With July PCE Data in Hand, We're Shifting Focus to These Rate-Cut-Sensitive Positions

The market may see bad August jobs data as good news for a September rate cut and we've got some sensitive Portfolio holdings.

You've reached your free article limit

You've read 0 of 1 free Pro articles.

*July PCE data in line with expectations, next week’s data will shape September rate cut expectations

*July Personal Consumption ticks higher, outpaces personal income gains

*Consumers continuing to eat into their savings rates explains increasing selectiveness

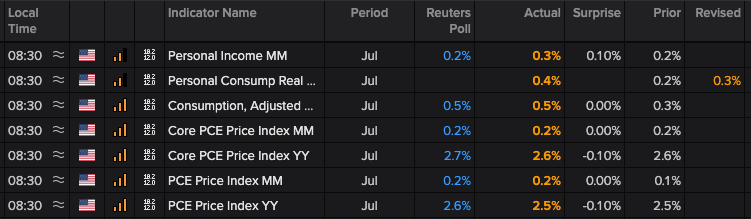

The big economic data point of the week, the July PCE price index, is out and for the most part, it was as the market expected with the core PCE reading rising at 0.2%.

We did see a modest surprise in the year-over-year figure for core PCE that remained at 2.6% in July, not ticking higher as the market expected. Because there were no major surprises, the report should not alter the thinking behind Fed Chair Powell’s Jackson Hole comments that called for an “adjustment” in monetary policy. However, those looking for clarity on whether the Fed is going to start its rate-cutting cycle with a move of 25 or 50 basis points will have to wait until we get through next week’s wave of August data.

The probable focus will be the pace of job creation and how it stacks up compared to the 114,000 non-farm jobs added in July. We’ll have ample tea leaves in the various August PMI reports and ADP’s Employment Change Report for the month, which will help fine-tune expectations relative to the current 163,000 market consensus for August. If we see the number of jobs rebound to that level and the PMI composites for August show the economy is not stalling out, odds are market expectations for a 25basis point rate cut in September will firm. However, if August job creation falls below the July figure and the August PMI figures soften considerably, we could see the market start to expect something larger on September 18.

The larger question is whether the Fed will deliver the 100 basis points of rate cuts that the market sees before the end of the year. So far, our thinking is that we’re more likely to get two rate cuts, but we’ll continue to let the data talk to us and adjust our thinking as needed. One of those data points will be the Fed’s updated set of economic projections and what they pencil in for rate cuts this year and next. It’s that total amount of rate cuts over the next six quarters that we’re more interested in as they could impact our more interest-rate-sensitive positions, such as Builders FirstSource BLDR, United Rentals URI, Vulcan Materials VMC and, to some extent, Eaton Corp. ETN.

The Consumer and Our Coty Exit: Personal Savings Rate Continued to Fall in July

Friday morning’s data also showed an uptick in July personal consumption spending, which likely reflects the pull forward in spending from Amazon's AMZN 2024 Prime Day and competing efforts. The continued drop in the personal savings rate to 2.9% in July from 3.3% to 3.5% in April and May helps explain why consumers are becoming increasingly selective. This also explains some of the guidance we’re getting from the likes of Dollar General DG and even Ulta Beaty ULTA.

On Thursday night, Ulta reported an earnings miss and cut its comp sales growth for the year to -2% to 0% from its prior outlook for 2% to 3%. Parsing that out, the company’s first quarter (April) comps rose 1.6% but fell 1.2% in the second (July) quarter, and that means management sees further softness in the next two quarters. The earnings call comment that stood out to us was that Ulta is seeing pressure in the prestige category, which reaffirms our recent decision to close out the portfolio’s exposure to Coty COTY. That pinch the consumer is feeling keeps us bullish on our positions in Costco COST and Amazon.

More Pro Portfolio

- Taking Some Profits in a Healthcare Stock and Downgrading Its Rating

- Weekly Roundup: Powell’s 'Adjustment' Drives the Market and Portfolio Higher

- Cash-Strapped Consumers, Mortgage Rate Lows: The Latest Signals Informing Our Strategy

At the time of publication, TheStreet Pro Portfolio was long BLDR, URI, VMC, ETN, AMZN and COST.