re-setting of EPS expectations, we will continue to focus on refreshing the Bullpen. Should that potential EPS expectation re-setting or the market have to dial back its aggressive 2024 rate cut expectations bring another bout of volatility to the market in September, we’d want to be in a position to take advantage of it just like we did in early August when we used market volatility to bring shares of Eaton ETN and Meta META into the portfolio.

Catching Up on the Portfolio This Week

The late-week, post-Powell-comments surge in the market led the Portfolio to close out a very positive week. All told, the vast majority of the Portfolio finished higher this week, helping lift the Portfolio’s overall performance. Notable gains were had in our more interest-rate-sensitive positions, with BLDR climbing low double-digits, making it the best Portfolio performer this week.

United Rentals URI and Vulcan Materials VMC shares were also strong outperformers as the market comes around to realizing the positive impact falling interest rates should have on their respective businesses. Renewed interest in Nvidia NVDA shares ahead of next week’s earnings report led those shares to climb nicely this week as did the shares of Marvell MRVL and Trade Desk TTD.

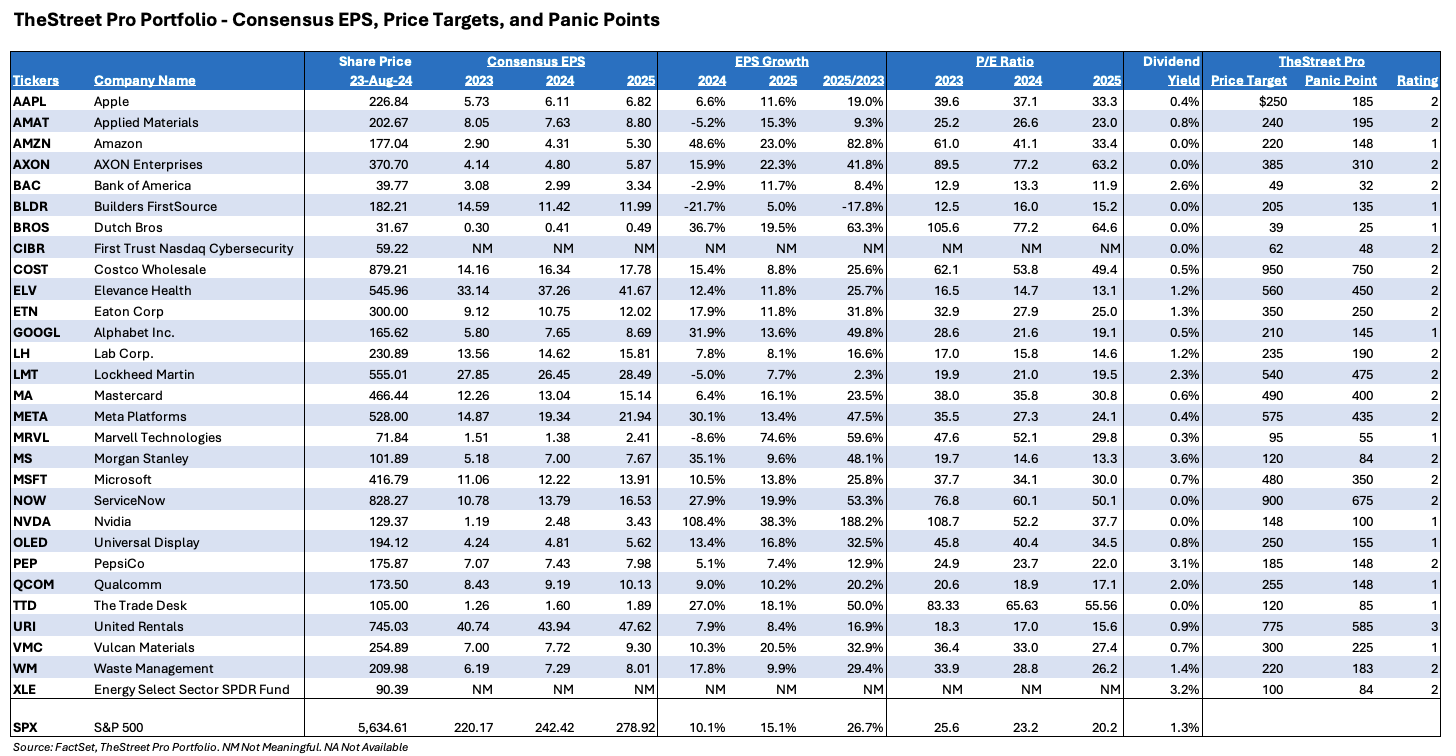

On Tuesday, we used the significant and recent moves and the overbought status to book some very profitable slices off the Portfolio’s positions in Axon AXON and Lockheed Martin LMT. Then, on Wednesday, we used a portion of that returned capital to pick up some additional shares of Dutch Bros BROS following its latest move lower. The combination of those trades put the Portfolio’s cash position at 9.3% of its assets.

In addition to those Portfolio moves, we added shares of Netflix NFLX to the Bullpen. On Thursday, we discussed some other interest rate-sensitive areas of the market and a few companies that could find their way into the Bullpen as the Fed embarks on the increasingly expected rate-cut cycle.

As we move to close out August and enter September, given the market’s overbought status and the once again stretched P/E multiple for the S&P 500, we will be even more selective with our next Portfolio additions. We will also keep in mind that September tends to be one of the poorest-performing months for the stock market. Between now and then, we’ll continue to ferret out new Bullpen candidates, so if things play out as we suspect, we’ll be ready. We’ll also continue to monitor positions that are encroaching on their price targets. As we refresh our fundamentals and technical analysis for them, we’ll determine if there is more upside to be had or if more prudent action is warranted.

In terms of upcoming dates to watch, we have our next set of Portfolio Office Hours on Tuesday, August 27 (from 4 p.m. to 5 p.m. ET in the Portfolio Forum), Nvidia earnings after the market close on Wednesday, August 28, and Marvell’s earnings the following day, also after the market close. And, as you’re marking your calendars, pencil in September 10, that’s the day Apple AAPL is expected to unveil its next iteration of iPhones.

This Week's Portfolio Videos

We cover a lot of ground during the week in our Daily Rundowns and the Portfolio Podcast. If you happened to miss one or more of them, here are some helpful links:

Monday, August 19: Our Road Map for the Coming Days

Tuesday, August 20: I See an Economic and Rate-Cut Wild Card Lurking

Thursday, August 22: Why We Raised Our Cash Levels This Week

Friday, August 23: Powell Confirms Policy Adjustment, But...

Key Global Economic Readings

Chart of the Week: The SPDR S&P Aerospace and Defense ETF (XAR)

Defense is a big theme in the political arena. Spending in this area is critical for our nation’s security and assisting other countries in need. But oftentimes, the spending is a bit more than needed — there needs to be a balance between replenishing stock, planes and weapons during peaceful times and war.

The SPDR S&P Aerospace and Defense ETF XAR has been on a roll of late. It is rumored that the U.S. government will be supplying Ukraine with more weapons in its battle with Russia, in addition to sending more weapons, drones and fighter jets to Israel to help improve its position. Whatever the decision, it is a boon to the group of companies in this ETF. No wonder the XAR has been running hot.

The candles show blue, which is bullish on the GoNoGo composite of indicators. Strong price action is chief among our indicators. Stochastics are also rising, good momentum fuels higher prices for XAR. MACD is on a buy signal as is the parabolic stop and reverse (SAR).

All in all, the XAR looks poised to continue making new highs. We have Lockheed Martin in TheStreet Pro Portfolio, which we rate a two, or stockpile on pullbacks. Lockheed is a highly-rated name in the XAR and represents a large weighting in the ETF. In addition, Axon Enterprise is also in the XAR, the largest weighting in the ETF.

Other charts we shared with you this week were:

Monday, August 19: S&P 500 - Bulls Got Some Relief in a Hurry

Monday, August 19: Builders FirstSource BLDR - Builders FirstSource is Coiling For a Move

Tuesday, August 20: Walmart WMT - We're Looking to Call Up This Bullpen Name

Wednesday, August 21: Trade Desk TTD - This Holding Is on the Cusp of a Breakout

Thursday, August 22: Meta Platforms META - Time to Add Shares of This Mega-Cap Holding

The Week Ahead

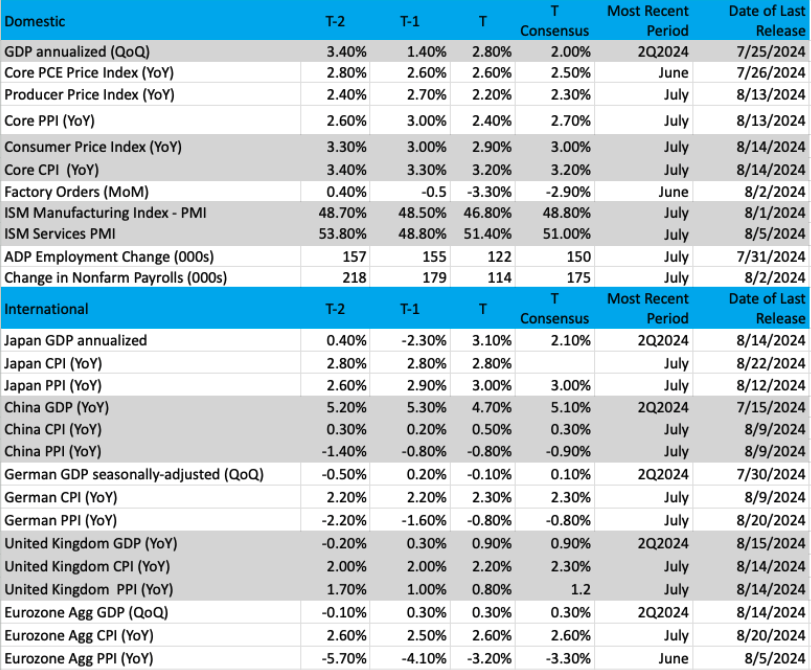

With Fed Chair Powell’s Jackson Hole comments behind us, next week the market’s attention will return to the last batch of quarterly earnings reports and the July PCE price index data. Because next week ends with a long weekend because of the Labor Day holiday that has U.S. equity markets closed on Monday, September 2, odds are that some folks will be on that last bit of vacation next week or taking off late in the week to make for an extended long weekend. This means trading volumes could run thinner than usual, exacerbating any market reactions.

With that high level thought out of the way, the market will be looking for further improvement in the July PCE price index to further cement the prospect for a September Fed rate cut. While Powell copped to a policy adjustment coming, as we suspected he would at Jackson Hole, he stopped there, reiterating incoming data would determine what happens next.

To us, that means we are likely to see a 25-basis point rate cut at the September meeting, but as we discussed on Friday, we have a lot more data to go until we get to that meeting and its outcome. If we see a pronounced fall off in key pieces of upcoming monthly data, including ISM’s Manufacturing & Service PMI, the August employment report and a few others, that could heighten the odds of a larger rate cut. This will keep us focused on the data.

Alongside that July PCE data, we’ll also get the Personal Income & Spending data and piecing all three of those data sets will give us a fresh look at real wage growth. Compared to earlier this year, real wage growth has slowed and the continued slowing in the jobs market depicted in this week’s Flash August PMI reports from S&P Global suggests that should continue. If that is what next week’s data shows, it will raise questions about consumer spending prospects. As we saw this week, the growing number of retailers that dialed back their forward guidance already suggests they expect the selective consumer to stick around. We’ll continue to favor Costco COST and Amazon AMZN shares.

Here's a closer look at the economic data coming at us next week:

U.S.

Monday, August 26

- Durable Orders – July (8:30 a.m. ET)

Tuesday, August 27

- FHFA Housing Price Index – June (9:00 a.m. ET)

- S&P Case Shiller Home Price Index – June (9:00 a.m. ET)

- Consumer Confidence – August (10:00 a.m. ET)

Wednesday, August 28

- MBA Mortgage Application Index – Weekly (8:30 a.m. ET)

Thursday, August 29

- Initial and Continuing Jobless Claims – Weekly (8:30 a.m. ET)

- GDP - 2Q 2024 – Second Estimate (8:30 a.m. ET)

- Corporate Profits – 2Q 2024 (8:30 a.m. ET)

- Retail Inventories – July (8:30 a.m. ET)

- Pending Home Sales – July (10:00 a.m. ET)

- EIA Natural Gas Inventories – Weekly (10:30 a.m. ET)

Friday, August 30

- PCE Price Index, Personal Income & Spending – July (8:30 a.m. ET)

- The University of Michigan Consumer Sentiment Index – Final (10:00 a.m. ET)

International

Tuesday, August 27

- China: Industrial Profits - July

Wednesday, August 28

- Japan: Leading Indicators (Final) – June· Eurozone: Loans to Companies & Households - July

Thursday, August 29

- Eurozone: Economic Sentiment & Consumer Confidence, Selling Price Expectations -August

Friday, August 30

- Japan: Retail Sales, Industrial Production – July· U.K.: Bank of England Consumer Credit – July· Eurozone: Inflation Rate - August

Just because next week is the last unofficial week of summer doesn’t mean we won’t have to jump through some earnings hoops next week. We have two portfolio companies reporting – Nvidia and Marvell – and another sea of retail-facing companies and a few others we’ll want to focus on.

Because NVDA shares account for close to 6.5% of the S&P 500, making it the third-largest holding in the basket, that report and the company’s guidance could have a meaningful impact on the market. So far this earnings season, Big Tech has lifted its AI and data center spending, and results as well as guidance from Microsoft MSFT, ServiceNow NOW and others show AI adoption is accelerating.

To that we can add, Taiwan Semi’s TSM June quarter results and guidance as well as its gang-buster July sales report. All of this lines up to suggest we should see another vibrant quarter from Nvidia. On Friday, we shared that we may need to revisit our NVDA price target if the company’s 2H 2024 EPS growth prospects versus 1H 2024 are way ahead of the 17% growth rate implied by the market’s consensus.

Turning to Marvell, the same factors we outlined above go for it as well. Let’s also remember that Marvell counts Microsoft, Amazon and Meta as proprietary AI and data center chip customers. Inside Marvell’s guidance, we’ll be looking for confirmation for a rebound in its enterprise networking and carrier infrastructure segments. Our thinking remains that as AI-on device and enterprise AI adoption grows, the chain reaction will lead to improving demand for those Marvell segments as network capacity utilization levels climb.

With that in mind, we will be parsing comments from Salesforce CRM about AI adoption across its platforms. And with an eye toward Qualcomm QCOM, what HP HPQ, Dell DELL and Best Buy BBY say about AI-on PC shipments in 2H 2024 and 2025 could bring a catalyst to drive QCOM shares higher. With Best Buy, we’ll also be interested in its comments about upcoming smartphone launches and the uptake of AI-capable smartphones.

Below, you can see that we have another wave of retailers, and we’ll use those learnings to round out our thinking about consumer spending prospects. As we saw this week between Macy’s M, Williams Sonoma WSM, Target TGT, TJX Companies TJX and others, the consumer is selective, trading down and looking for ways to stretch existing spending dollars.

Here's a closer look at the earnings reports coming at us next week:

Monday, August 26

- Open: Heico HEI

- Close: Trip.com TRIP

Tuesday, August 27

- Close: Ambarella AMBA, Nordstrom JWN, PVH PVH.

Wednesday, August 28

- Open: Abercrombie & Fitch ANF, Bath & Body Works BBWI, Chewy CHWY, Foot Locker FL, JS Smucker SJM, Kohl’s KSS

- Close: Affirm AFRM, CrowdStrike CRWD, Five Below HPQ, HP HPQ, Nvidia (NVDA), Okta OKTA, Salesforce CRM, Victoria’s Secret VSCO.

Thursday, August 29

- Open: American Eagle AEO, Best Buy BBY, Birkenstock (BIRK), Burlington Stores BURL, Dollar General DG, Malibu Boats MBUU, Ollie’s Bargain Outlet OLLI·

- Close: Dell DELL, Gap GPS, lululemon athletica LULU, Marvell (MRVL), Ulta Beauty ULTA

Portfolio Investor Resource Guide

- Economic Data: Here's a List of Links to the Key Economic Data We Closely Watch

- Investing Terminology: 16 Key Terms Club Members Should Know

- 10-Ks: Want to Know About a Stock? Read the Company's Reports

- 10-Qs: Unlock the Numbers and Key Information Behind Your Stock With the 10-Q

- Income Statement -Our Cheat Sheet to Understanding This Financial Document

- Balance sheet, Cash Flow Statements, and Dividends - How to Know If a Company Is Off-Kilter? Read Its Balance Sheet

- Valuation Metrics - Everyone Wants a Value. Here's How Investors Can Find

The Portfolio Ratings System

1 - Buy Now (BN): Stocks that look compelling to buy right now.

2 - Stockpile (SP): Positions we would add to on pullbacks or a successful test of technical support levels.

3 - Holding Pattern (HP): Stocks we are holding as we wait for a fresh catalyst to make our next move.

4 - Sell (S): Positions we intend to exit.

More Pro Portfolio

- Booking a Slice of Big Chip Gains

- Weekly Portfolio Roundup: The Bulls of Summer

- From AI to Aging Americans, We've Got the Scoop

At the time of publication, TheStreet Pro Portfolio was long BLDR, ETN, META, URI, VMC, NVDA, MRVL, TTD, AXON, LMT BROS, AAPL, COST, AMZN, MSFT, NOW and QCOM.