New Applied Materials Checkpoint as We Update Our Portfolio Table

We’ve refreshed consensus EPS estimates, potential pick-up points, beta, RSI levels and more for each holding.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

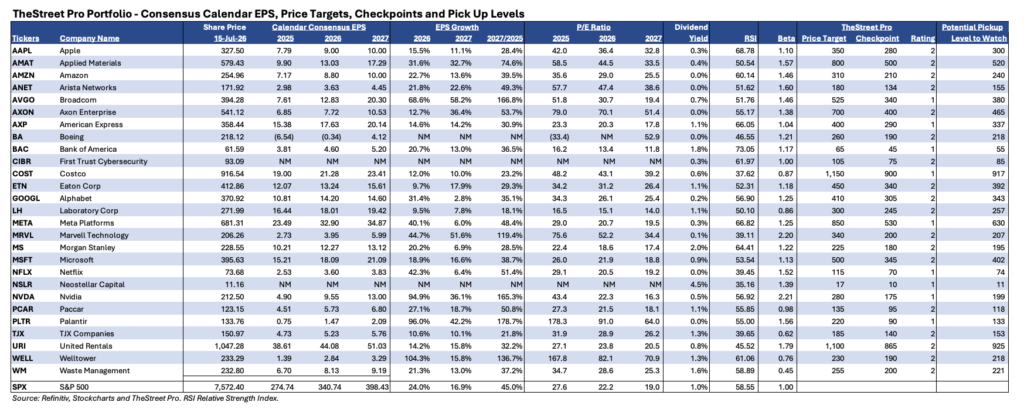

We have updated our table for the Pro Portfolio, which includes fresh consensus EPS estimates for each holding, current P/E ratios and the latest beta and relative strength index (RSI) levels. It also provides fresh levels at which we would contemplate adding to our holdings, subject to cash on hand and new information that could become available as we move deeper into the current earnings season.

Before you scan the table below for those potential pick-up levels, a few comments.

1. In response to the current market mood but also the upsized capital spending plans from Samsung (SSNLF), SK Hynix (SKHY), Micron (MU) and now Taiwan Semiconductor (TSM), we’ve reset our checkpoint for Applied Materials (AMAT) to $500 from $600. While this may seem counterintuitive, we are giving the shares a bit more room given the potential for near-term volatility. Should that emerge, our plan would be to use it to add to our AMAT position should a compelling risk to reward trade-off present itself. There is no change in our bullish stance on the shares.

2. When you examine the EPS Growth columns, especially the one for 2027/2025, which depicts the multi-year EPS growth the market expects, you’ll see some substantial EPS growth figures. That’s on both an absolute basis and relative to what the market expects for the S&P 500. Those substantial growth rates include those for Palantir (PLTR), Broadcom (AVGO), Nvidia (NVDA), Marvell (MRVL), and… Welltower (WELL).

That last one might surprise you, but it speaks to the power of the demographic shift behind the Silver Tsunami as well as Welltower’s shift to focus solely on senior housing. We intend to revisit our current $230 price target when the company reports its quarterly results on July 27. Part of what we’ll be focusing will be the timing of expected portfolio dispositions that will increase its focus on senior housing. As that happens, we should see a positive delta in Welltower’s margin profile.

3. On the topic of P/E ratios, no doubt a few will stand out. Nvidia, for example, at roughly 16x expected 2027 EPS, Boeing (BA), at more than 50x 2027 consensus EPS estimates, and those for Palantir and Axon (AXON). While we understand some folks focus on P/E ratios when it comes to our chip holdings, such as Nvidia, and also for Palantir and Axon, our preferred valuation metric is the price-to-earnings growth (PEG) ratio. PLTR is trading at a 1.5x PEG on expected 2027 EPS prospects, while AXON is trading at a PEG of 2x, on a similar basis. For Nvidia, it’s more like 0.35x, while Broadcom is near 0.38x and Marvell at 0.73x.

With Boeing, remember our play here is on ramping aircraft production and capturing the benefit from fixed-cost absorption and rising incremental margins. What that means is currently Boeing’s earnings are depressed, making the shares look expensive on a P/E basis. As Boeing converts its backlog to shipping aircraft, consensus EPS figures for 2028 approach $8, and that upswing is what we aim to benefit from.

More Pro Portfolio:

- Adding to 3 Portfolio Holdings, Resetting 2 Checkpoint Levels

- 30 Signals Across the Portfolio’s 10 Themes and Strategies

- Weekly Roundup: Portfolio Extends Lead, Adds Firepower Ahead of Earnings Season

At the time of publication, TheStreet Pro Portfolio was long the positions in the table.