This ETF Says It Beats the Market. Here’s the Catch.

AVUV bets on cheap, small stocks besting the market. The edge is real, but streaky. Here’s who should consider it.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

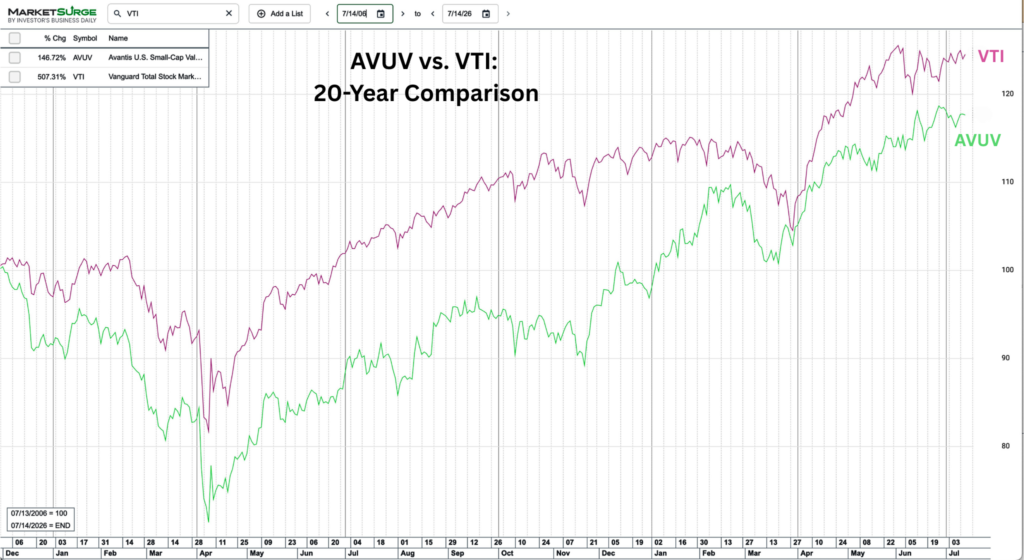

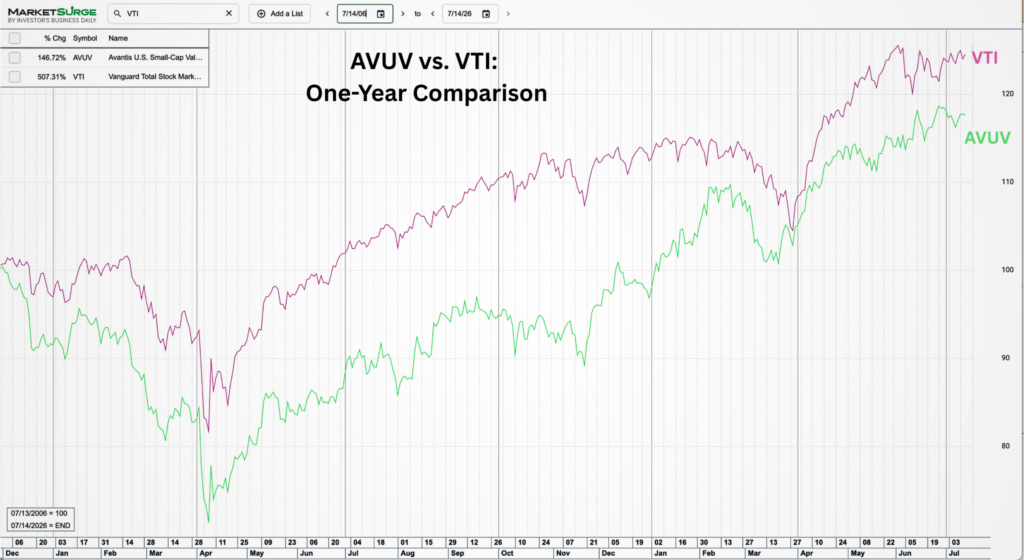

The idea behind the Avantis US Small Cap Value ETF (AVUV) is simple: Small, undervalued companies have a track record of outpacing the broader market over time.

But that doesn’t mean that outperformance is consistent; these stocks can win big, and then languish for the next 10 years.

AVU is built specifically to hold onto small, cheap companies throughout thick and thin, awaiting the payoff.

These charts show its performance versus the Vanguard Total Stock Market ETF (VTI), which tracks a broader market index, over the past 20 years and over the past year

AVUV owns a basket of small U.S. companies, but it’s selective about which ones: Managers favor stocks that are cheap relative to their earnings, but still solidly profitable.

This ETF behaves like an index fund in some ways, such as its breadth and low cost. Its expense ratio is 0.25%. Relative to indexes, that’s on the higher side. But compared with active funds, it’s on the lower side.

But unlike an index fund, which updates its holdings on a regular schedule, AVUV checks prices continuously, leaning further into stocks as they get cheaper. It also pares back other holdings as they get pricier, rather than waiting for a scheduled reset.

How It Stacks Up Against an Index

VTI tracks the broader U.S. stock market, which includes smaller names outside of the S&P 500.

VTI’s fee of 0.03% means its return is close to that of the underlying index, without expenses chipping away too much.

VTI really isn’t much different from its larger cousin, the Vanguard S&P 500 ETF (VOO). But VTI has cast a wider net, as it includes mid- and small-cap names that aren’t part of the S&P 500.

The two ETFs are highly correlated. The largest companies in the U.S., the ones that dominate the S&P 500, also constitute the majority of VTI’s holdings, since both funds are market-cap-weighted. The mid- and small-cap slice VTI adds barely moves the needle, as you’d expect.

It’s a reminder of just how different AVUV’s approach really is.

VTI and VOO are essentially both bets on the same handful of giant companies. AVUV is the opposite. It’s designed specifically to avoid those giants and lean into the part of the market those two Vanguard funds don’t touch.

The Real Case for AVUV

Plenty of ETFs are running on a gimmick, or latching onto something trendy.

But AVUV’s thesis isn’t just a marketing pitch; it’s based on decades of academic research and billions of dollars invested in factor funds. So it’s been road tested.

Despite the broad asset class of domestic small-caps outperforming in streaks, rather than consistently, there are a few reasons why it may be an acceptable portfolio addition for some investors.

- The Nobel Prize wasn’t for nothing. Fama and French’s research found that small and cheap value stocks have historically outperformed, although as I noted earlier, not on a consistent basis. This pattern wasn’t concocted by some fund company to drum up interest in a new product.

- This isn’t some wacky experiment. AVUV is constantly adjusting its holdings to lean into cheap, profitable companies. It’s a real, funded thesis, not some trendy gimmick.

Why VTI Is Often the More Suitable Choice

AVUV isn’t based on some thesis a marketing department cooked up last week. But there are reasons why most investors are still better off with VTI.

- If it were free money, it wouldn’t last. Markets move fast, and when enough investors pile into “cheap and small,” that edge tends to shrink or disappear. Other factors take the lead.

- The risk is the whole point. Even the researchers who found this pattern agree: The extra return has always been tied to extra risk, rather than being a free lunch. Remember, risk and return are related! Taking extra risk isn’t necessarily bad, but it depends on your liquidity needs, among other things.

- Expect the lag. AVUV can badly trail VTI for years at a time. That should surprise exactly no one who understands the nature of small value stocks. However, most people don’t have the patience or the time to ride out the lean years.

- Fees add up. You’d pay 0.25% every year with AVUV versus 0.03% with VTI. Regardless of which ETF outperforms in any given year, that gap is always there, even when the payoff isn’t.

When AVUV Might Make Sense

A smaller allocation of about 5% to 10% of assets, or even less, might be suitable for an investor with decades of runway ahead and the ability to stomach what history shows is likely to be a bumpy ride.

But that investor would want to layer AVUV on top of a core index holding. AVUV is not a replacement for most people’s core portfolio.

Bottom Line

For most retirement savers, a low-cost total-market fund does the job quite well without asking you to bet on a theory whose results happen to match up with your specific timeline.

Simple wins for most portfolios. Keep in mind: AVUV isn’t a scam. Far from it, in fact. But it’s just a bet most people don’t need to make.