Major Taiwan Semi Sales Growth Supports Five of Our Positions

Plus, what we expect from the big Apple Intelligence update coming today.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

In Friday’s Weekly Roundup, we discussed how the decline in the Volatility Index (VIX) suggested that investors had become a tad complacent.

Amid the market’s move lower on Monday — granted, from near-record levels — we saw the VIX move higher as the market gets ready for Wednesday's November CPI report. While we have some positive developments spinning out of November revenue from Taiwan Semi TSM and quarterly earnings last night from Oracle ORCL and Toll Brothers TOL, we could be in for a subdued day on Tuesday as investors wait for the CPI data.

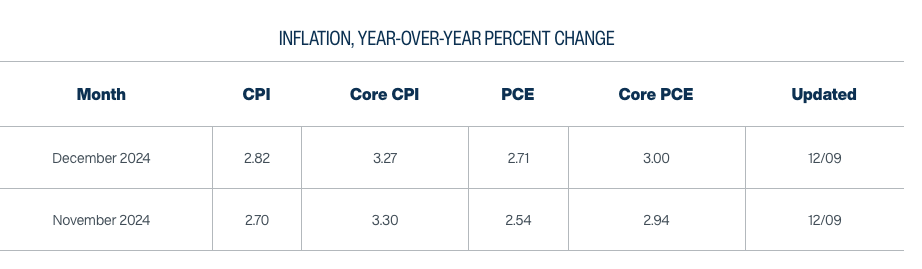

Headline CPI is expected to tick up to 2.7% year over year from October’s 2.6% print, while the consensus view for the core reading sits at 3.3% year over year, the same as September and October, and up from 3.2% for the two prior months. We see that as more data moves in the wrong direction, with the same being said for the sequential core CPI reading of 0.3% expected for November. Looking at an early view on December CPI, the Cleveland Fed’s Inflation Nowcasting model doesn’t offer much hope for a meaningful decline either.

Should the November CPI data line up with the consensus forecast, it would be the fourth consecutive month at that level, which means a trailing three-month annualized figure of 3.6%. In short, figures like that will not go unnoticed by the Fed nor should they be ignored by the market. While some may be tempted to put some capital to work on Tuesday following Monday's market trade off, we’ll ride Tuesday's trading hours out and wait for Wednesday's inflation revelation.

Taiwan Semi November Sales Up Almost 34% Year Over Year

While we wait for that report and the reverberations through market rate cut expectations or not, Taiwan Semi reported November revenue that rose just shy of 34% year over year. While the typical seasonal pattern of a decline compared to October repeated, the company’s combined October and November revenue, which rose 31% year over year, should dampen any questions about AI, data center or smartphone demand. We see that supporting our positions in Nvidia NVDA, Marvell MRVL, Apple AAPL, Qualcomm QCOM and Universal Display OLED.

Big Apple Intelligence Update Set: What We Expect to Happen Next

As we think about TSM’s monthly figures to come, we’ll want to watch the December and January figures to see an early response to Apple’s updated iOS 18.2 with richer Apple Intelligence features.

That update is expected to land later on Tuesday, and early reviews are positive, and that could help spur the iPhone upgrade cycle. With even more Apple Intelligence features slated for future iOS updates, we continue to see a protracted upgrade cycle over the coming quarters.

More Pro Portfolio

- We're Locking In a Triple-Digit Gain for This Deeply-Overbought Name

- Weekly Roundup: A Lack of Fear Is Concerning as the Market Melts Up

- Half of U.S. Living Paycheck to Paycheck — and More Headlines You Might Have Missed

At the time of publication, TheStreet Pro Portfolio was long NVDA, MRVL, AAPL, QCOM and OLED.