Looming Rate Cuts Have Us Looking at New Bullpen Candidates

As eventual rate cuts bring folks back to the market, here are two areas that could benefit.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

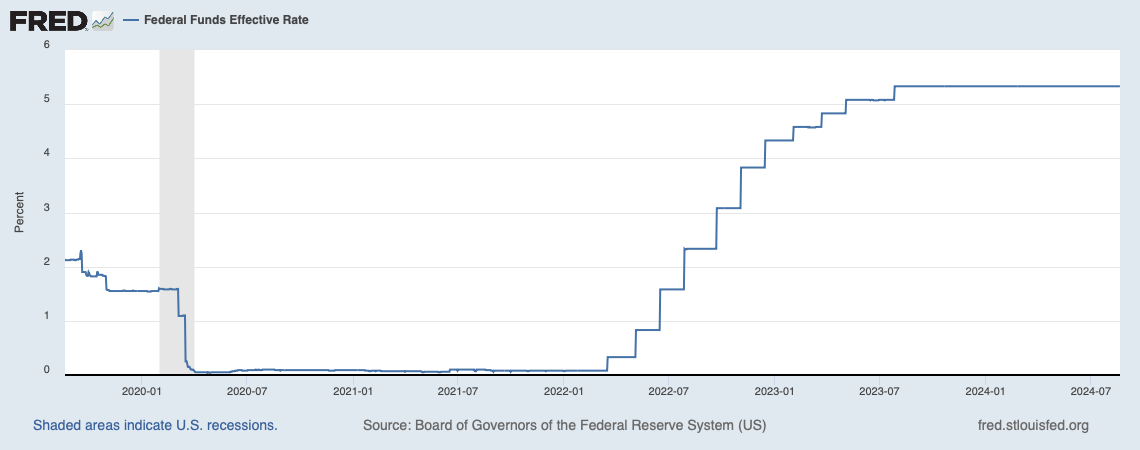

The Fed’s July meeting minutes suggested that we are that much closer to the Fed entering a rate-cutting cycle and we are contemplating what that could mean for several different areas of the market.

Previously, we’ve discussed what rate cuts could mean for shares of more interest rate-sensitive positions in the portfolio, such as Vulcan Materials VMC and Builders FirstSource BLDR. Expanding that view could help identify new areas for us to explore first for the Bullpen and potentially for the Portfolio.

When the Fed hiked the fed funds rate, it quashed the “there is no alternative” (TINA) trade in the market because there was now a risk-free alternative at banks. Even Apple AAPL and American Express AXP offered high-yield savings accounts, which for now still pay 4.25% to 4.40%. But, come Fed rate cuts, past a certain point, we are likely to see some downward adjustments in those and other products. That could bring some money into the market, but some of it could be looking for more dividend yield rich opportunities.

In this week’s Saturday signals alert, we’ll be sharing a startling revelation: “Gen Xers between 45 and 54 years old had a median account balance of roughly $60,000 in defined-contribution retirement plans at Vanguard Group in 2023, according to the firm.”

This means that there will be a need for income, and that suggests capital coming back into the market may be looking for high-dividend yields or companies with a rising dividend bias.

REITs and BDCs

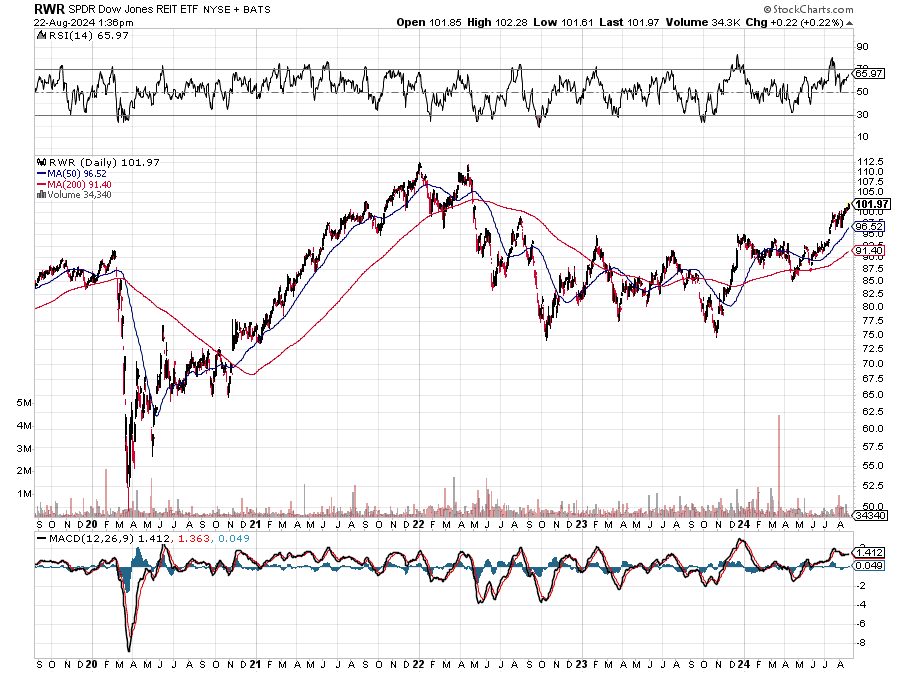

When we think of high dividend-yielding companies, two categories quickly jump out — real estate investment trusts (REITs) and business development companies (BDCs), like the portfolio’s one-time position in Trinity Capital TRIN that delivered a high teens return including dividends received. What both of these structures have in common is that they must pay out at least 90% of their net income to shareholders each year. As we can see in the chart below, REITs fell out of favor as the Fed hiked the fed funds rate in the first half of 2022 and kept going.

While we’ll keep tabs on Trinity and other BDCs, lower rates could be a tailwind to the spreads and fees they generate on new originations. With REITs, not all are created the same. There are healthcare facility-focused REITs, data center REITs, shopping mall REITs, industrial-focused ones and even commercial office space ones as well as diversified ones.

Given the lingering issues of return to work, we’re not particularly interested in office REITS, but given our thematic bent and our related investment strategies, we are more interested in data center as well as those that fit our aging-of-the-population theme.

We have Welltower WELL in the Bullpen already and it has made a nice move so far this year ahead of Fed rate cuts. It may not be done, but we are kicking ourselves for not making the move with the shares earlier this year. Others on our radar include Omega Healthcare OHI; Healthpeak Properties PEAK; which merged with Physicians Realty Trust; Ventas VTR; Digital Realty Trust DLR; and Equinix EQIX.

Rising Dividend Payers

We’ve talked before about the Dividend Kings, of which PepsiCo PEP is one, and the Dividend Aristocrats, which are members of the S&P 500 that have increased their dividends in each of the past 25 years. Kings tend to factor into Aristocrats, provided they are members of the S&P 500, like PepsiCo is. What we like about these companies is their ability to consistently increase their payouts to shareholders no matter the economic environment. As the fed funds rate declines, we are likely to see investor interest in these types of companies grow.

Much like our diverse cybersecurity play through the First Trust Nasdaq Cybersecurity ETF CIBR, there are a few plays of the Aristocrats, including the ProShares S&P 500 Dividend Aristocrats ETF NOBL. It’s big and it’s liquid, but for investors looking for income, it falls a bit short. In 2023, NOBL paid out just $0.70 in dividends per share and so far, this year it looks like $0.80. Potential shareholders would have to be more inclined to forego meaningful dividend income and settle for capturing the price return as the market re-embraces dividend payers.

In the portfolio, besides PepsiCo, we have Qualcomm QCOM, which has steadily boosted its annual dividend since 2004. A few more years and it could qualify for Aristocrat status. Mastercard MA is another dividend grower as are Waste Management WM, Eaton Corp. ETN and, more recently, Morgan Stanley MS and Universal Display OLED.

Similar to our thinking on REITs, when we look for fresh rising dividend payers for the Bullpen, we’ll do so with an eye toward our thematic strategies. Companies poised to prosper from those tailwinds should see benefits not only in their revenue, profits, and earnings but also in their cash flow and ability to further increase their annual dividend payments to shareholders like us.

More Pro Portfolio:

- Booking a Slice of Big Chip Gains

- Weekly Portfolio Roundup: The Bulls of Summer

- From AI to Aging Americans, We've Got the Scoop

At the time of publication, TheStreet Pro Portfolio was long BLDR, AAPL, PEP, CIBR, QCOM, MA, WM, ETN, MS and OLED.