Portfolio Defensive Stocks Offer Shield From Piping Hot Producer Prices

We braced for hot prices, but we didn’t expect they’d be boiling.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

We were bracing for a step up in inflation pressures. We has read through the April Purchasing Managers’ Index reports from the Institute for Supply Management, saw the uptrend in oil and petrochemical prices and heard the company comments on tariffs. But even so, we still didn’t expect the red-hot data found in today’s April producer price index (PPI) report.

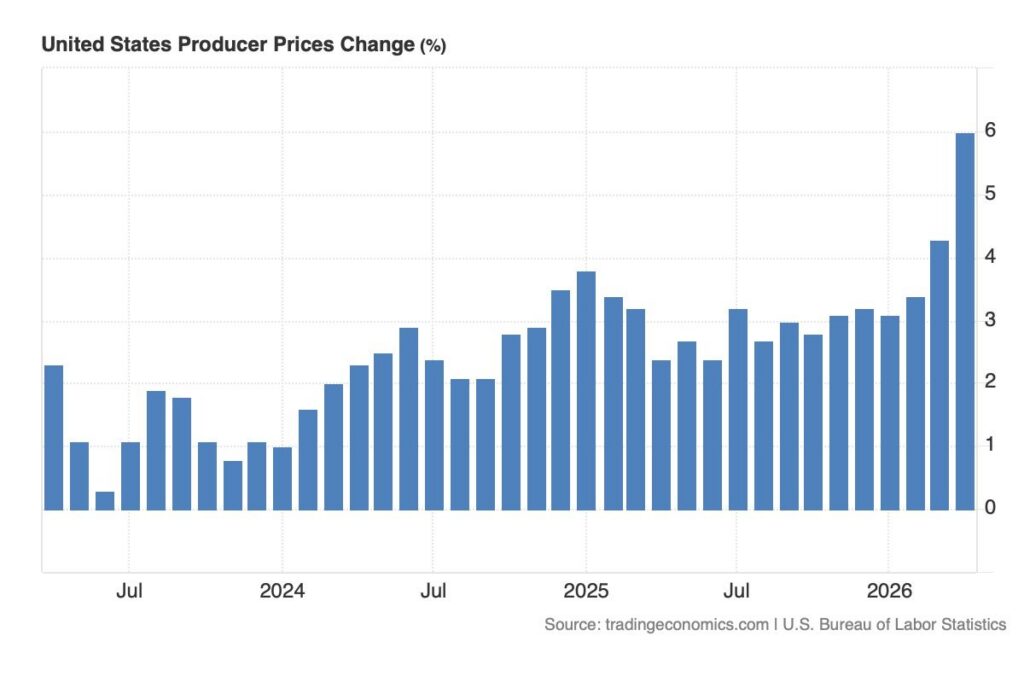

Headline PPI came in at 6.0% year over year, well ahead of the market’s 4.9% forecast and up meaningfully from the 4.3% figure from March. For context, the April reading was the highest back to December 2022.

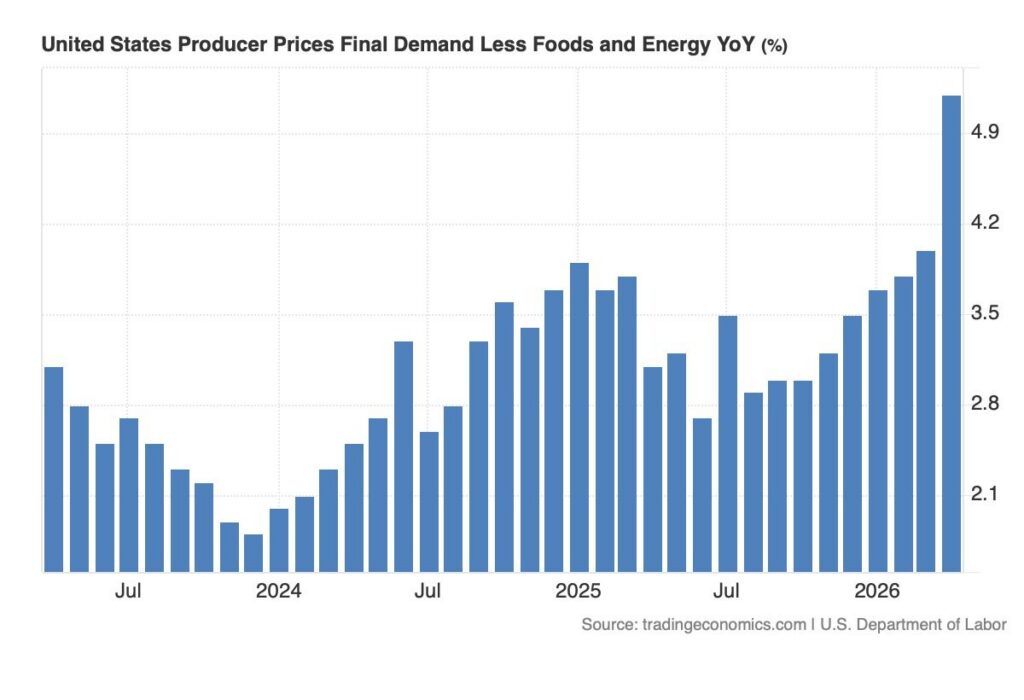

April core PPI also soared past consensus expectations coming in at 5.2%, nearly a full point higher than the 4.3% expected and well above March’s 4.0% reading.

Despite what some in Washington would say, the key to the last few months of PPI data is inflation pressures are building in the system. Based on ISM and S&P Global PMI comments about efforts to boost output prices, the logical conclusion is we are going to see consumer price index (CPI) data move higher.

The fallout from this means the Fed, even with pending Fed Chair Kevin Warsh, is going to have a very hard time arguing for additional rate cuts any time soon. In fact, we could see murmuring about the need for a potential rate hike.

We will see renewed margins concerns for those companies that are not able to pass along price increases and that will raise questions over earnings per share prospects.

Comparing the year-to-date, year-over-year wage growth data between 3.4%-3.7% found in the monthly employment report against the 3.8% figure for the April CPI and the sharp step up in PPI will call into question consumer spending power as the benefit of tax refunds fade.

The above reaffirms our concern over consensus 2026 EPS figures for the S&P 500 as well as our positions in Costco (COST), TJX (TJX), and Amazon (AMZN). As we lean into retail and other consumer-facing earnings with the S&P 500’s relative strength level at 73.68, we’ll maintain our market hedging, inverse exchange-traded fund positions.

And while we tend to not wage into political discourse, there is little question claims by those in Washington that inflation has been beaten, to use their own words, is fake news.

At the time of publication, TheStreet Pro Portfolio was long AMZN, COST, and TJX.