No Rate Cuts Anytime Soon After the March CPI Report

We will now be paying close attention to Thursday’s PPI report.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

* A hotter-than-forecasted March CPI report has the market trading off.

* We will stick with our portfolio plan, waiting for more favorable risk-to-reward entry points for our shopping list to emerge.

* Here’s why we’re focused on tomorrow’s March PPI report.

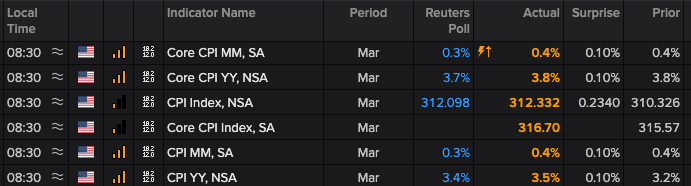

Equity futures plummeted after the March CPI report that, as we expected, showed hotter than inflation figures, was published. While the market consensus was for the core CPI to rise 3.7% on a year-over basis and 0.3% compared to February, the published figures came in at 3.8% and 0.4%, respectively, matching their February counterparts.

As you can see in the below table, headline CPI also came in ahead of expectations.

Getting ready for this morning’s report, we shared our view that we were likely to see the March figures come in ahead of expectations and it would mean that meaningful inflation progress stalled in the last six months. Part of our portfolio plan was to wait on the sidelines for the report because of the potential market reaction that we are now seeing as the market comes to grips with falling rate cut prospects for this year.

We have our shopping list and as stocks come to more favorable risk-to-reward levels, we will opportunistically deploy some of the portfolio’s capital.

Despite the March data collected ahead of this morning’s report, we’re still a little surprised the market consensus was looking for some modest improvement compared to February.

While we can’t speak for others, as we like to say, we will continue to let the data talk to us and that means paying close attention to tomorrow’s March PPI report. Given what we’ve seen in oil, gas, and other commodities, we are likely to see an uptick in that report compared to February, but the question to be answered is will it be hotter than expected?

If it does, we could see the market continue to trade off like we are seeing so far today. It could also lead to some speculating the Fed may need to hike one more time to finally break inflation and get it back on track.

As of now we give that a low probability of happening, but again, we will continue to evaluate the oncoming data, letting it talk to us, and adjusting our outlook as needed.