3 Dividend Plays for Traders ‘Behind in the Count’

How a baseball mindset can improve your covered-call score.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

Sometimes you have to think of trading as you would playing ball.

Let me explain.

An experienced MLB hitter approaches the plate quite differently depending on the pitch count. A batter ahead in the count 3-0 will sit on his pitch and swing away only if he gets it. The outcomes are favorable. Most likely a hit if the batter makes contact or a hard-hit ball that just happens to go right at the third baseman if bad luck hits. A foul ball, taking a strike or a whiff, just pushes the count to 3-1, which is still a favorable count.

A batter behind in the count 1-2 approaches the plate in a completely different and cautious way. He chokes down on the bat, intent of just putting the ball in play or at least fouling off the pitch.

I approach the market this way. If I believe market valuations are stretched and I am growing increasingly concerned about a potential AI bubble, I am focused on playing “small ball,” as if I am behind in the count.

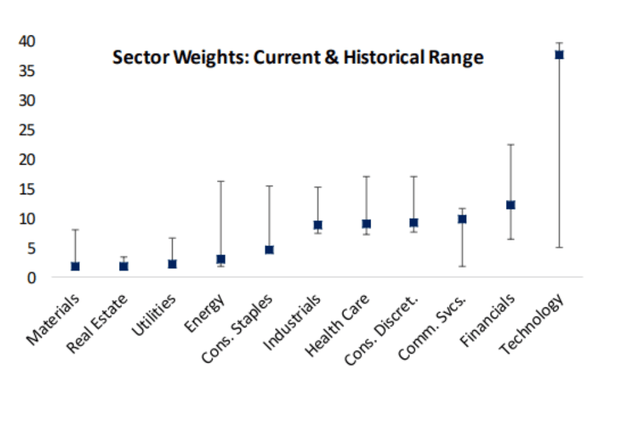

For this means acting upon the few stocks I am finding in this market that are sporting reasonable valuations for covered-call trades. That way I can produce a solid profit even if my target trades down a tad over the option duration. Not surprisingly, I am finding most of these opportunities in the sectors in the market that are significantly below their historical weightings as tech and tech-related names have dominated the rally in the market that began when ChatGPT debuted on the market in November 2022.

Last Monday and Wednesday I highlighted several covered-call holdings I hold within the Biotech/Biopharma sector. As you can see above energy, real estate and staple are also currently significantly underweight compared to their historical levels. In this article, I will highlight a few solid dividend plays in these sectors that I am boosting the yield around holding within covered call positions.

In real estate I continue to avoid the home builders even as many are trading near their book values. I feel there is still some more pain to come due to the moribund housing market. I think it is likely I will be back in the sector at some point in 2027 at lower entry levels and hopefully some improving trends.

I do hold CTO Realty Growth, Inc. (CTO) as the only real estate investment trust in my portfolio at the moment. The stock has been a steady performer here in 2026 as management continues to upgrade its retail property portfolio. The shares still trade at a reasonable just over 10-times forward funds from operations and they also provide a healthy 7% dividend yield.

In the consumer staple space, PepsiCo. (PEP) is looking more interesting after a recent post-quarterly earnings slide. The business is being hurt by a struggling consumer and higher gas prices. After the recent pullback, the shares trade just under 16-times forward earnings and have a solid 4.4% dividend yield.

Finally, ExxonMobil (XOM) is a good proxy for the energy sector and provides an over 2.8% dividend yield and trades at a reasonable 11-times forward earnings.

These are some ways I’m playing small ball right now.

At the time of publication, Jensen was long CTO, PEP and XOM